Last week I read an article on Seeking Alpha by Andy Obermueller titled, "SodaStream: This 'Coca-Cola Killer' Is A Great Holiday Growth Stock". The author did some "boots-on-the-ground reconnaissance", observing that in various stores the SodaStream (SODA) makers were selling very well. Readers of some of my earlier articles will note that I'm a big fan of this kind of investing, and I appreciate the approach that Andy took. It's the strategy I used to pick stocks like Target (TGT) and Verizon (VZ). I love shopping at Target, which seems to be always packed every time I go. In addition, almost everyone I know uses Verizon Wireless, including myself, and since going over to FiOS, I can't see myself switching away from it. For these two companies, boots-on-the-ground experience as well as the financials made sense to me, and as a dividend growth investor, I felt that they would make great long term stocks.

In reading about Andy's assessment of SodaStream, two things pop out at me immediately from the title . First, SodaStream is no Coca-Cola (NYSE:KO) killer. I'll get to that later. Second, what is a holiday growth stock? Does that mean that you buy the stock when the product sells well during the holidays, and then after good quarterly results you unload it for a profit? The article isn't clear, but if you're going to compare this company to Coca-Cola, it had better be a great long term hold, and not something that you buy for a 1 to 2 month turnaround. After all, Coca-Cola is regarded historically as one of the greatest long term investments.

Company Comparison

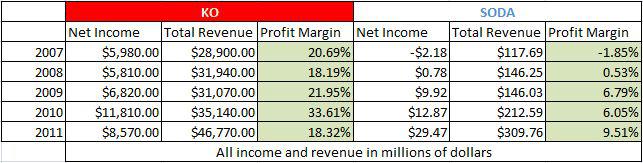

Since these companies are vastly different in size, I decided to look at profit margins for the past 5 years.

(Click to enlarge)

As the data clearly shows, SodaStream is no Coca-Cola. Despite the numbers, you have to consider that KO is a well established company, and the product isn't really the same. SODA sells syrup and CO2, whereas Coca-Cola sells the finished product, consisting of mostly water. The difference between syrup and water (that investors care about, at least) is that water is cheap. This means that Coca-Cola should inherently have higher margins that SodaStream. It also means that if at any point in the future Coca-Cola felt threatened by SodaStream, they could afford to sell their product for less and still be competitive. I guess they could also buy SodaStream outright, but that probably wouldn't make too much sense for them. The point is that you can't call SodaStream a Coca-Cola killer when the profit margins are less than half, or negative.

Long Term Prospects

Coca-Cola has been and will be around for the long term. I'm not going to spend any more time on that. Read this old article of mine if you disagree or want some more details.

