By: Jayson Derrick

2013 will be an interesting year for Chipotle Mexican Grill (NYSE:CMG) as the company has the opportunity for re-invigorated same-store sales driven by a change to the menu pricing and new catering initiative. The recent quarterly results were a miss, but I believe investors should consider some of the background context and focus on the positives. Furthermore, Chipotle's growth potential remains among the highest in the Mexican casual fast food industry. With an improving same store sales, fewer margin headwinds, and a multi-year runway for growth both domestically and internationally there is no reason why investor's should not expect anything but a positive 2013 and beyond.

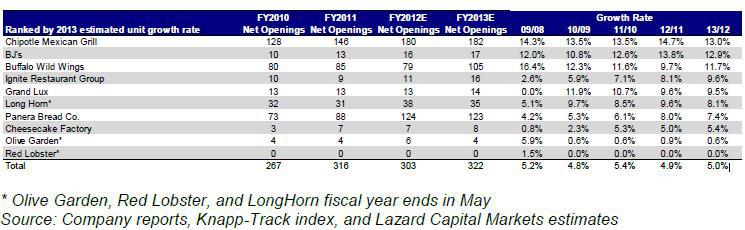

Significant growth potential ahead

In 2011, the LSR (Limited Service Restaurant) Mexican industry was estimated to be nearly $13.5 billion. The top 150 Mexican fast casual concepts accounted for nearly $5 billion. Chipotle is leading the way in the Mexican fast casual restaurant with over $2 billion in sales which accounts for nearly 15% of the LSR Mexican industry. By comparison, the next largest competitor Qdoba only generated $530 million in sales in 2011.

The Mexican restaurant category is growing faster than the overall industry as well. The LSR Mexican industry grew nearly 4% in 2011, compared to a 3.5% growth in the general fast food industry. Not only is Chipotle's unit growth rate among the highest in its peer group but Chipotle is one of the fastest growing public restaurants between 2009 and 2012 averaging roughly 14%.

Same-store sales poised to re-accelerate

Same-store sales slowed throughout 2012 as pricing rolled off and the macro environment remained challenged. In 4Q12, two-year traffic trends fell to single digits for the first time in over eight quarters. Two catalysts that will re-invigorate same-store sales in 2012 are menu pricing and a new catering initiative.

Menu pricing: During investor presentations, management indicated it intends to "possibly" raising prices during the middle of 2013.

New catering initiative: Chipotle launched a catering service in the Colorado market on January 21 and plans full system penetration "in the coming months" intended for 20-200 clients. Catering should drive positive mix in a similar way that yielded success for Panera Bread (PNRA) over the past few quarters. A 3% same-store sales lift can add an incremental $0.40 to EPS. From an optimistic point of view, long-term same-store sales contribution could be in the high single-digit to low double-digit range and contribute up to 10% to EPS growth.

Successful execution of growth plan despite moderation among peers

In 2013, double-digit rate of unit growth expansions should continue. Many investors were surprised that Chipotle added 60 new restaurants in fourth quarter 2012, bringing the total added in 2012 to 183. Prior guidance issued in October was for "at or above 155-165" stores. Chipotle should maintain current growth rate for 2013 and looking beyond 2013, management hopes to have between 3,000 and 4,000 restaurants compared to the roughly 1,300 today. Such forecasts are conservative and realistic in a global context for a rapidly growing, and more importantly, popular restaurant chain.

Margin outlook improving

Commodity prices spiked in 4Q12 and caught management by surprise. 4Q12 margin declined 150bps year-over-year to 24.6%. Commodities should ease in 2013 giving restaurants some relief and reduce margin pressure. Looking at the overall picture, one could conclude the 4Q12 EPS miss was limited to the quarter. Higher menu prices and lower commodity costs should work in Chipotle's favor in 2013.

Valuation, target and conclusion

Applying a 30x PE multiple to a conservative 2014 EPS estimate of $12.00 yields a price target of $360 which represents a roughly 15% upside. A 30x forward PE multiple seems appropriate as it is in line with the stock's 5-year historical average. The future appears to be bright for Chipotle and although the stock price is expensive, it can present an attractive investment opportunity for investors that want exposure to the fast food restaurant industry.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.