I first wrote about this issue last summer when I noticed that there is a definite declining trend being established in terms of production per well in the greater North Dakota Bakken area, which also includes Three Forks and Sanish (link). Back then, there was little to go on in terms of being able to predict the effects on production going forward, therefore I assumed a hypothetical 3% per year decline in production per well and a steady addition of 2000 wells every year. That resulted in a forecast for a peak in total production of roughly 2.7 million barrels per day in the mid 2020s. Given what we now know about the rate of decline in production per well, which we can assume will not slow down, that estimate turns out to be highly optimistic.

Data source: ND Bakken Oil Production Statistics.

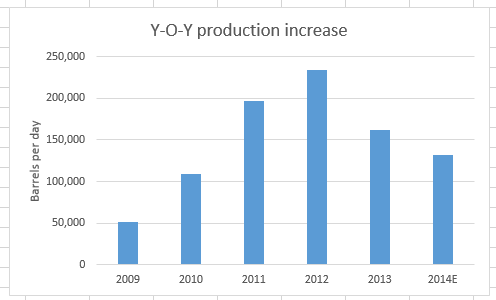

Note: The 2014 production increase is an estimate based on both current average monthly production increase, which is 11,000 barrels per day, as well as a forecast based on continued production per existing well decline continuing at an average of 0.7% per month. The 2014 production per well rate in the first graph is based on the first two months of the year only, therefore likely to change in time.

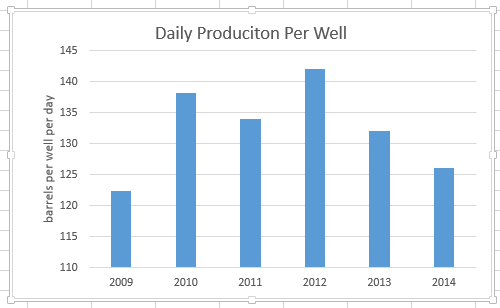

We are now twenty months past the peak in production per well, when 144 barrels per day were produced per month in June 2012. For February 2014 average production per well was 126 barrels per day.

If this monthly rate of decline will continue, production per well by the end of this year will already drop to about 117 barrels per day. That means year-on-year production increase from the Bakken will be about 140,000 barrels per day this year. It is quite a drop from the best year-on-year increase we had, which happened in 2012, which was 234,000 barrels. In 2015 the year-on-year increase in production will be less than 130,000 barrels per day. I am basing this on a revision of the number of wells being drilled this year and next to 1,800, due to the fact that last year fewer wells were drilled than most people, including myself anticipated. Last year when I wrote on this subject, I assumed that 2,000 wells would be drilled on average each year. If there were to be a sudden increase in wells drilled, the situation would change for as long as the increased drilling pace will last, but I do not foresee such an increase in activity.

The main causes of decline:

The main factor contributing to this decline is a simple and obvious one, which I identified in the last article as well. In the 2009-12 period there was a year-on-year increase of total producing wells in the 50-60% range. In 2013 however, the year-on-year increase in total wells dropped to just over 30%. This rate will continue to decline and production per well will continue to decline with it.

The other factor, which currently plays a relatively significant role, and will likely be more important in coming years is the decline in initial production volume per new well. It is forecast by the EIA to drop from 435 b/d in 2013 to 414b/d this year. That is a decline of about 5%. As companies continue to exhaust the sweet spots in the field and are forced to tackle increasingly inferior quality reserves, the negative effect on total production per well will intensify.

We should keep in mind that none of this is to be taken as a sign that the field is close to reaching its peak. A peak will be reached many years from now. The reason why it is important, however, to acknowledge the current trend is in order to understand that the era of spectacular increases in Bakken production ended in 2012 and the annual increase rate will be smaller and smaller going forward in the absence of a sudden and unlikely surge in drilling activity.

Implications for the economy.

Since 2008, shale liquids production provided for roughly half of all global liquid fuels production increase. It can be argued that one of the reasons behind this fact is the geopolitical situation which disrupted supplies from some OPEC members such as Libya and Iran, therefore geopolitics is the only reason why continued growth in liquid fuels supplies has become so dependent on US shale oil production gains. Regardless of the reasoning behind this fact, it still remains the reality of the past half decade.

As I pointed out on many other occasions, the current long-term relationship between liquid fuels supply growth and economic growth, based on past data can be expressed as follows:

1.5% yearly efficiency gains + 2 x percentage growth in liquid fuels supplies = total global potential GDP growth.

In other words, every 1% gain in liquid fuels supplies yields a 2% gain in potential global GDP growth, on top of the 1.5% gained through increase in efficiency. Based on this, we can reasonably claim that since 2008, the increase in US shale oil supplies, which added about 3% to global liquid fuels production, added about 6% to global GDP growth for the 2008-13 period. So, if the shale oil boom would have not happened and all else were to be the same, the world's economy which grew at an average yearly rate of about 3% during this period, would have only managed about 2% on average each year.

There has been a major effect on the US economy as well as a direct result of this increase. It narrowed the yearly trade deficit by about $100 billion since 2008, which on its own translates into a 0.2% yearly increase in GDP. There is also the effect on employment with hundreds of thousands of jobs directly or indirectly created through the new economic activity.

The Bakken and Eagle Ford are the two fields responsible for most of this beneficial trend. There is more and more evidence unfortunately that the trend is starting to dissipate. There are currently no other fields ready for prime time. The Cline shale in Texas needs an average price of $100 a barrel to break even on production, which essentially means that unless the price of production will decline very significantly, only limited development of the field will ever take place.

There was much hope that the Monterey field in California would start to contribute soon, but the reality is that the technical challenges are currently just too great to overcome (link). Meanwhile, the two fields responsible for positively impacting the economic fortunes of the US and of the world for the past half decade are slowly retreating from their role as leading providers of fuel for the global engines of growth. It seems few people are able to get past the years of euphoria created by the spectacular rise in production and realize that we are entering the phase of winding down and soon reversing course.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.