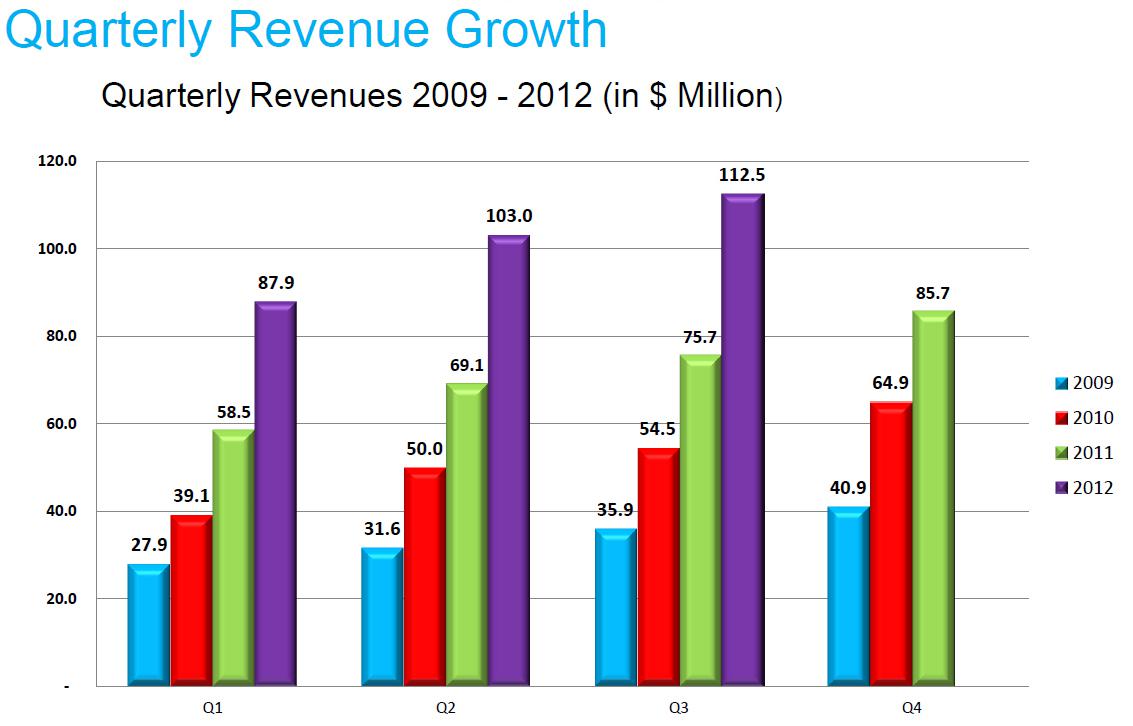

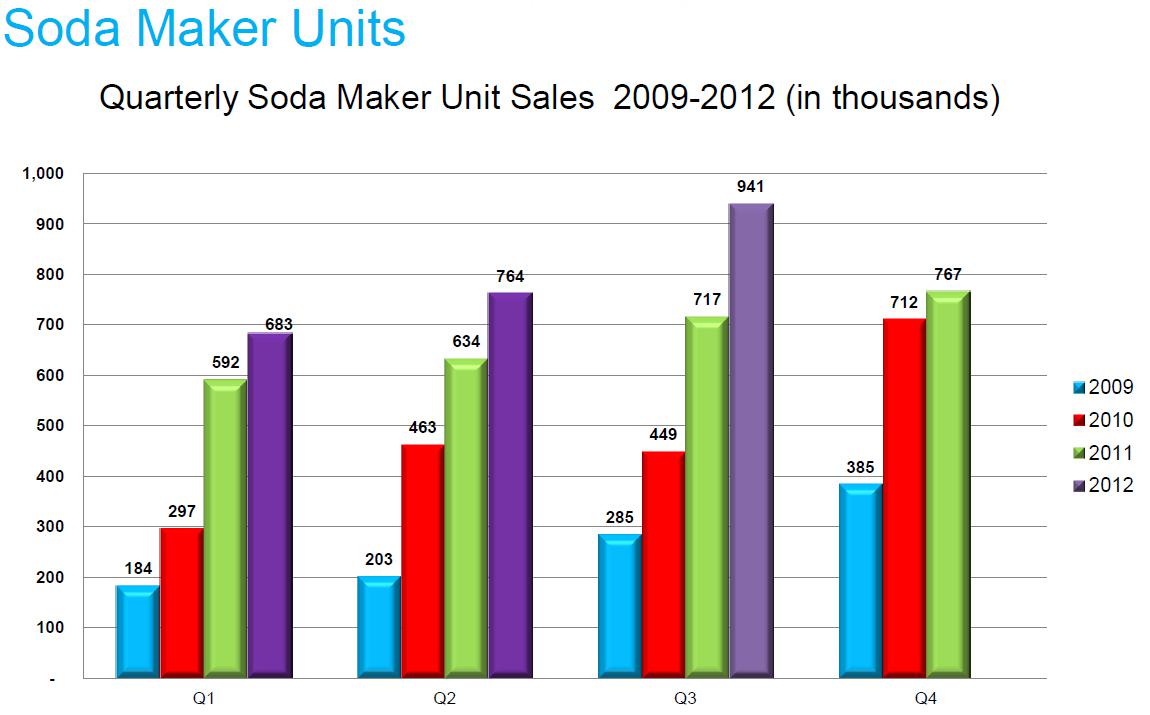

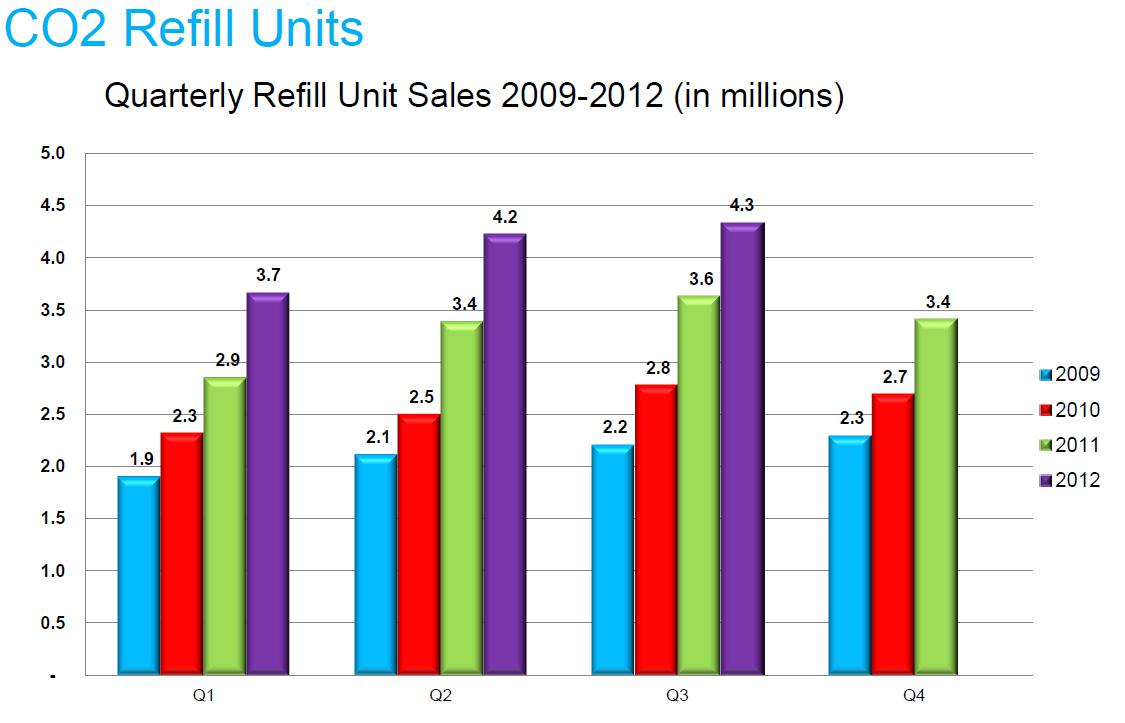

SodaStream is a little more complicated. Luckily, I was able to get some useful information from the 2012 Q3 press release. The company was kind enough to offer three graphs, for quarterly revenue, soda maker sales and CO2 refill sales, dating back from 2009 Q1 up to 2012 Q3.

(Click to enlarge)

(Click to enlarge)

(Click to enlarge)

