A retirement portfolio does not always belong to a retired person. These portfolios can be funded by inheritance, stock options, the sale of a business or just built by disciplined savings. The origins do not really matter, but they do make for interesting stories and I love hearing them from my clients. When these accounts are needed for income to pay for living expenses a higher yield matters assuming the owners have a need to maximize the income for their comfort. The longer an account holder can wait to take the income the more focus shifts to the income growth rate.

My previous article addressed my portfolio design for maximum current income. This time I'm going to attempt to share my thoughts on a portfolio of maximum income growth. This requires more crystal ball work than high income with low growth. Higher current income is often related to low growth rates and can be found in capital intensive sectors like utilities and real estate. High income growth over any meaningful time frame needs innovation, competitive advantages and the ability to strongly pass input costs into pricing or in other words - just growth.

Setting Realistic Goals is a Key to Success

So what are some good realistic goals for a portfolio designed for maximum income growth? I feel that the current yield will be at a discount to future growth. This means you are having to pay up (in a big way) for quality. The higher the quality of the income stream the lower that yield on purchase will be.

A good example of this is 3M (MMM):

Price: $108.26 P/E: 17 Yield: 2.3% 5 yr Growth Forecast: 8.95%

3M has paid dividends for 97 years, the market sees 3M as a high quality income stream with growth premium. Margins are high and debt is under control with a strong share re-purchase program in place and all this with a payout ratio of about 38%.

My crystal ball tells me that a portfolio can generate a current yield of 4% and can grow that income at 10% per year (outside of growth from share purchases). All of these type accounts are for growth so we will re-invest when doing a model. Current income will be needed in the future for this portfolio design, but that need must be at least 10 years in the future.

Portfolio goals:

- Yield at Purchase of 4%

- Dividend growth rate of 10%*

- Re-invests all dividends.

- Low taxes.

- 20 year time frame

I don't want to waste time with tracking yield on purchase (YoP). YoP is a good way to congratulate yourself but is less important than actual dollars getting paid to you. When considering retirement it is more efficient to look at current yield on invested capital value. In a tax sheltered account an individual may easily rebalance at a future time to maximize that yield. A cash account may need to consider capital gains before rebalancing for higher current yield.

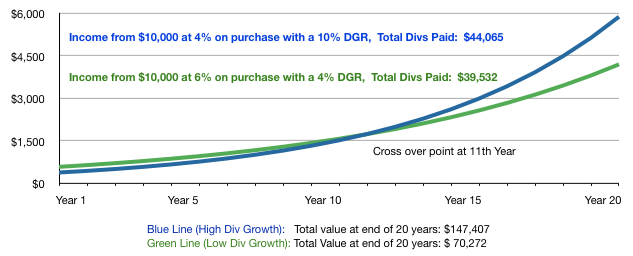

Let's look at a 4% Yield on Purchase with a DGR of 10% and compare it to my maximum current income model of 6% Yield on Purchase with a target of 4% DGR. Source www.piermoney.com.

(Click to enlarge)

In fairness I have added a share price growth equal to the DGR. That means price appreciation was added to the formula before the re-investment of the dividend. This is a linear model and does not reflect the ebb and flow or volatility seen in the market. The validity of a model like this is questionable, however from a historical perspective if the dividend is growing and maintains its quality then the market will rarely discount the price. For example - as Coke grows, it's dividend grows, for the most part.

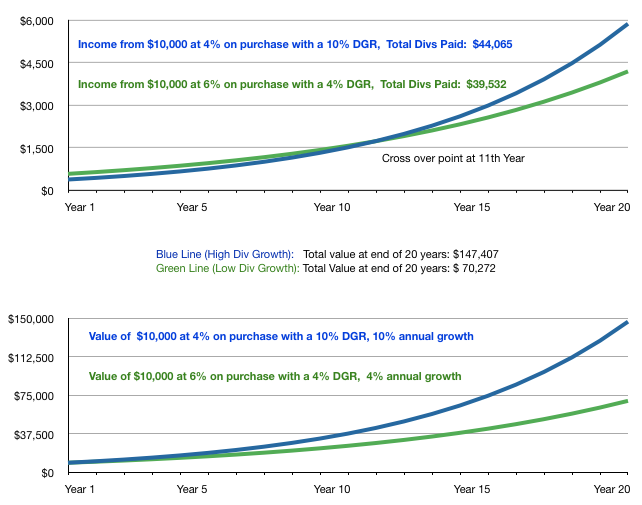

Let's add the capital value to the above chart.

