Annaly Capital Management, Inc. (NYSE:NLY) is one of our holdings in the Galt’s Long-Term Portfolio. NLY is organized as a Real Estate Investment Trust (REIT) for tax purposes. This means they pay out 95%, or more, of taxable profits to unit holders (shareholders). As an REIT, NLY does not have any tax liability.

Annaly Capital Management, Inc. (NYSE:NLY) is one of our holdings in the Galt’s Long-Term Portfolio. NLY is organized as a Real Estate Investment Trust (REIT) for tax purposes. This means they pay out 95%, or more, of taxable profits to unit holders (shareholders). As an REIT, NLY does not have any tax liability.

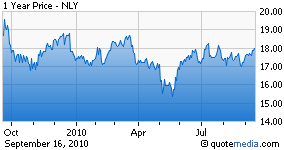

Unit holders receive a K-1 in the first quarter of the year, with their share of company expenses that can be deducted against the income paid quarterly. NLY currently yields 15.5%.

The interesting thing about this REIT is that they don’t own or invest in real estate. They invest in real estate mortgages. NLY buys government backed (guaranteed) mortgages. Their business model is to borrow money for one or two percent interest, and buy mortgage backed securities (MBS) that pay 4, 5, or 6% interest. That is a nice business since they only buy securities that have the government guarantee. Why chase yields if you can make money with no risk?

NLY then takes their business model one step further; they may leverage the portfolio eight times or more. Again, all securities have government guarantees. This is a great business model that has paid our subscribers handsomely over the last two years.

We believe NLY will be announcing their quarterly distribution on Monday (Sept. 21), with the ex-dividend date following by a couple of weeks and payment in the fourth week of October. Before you think, “Boy, I better buy some NLY tomorrow,” keep reading. NLY is a great company, but the timing may not be right.

We have a sell on NLY. Why would we recommend selling such a great performer? First, a little history is in order. We have owned NLY twice in the last two years. We sold it last March for a 53% return in one year, then bought it back in May and are ready to record a 23% gain in four months!

We are concerned about the interest rate spreads NLY is currently able to produce and because of the low current mortgage rates, refinances. Every time a homeowner refinances the loan is converted from a higher rate to a lower rate. NLY’s portfolio is being turned over faster than planned and we believe there may be a surprise in their earnings announcement.

NLY is still a great company, and we will keep them as a future buy recommendation candidate, but for now we would rather sit on the side lines counting our money than have the exposure to the stock price if the earnings are impacted by re-finances.

Annaly publishes a monthly commentary that is insightful in all things economic. In the September 10 Salvo, they wrote:

Long-run monetary neutrality is an uncontroversial, simple, but nonetheless profound proposition. In particular, it implies that if the FOMC maintains the fed funds rate at its current level of 0-25 basis points for too long, both anticipated and actual inflation have to become negative. Why? It's simple arithmetic. Let's say that the real rate of return on safe investments is 1 percent and we need to add an amount of anticipated inflation that will result in a fed funds rate of 0.25%. The only way to get that is to add a negative number--in this case, --0.75%.

To sum up, over the long run, a low fed funds rate must lead to consistent—but low--levels of deflation.

Bernanke said in his Jackson Hole speech that his goal, if necessary, would be to make the markets think that the Fed would keep rates low for longer than expected. Kocherlakota (Minneapolis Fed President Narayana Kocherlakota) says that this prophecy will become self-fulfilling, becoming precisely the thing that will cause deflation, not simply prevent inflation. If ultra-low rates become entrenched, deflation is actually necessary for investors to reach their required rate of return on risk-free assets. This sounds exactly like Japan, where a deflationary mindset has become entrenched. This is part of the reasoning for committing to low short rates, but also including an inflation target or specifying a timeline for zero rates. Both would have the effect of keeping inflation expectations positively anchored if they began to turn negative. With the economy weakening again, the risk of deflation may be more real than the Chairman let on in his Jackson Hole speech.

This is a take on the inflation-deflation economic argument that is worth our consideration. To repeat, "over the long run, a low fed funds rate must lead to consistent—but low--levels of deflation."

We will be mindful. Fed’s serve…

Disclosure: No position