Why are you invested in actively managed mutual funds? Many of you who invest in mutual funds were probably told to buy them because some financial advisor recommended you do so. The harsh reality is the ones who own 90% of the $17 billion held in mutual funds didn't beat the market index. The same is true for the rest of the world, who have $35 billion held in mutual funds.

Below is the harsh reality when it comes to this professional manager performance.

In 2011, 79% of active fund managers didn't beat the S&P 500 stock index.

In 2012, 66% of active fund managers didn't beat the S&P 500 stock index.

In 2013, active fund managers came close to beating the S&P 500 index but still did not do so. In fact, according to McGraw Hill Financial Director, Aye M. Soe, CFA, as of mid-2013;

59.58% of large-cap funds, 68.88% of mid-cap funds and 64.27% of small-cap funds underperformed their respective benchmark indices. The performance figures are equally unfavorable for active funds when viewed over the three- and five- year horizons. Performance across all domestic equity categories lagged behind the benchmarks over the three- and five- year horizons.

When you add the fees that mutual fund managers make, it takes even more away from your mutual fund overall return. Mutual funds have raised their fees from an average of 0.62 % of assets to 1.11% of assets, an increase of 84%.

According to Yan Zilbering, an investment analyst with the Vanguard Investment Strategy Group, over time these fees add up.

If you invested $50,000 in a fund with the 2012 average Vanguard expense ratio of 0.19%, in 30 years you could have $65,793 more than someone who invested in a fund with the industry's average expense ratio of 1.11%.

The Financial Industry Regulatory Authority (FINRA) has a good calculator you can use to see what fees your mutual fund is charging you. It can be found by clicking here.

Mutual fund sales are big business and financial advisors make good commission from selling these actively managed funds to you. But are they really in your best interest in doing so? I don't think so, and the data above proves it. So what did you pay to get into your current mutual fund? To answer this, you need to know what type of shares you bought "A" front load; "B" back load; "C" annual fees (sometimes called no-load funds); and "H", which is a hybrid of "A" and "B" that includes both a smaller front load and back load.

On a $10,000 investment in "A" shares, a 5% front load fee would be $500. This means you start your investment with $9,500, but there are no back-end fees upon liquidation. A "B" shares purchase means that when you liquidate your investment, you are charged a declining fee that typically starts at 5% and disappears after 5 to 7 years depending on the fund.

No-load funds typically charge an annual fee, or what is called a 12b-1, that amounts to 0.25% of the fund's average annual net assets. It is important to note that the "B" back-end load shares mentioned above most likely also has a 12b-1 fee associated with it. Also, "H" shares typically have a higher 12b-1 fee.

Below you will find a comparison of 3 large cap blend funds with A shares represented by Rydex Funds (RYTTX), B shares represented by Prudential (PTMBX) and a no-load fund represented by Vanguard (VFIAX). The purpose of this analysis is not to say one fund outperforms the other based on how the manager invests, but to show you how fees and commission charged can affect your overall total return. Each fund has an initial investment of $20,000, the same 10-year time frame and each has an assumed annual return of 7%.

All things being equal, you can see how lower fees can make a huge difference in your overall return and you should be aware of what your advisor is selling you.

Lastly, some mutual funds are wrapped inside variable annuities and another layer of fees called a mortality and expense risk charge in the range of 1.25% per year of your account value, or $125 on a $10,000 investment. This fee takes care of insurance costs because the annuity is actually an insurance product, and also the commission paid to the broker who sold it to you since most of these variable annuities are no-load. Another word of caution with variable annuities is the liquidation penalty that can run quite high, typically 5% to 10%, if you need your money within the first 5 to 10 years. Also, the penalties for withdrawing your money before age 59 1/2 are 10%, but these annuities are tax-deferred. Unlike investing in mutual funds, however, your growth is not taxed as a capital gain, but rather as ordinary income. Variable annuities make zero sense inside one's IRA or 410k, unless of course you know you're going to live to 90 or 100 and can take advantage of life-time income options that beat the mortality tables that actuaries draw up.

With all these fees, commission, loads and penalties, how does an investor get ahead? Perhaps hedge funds are the answer.

For Hedge Fund Investors, It's Worse than Mutual Funds

No, hedge funds are not the answer. There are over 10,000 hedge funds holding $2.4 trillion in assets but hedge funds only rose 7.4% on average in 2013, making it the 5th straight year that hedge fund managers have not beat the S&P 500. The simple little S&P 500 Index has outperformed hedge funds for 10 straight years except for 2008, when both the S&P 500 Index lost big but hedge fund managers edged mutual fund managers in overall performance.

The best hedge fund manager in 2013 was David Tepper of Appalossa Management, whose fund was up approximately 38%, or just 9% more than the S&P 500 Index. For this performance, Tepper was paid $3 billion.

Just imagine what the hedge fund managers who are not beating the Index are getting paid! According to a recent Citibank study, they estimated that hedge fund managers

need at least $300 million Assets Under Management (AUM) to break even. This would mean that of the $300 million total needed for expenses, an investment manager would receive about 20% of $60 million or $18 million even before the fund has invested a dime. The larger the hedge fund, the less the manager makes. But of course, that's on a much larger piece of the pie like in Tepper's case above, as he manages approximately $18 billion of assets to have earned his $3 billion in 2013.

The wealthy in America may impress their friends by saying "I invest in Hedge Funds," but clearly most that do so are worse off than anyone else. I think you could have thrown darts at a Wall Street Journal listing of stocks and done better than the 7.4% average in 2013, and saved the fees paid to your funds' managers.

A good theory might be that mutual fund managers did better in 2013 than in past years because pre-2013 mutual fund managers took their horrid record of performance (not beating the indexes) to go manage hedge funds to get the higher payout. But still, the bottom line is, none of these guys are good at beating the index.

This leads us to the question; why are you paying anyone to manage your money when it is clear that you have a higher probability of success by simply buying an Index fund with lower fees that will put more money in your retirement account instead of your broker's retirement account?

For now, you are informed as to how well "the professionals" are doing with your hard-earned money. It truly has been awful. But more than likely you can do better if you follow these recommendations.

Recommendations

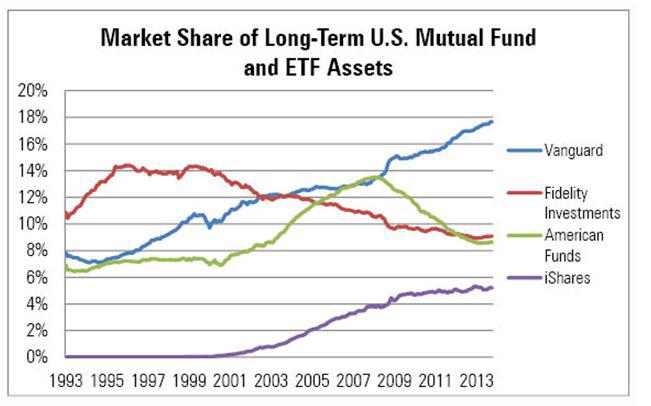

Vanguard was one the first to start an Index fund in 1976, and still whom I would recommend to use today. Its fees are lower than Fidelity, American Funds and iShares, its closest competitors, averaging just 0.15%, which is also a reason why the market share of Vanguard has grown to 44% for its passively managed shares.

The no-load Vanguard Index 500 Fund Admiral Class (VFIAX) or a couple ETFs; the Vanguard S&P 500 Value Index ETF (VOOV) or Vanguard S&P 500 Growth Index ETF (VOOG) will help you beat the mutual fund and hedge fund professional managers. For a complete list of Vanguard funds and ETFs see Morningstar.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.