Advanced Micro Devices (NASDAQ:AMD) is a U.S., based technology company that specializes in the design and marketing of semiconductor devices. AMD is one of the two major marketers of central processing units (CPU), the other being Intel (INTC). AMD is also a major player in the graphics processing unit (GPU) market with NVIDIA (NVDA). The CPU is one of the main components of a computer while the GPU is a single-chip processor mainly used to control and improve the performance of 2-D or 3-D graphics, video, and texture mapping among others. The GPU work to lessen load on the CPU and, hence, produce video and graphics faster.

AMD is one of the stocks on the stock exchange nowadays that are most misunderstood by the investing public. Events in the recent quarters confirm this assertion. Or how else do we explain the negative reactions of many investors to the stock of a company that exceeded Wall Street estimates two quarters in a row and yet it shares were dumped leading to massive price dips? I took a cursory look at the possible causes of this negativity against AMD and I discovered that it was mainly because the company wasn't well-known the way investors know popular tech companies like Apple (AAPL) and even Netflix (NFLX). Therefore, since many investors are unable to reflect on the facts prevailing in the industry where AMD is listed, they generally conclude that the company is underperforming or lacks economic moat. There are also instances where investors would just believe the recommendations of some stock analysts without doing their own due diligence.

A Review of AMD's Recent Quarter Results

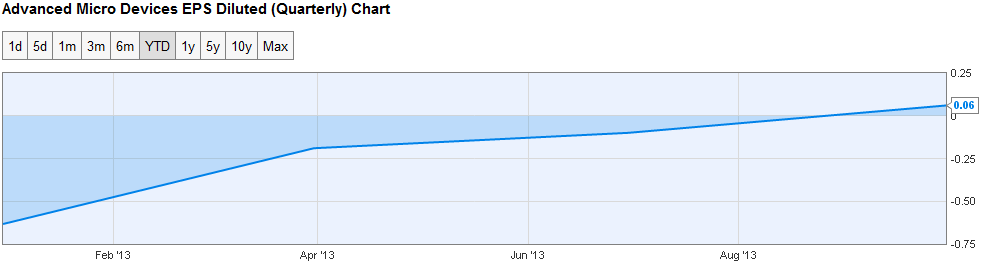

Two weeks ago, October 17 to be precise, AMD unveiled its 2013 Q3 financials to the investing public. The financial report shows clearly that the company has overcome its past issues and has returned to profitability due to the success of its business diversification plan. The company reported a net profit of $48 million for the quarter at earnings per share (EPS) of $0.06 from operating income of $95 million compared to a net loss of $157 million at earnings per share of $0.21 for the corresponding quarter of 2012. Non-GAAP net income also came in at $31 million or at $0.04 earnings per share from non-GAAP operating income of $78 million.

AMD grew its revenue from $1.27 billion it reported for third quarter 2012 to $1.46 billion for 2013 Q3 beating consensus estimates of $1.416 billion by $0.044 billion which translates to an increase of 26% sequentially and 15% year-over-year.

In his comment about the third quarter results, Rory Read, AMD president and CEO, said emphatically that:

"AMD returned to profitability and generated free cash flow in the third quarter as we continued to successfully execute the strategic transformation plan we outlined a year ago'.' He also added that:

"We achieved 26 percent sequential revenue growth driven by our semi-custom business and remain committed to generating approximately 50 percent of revenue from high-growth markets over the next two years. Developing industry-leading technology remains at our core, and we are in the middle of a multi-year journey to redefine AMD as a leader across a more diverse set of growth markets."

Despite the positive tone in these statements and reassurances of a revitalized company portrayed in the quarterly results, the shares of AMD dipped just because five analysts saw just one negative aspect of the report; the reduction in revenue growth for the next quarter to 5% and, therefore, downgraded the stock.

The Impacts of analysts' Downgrade on AMD

Five major Wall Street analysts, namely, Citigroup, Goldman Sachs, Sanford Bernstein, Credit Suisse, and Merrill Lynch issued negative ratings on AMD and, hence, generated a sell off momentum on its stock. AMD stock recorded about 12% price gain before the release of its 2013 Q3 results but unfortunately, it has gone down by more than 22% since its impressive Q3 financials were announced to the investing public due to the negative outlook painted by the five analysts. AMD could still have a huge break out this year but due to the negative impact of the downgrade on the investing public, value investors may have to wait till another quarter before seeing a huge increase in its stock price.

AMD's Valuation Metrics and Future Outlook

The semiconductor industry is highly competitive and also cyclical. Consumers' demands often change as rapidly as they evolve meaning that a semiconductor company must be constantly innovating and proactive about seizing opportunities in new niche areas as they evolve. The management of AMD has done a good job by repositioning the company for growth and to easily adjust to new market trends expertly. Here is a graph showing how AMD has returned to profitability during the last quarter:

(Click to enlarge)

AMD has been able to shift from niche areas like the PC that are declining in revenues to high growth niche areas like professional graphics and semi-customized chips such as the gaming consoles which currently constitute about 30% of AMD 's earnings. Due to the downgrade by rating firms, the shares of AMD are currently undervalued. Therefore, buying AMD at this time offers value investors huge opportunity for capital appreciation in the coming quarters. AMD stock is a BUY!

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.