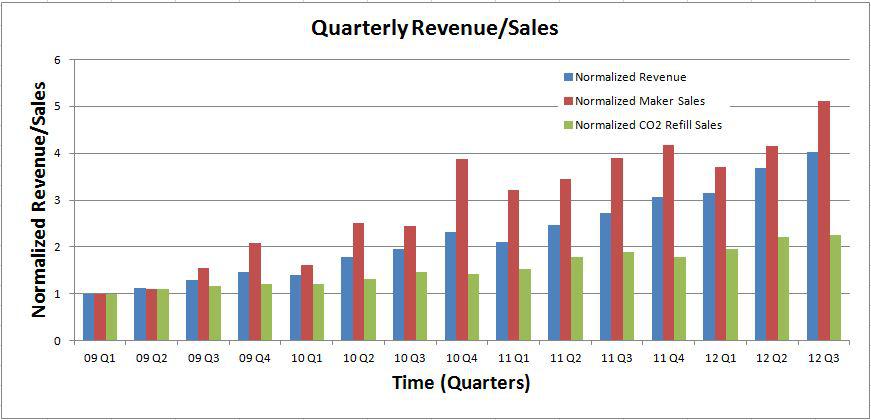

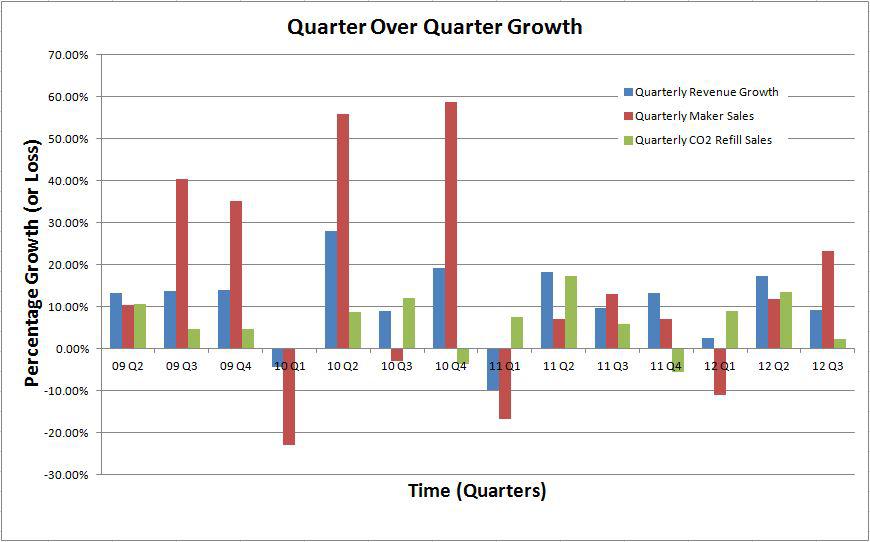

From the graphs, there appears to be steady growth. To make this data more useful, I re-graphed it from 2009 Q1 through 2012 Q3, all in a row, instead of grouping the data by years. I normalized it to scale it for comparison. I also calculated and graphed quarter over quarter percentage growth.

(Click to enlarge)

(Click to enlarge)

The sales and revenue shows me something interesting; While revenue and soda maker sales have been going up, the CO2 refills have not been able to keep pace. Since CO2 is needed to actually make use of the product, and the refills aren't keeping up with sales, this indicates that after trying it out, the SodaStream is destined to sit for the remainder of its lifetime in the appliance closet, between the Ronco Rotisserie and the EZ Egg Cracker. The revenue must be coming largely from the soda maker. Unfortunately for the company, these are one time sales. To make SodaStream a solid long term investment, revenue will have to come from CO2 and syrup refills.

The graph showing quarter over quarter growth seems very sporadic. For any growth company, I'd like to see consistent growth, not the random jumps and falls that SodaStream is showing. The CO2 refill growth is much lower than soda maker sales, and that may be the only thing sustaining the refills. If that's the case, once the soda maker growth levels off, the CO2 refills (and syrup sales) will begin to shrink. If you're still convinced that SodaStream is a solid company, this will be your indicator to get out (or run out). The company can only survive in the long run if consumers keep buying their products after the initial soda maker investment.

Conclusion

If you decide to get out, my suggestion is to go to the real killer: Coca-Cola. You don't get to $86 billion in assets and over 500 brands from inconsistent growth; you get there from selling great products that consumers buy over and over again.

Thanks for reading my article. I hope you got something useful out of it. I understand that not everyone is a dividend growth investor (although I'm not sure why), so your particular style of investing might find SodaStream to be a great company for your portfolio. Anyway, tell me what you think. If I'm missing some important information in my analysis, please tell me in the comments below.

Disclosure: I am long KO, TGT, VZ. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.