The consumer-constrained by intense, structural-liquidity woes, without real growth in income, and without the ability or willingness to take on meaningful new debt-simply cannot support a sustainable turnaround in housing activity. - John Williams, Stadowstats.com

The big homebuilder stock spike on Wednesday on the back of the entire stock market rebounding sharply after the FOMC taper decision is a gift from the market gods to those who are looking to sell out of long positions in, or get short, the homebuilders. The National Association of Realtors (NAR) existing home sales report for November released Thursday confirms this view. As I'll explain below, not only were the results below consensus expectations, but a detailed look at the month to month sequential decline reveals a drop in existing home sales volume which is worse than is being reported by Wall Street analysts and the financial media.

First, I want to run through the numbers really quickly, which I'm accessing from this NAR data table (Pdf link). I want to focus primarily on the month to month sequential data as opposed to the seasonally adjusted annualized year over year numbers broadcast in the media. Using the unadjusted actual monthly data, we can see that going from October to November homes sales plunged by 53k, or 12.5%.

Seasonality aside, please recall that the storyline for October was that the government shutdown slowed sales down. Because of that it would stand to reason that sales should have bucked seasonality and there should have been a "snap-back" affect, since the government shutdown ended on October 17. To demonstrate the magnitude of this plunge, in 2012 the unadjusted sales from October to November only dropped 15k, or 3.8% vs. the hefty 12.5% plunge this year. To further illustrate this, year over year for November, unadjusted homes sales dropped 3.6%.

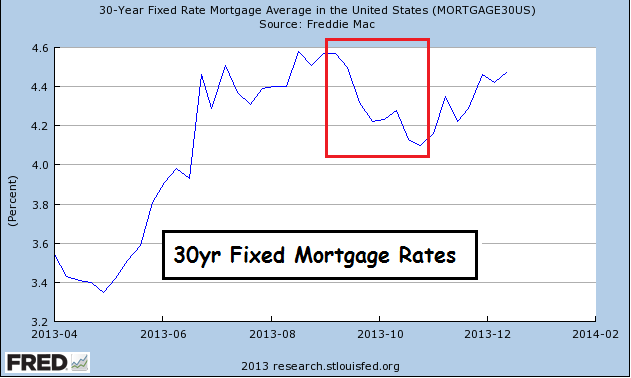

It is clear at least to me that something ominous is occurring in housing market sales activity and I've illustrated the declining trend in existing home sales that started in the early summer in previous articles on Seeking Alpha. This view is further reinforced when you consider mortgage rates. Existing home sales are accounted for when the sales transaction has fully closed, including title transfer. In other words, sales for November would reflect contracts signed in September and October, for the most part. Interestingly, 30yr fixed mortgage rates dropped by quite bit starting in late September and didn't start rising again until November:

(Click to enlarge)

As you can see from this graph, falling rates during September and October should have stimulated sales at least to the point at which the seasonal decline from October to November was comparable to that of the decline in 2012. Please note that most of the contracts signed which comprise the November sales number would have been signed during this period of falling mortgage rates.

The low inventory argument being thrust out by NAR Chief Economist Larry Yun (per the report link at the top) does not hold water, as you can see from this graph (edits are mine) straight from the NAR website that the total inventory of homes has been rising (red circle):

(Click to enlarge)

One point of note on the inventory number used by the NAR. It is a seasonally adjusted number. This means that to the extent a downtrend is starting to occur in the actual monthly data, as I argue is the case, the seasonally adjusted annualized rate of home sales mathematically overstates the true level of home sales. This is because, the way the inventory is calculated, the "month's supply" number becomes significantly understated until the statistically massaged numbers begin to "catch up" with the real numbers. In other words, in my view, the real inventory is quite bit higher than is represented by the NAR statistical method of calculation.

Falling prices is yet another indicator that the housing market is in a state of decline. Again looking at the NAR data table linked above, you find a section which shows the actual unadjusted sales prices. Prices peaked in June at $261k and have fallen every month since then down to November's $244.5k - a drop of 6.3% from June to November. It would seem that lower prices should be stimulating sales volume but they aren't. A big argument that has been made both by Wall Street analysts and the NAR's Larry Yun is that lower affordability in general has affected sales. Given the big drop in price over the last 6 months, combined with lower mortgage rates over the last 3 months, we would have expected to see some sort of "bounce" in sales, with or without seasonal bias. But sales continue to decline.

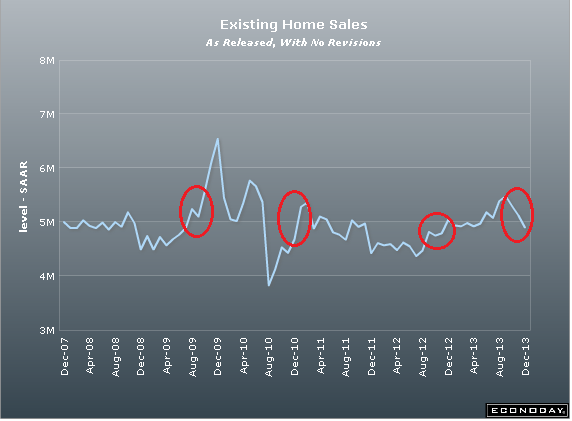

One more chart to illustrate my view (sourced from Bloomberg, edits in red are mine):

(Click to enlarge)

This chart shows the seasonally adjusted annualized home sales numbers going back to December 2007. As you can see from the red circles, in 3 of the previous 4 years, sales during the September to November period actually showed up as increasing during the period, as opposed to this year (and 2011) when they declined. This illustrates my point, especially given the relatively historically low mortgage rates right now, that the housing market is fundamentally in back in the bear market decline that started in mid-2005.

Based on my view of the housing market, I continue to recommend shorting the new homebuilders as the best proxy for playing the housing bear market theme. You can see my favorite short-sell plays in my article on new home sales a couple days ago. It is very important to keep in mind that this is a longer term play and not a day or week trade. The home builders are highly leveraged and heavily shorted, which means on days when the stock market moves higher, the homebuilders can really move up quickly for a short period of time. However, since mid-May the Dow Jones Home Construction Index (DJUSBH) has significantly underperformed the S&P 500. In fact, the DJUSHB is currently down nearly 16% from its peak in May.

To illustrate my point on the importance of being patient, I first called a homebuilder short at the end of January this year with the DJUSHB at 515. It ran up 550 by mid-May. However along the way I kept adding my short position in DR Horton (DHI) and I'm currently up well over 22% on my cost-averaged position. I've been up as much as 34% and I fully expect to ride DHI from roughly $26.50 to $6.50 or lower over the next year or two.

Disclosure: I am short DHI, KBH. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.