(Click to enlarge)

Yes, time is the friend of the steady investor. A strategy based on low income (with high income growth) would do best with an 8 to 10 year time frame before needing the whole income stream for living expenses. An ideal situation would be an individual that did not need to maximize income an could simply wait for the inherent appreciation in a low yield, high DGR model. Either way is better than selling shares and being subject to market fluctuations to determine the life cycle of your account.

Let's switch to a look at what I use to build this type of portfolio. I'm not going to spend much time on breaking down each stock but I will show our purchase target.

Technology

- Apple (AAPL) Buy below $440 3yr DGR: **

- Microsoft (MSFT) Buy below $34 3yr DGR: 15%

- Intel (INTC) Buy below $24.50 3yr DGR: 15%

Consumer Goods

- Philip Morris (PM) Buy below $88 3yr DGR: 13%

- General Mills (GIS) Buy below $48 3yr DGR: 12%

- Wal-Mart (WMT) Buy below $72 3yr DGR: 13%

- Coke (KO) Buy below $39 3yr DGR: 7.5%

- Starbucks (SBUX) Buy below $53 3yr DGR: **

- Walgreen (WAG) Buy below $42 3yr DGR: 26%

Healthcare

Energy

- Holly Energy (HEP) Buy below $40 3yr DGR: 5%

- Kinder Morgan (KMP) Buy below $85 3yr DGR: 5%

- Energy Transfer (ETE) Buy below $59 3yr DGR: 6%

- Chevron (CVX) Buy below $105 3yr DGR: 10%

- Exxon (XOM) Buy below $86 3yr DGR: 9.5%

Utilities

REIT's

- Realty Income (O) Buy below $45 3yr DGR: 6%*

Manufacturing

- 3M Buy below $104 3yr DGR: 5%

- General Electric (GE) Buy below $21 3yr DGR: 5%

* Realty Income had a large recent increase that my Morningstar screen was not picking up, 6% is an estimate. Realty has a steady income growth starting high but growing slow and would be a minor part of this portfolio. REIT's would most often be in IRA's as well for tax purposes.

** I'm counting on Apple and Starbucks to add about 15% and 10% respectively, per year into the future. Starbucks is significantly over priced. That is a link to a solid discussion from a new SA contributor, Mr. Strohmann.

This portfolio has an equal weight DGR of 10.6%, I would not suggest an equal weight. I would have an overweight of consumer goods, technology and a few others adding to shareholder value with legitimate share re-purchase plans, such as Becton or Chevron . It is beneficial to start with a strong yield at purchase, and that would greatly affect the composition of the portfolio.

Portfolio Design Wrap-Up

These portfolios are not as price sensitive as those with current needs. The goals are set far in the future. Price does matter and I tend to wait for good pricing to make large scale moves into positions as that makes my clients safer and happier. Also a quick look at the end point shows that price appreciation is still 65% (approx) of the gains.

These positions are even more rarely sold than in a high current income portfolio and most of my activity in these accounts is with inflow of funds. I will sell positions and add stops if I see the need. A few reasons to do this, as previously discussed are:

- Rapid specific capital gains.

- Dividend growth underperformance.

- Eroding fundamentals (see Pitney Bowes).

- Periodic rebalancing.

- Mergers, divestitures and such (see Abbot and Altria)

- Life events not related to investing.

It is impossible to predict the future, of course. It has always been my investing philosophy to focus on a rising income stream to reach a goal for a portfolio. It is a much easier and measurable way to invest. Expectations must be realistic and risk well understood. The final results of a high DGR portfolio would most predictably fall short of a 10% annual price appreciation. In working a model for your own unique life situation I would discount that rate to 6%. Having a higher share price appreciation in the model makes the income stream prediction more conservative because it allows for the re-purchase to be less shares. Do you due diligence, and remember that nobody cares more about your money than you do.

Disclosure: I am long AAPL, MSFT, INTC, JNJ, BDX, WAG, GIS, KO, T, HEP, KMP, ETE, O, GE, MMM, CVX, XOM, SBUX, PM, WMT, CMS. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.