Disciplined value investors look for meaningful divergences between stock prices and business fundamentals. We wait patiently for situations where transitory influences inject unwarranted fear or euphoria into a stock price. We believe the recent drama surrounding Iteris' delayed 10-k has created one of these opportunities.

Our research indicates Iteris' 10-k was delayed due to a mix of bad luck and poor execution; however, we do not see this delay being a harbinger of further bad news. We believe the accounting issue is contained entirely to the timing of revenue recognition between certain quarters. Our research indicates the financial data on the existing cash flow statements and balance sheets are accurate and will not be adjusted. We believe the amount of revenue that is potentially categorized in the wrong quarters is less than 2% of total revenue.

We believe Mr. Market has overreacted and is ignoring the positive fundamentals of the underlying business. Investing in companies with accounting issues can seem like a daunting proposition but investors should take comfort that ITI has been a public company for 19 years and it has generated positive free cash flow each year for the past 7 years. We have spent considerable time with the CEO, Abbas Mohaddes (CEO since 2007, owns 2.7% of the shares outstanding) and all of our background checks indicate that Mr. Mohaddes is highly respected in the Southern California business community.

While the accounting snafu is disappointing, we don't think this matter impacts the intrinsic value of Iteris. The underlying business is experiencing fundamental strength despite what the stock chart says. With the stock trading below book value and a pristine balance sheet ($20m in cash and zero debt), we think the current stock price offers an attractive risk/reward opportunity. We estimate the intrinsic value for ITI is $2.40 per share or +55% upside.

Company Description:

Iteris, Inc. (NYSEMKT:NASDAQ:ITI) provides intelligent information solutions to the traffic management market. The company develops and applies advanced technologies and software-based information systems that reduce traffic congestion, provide measurement, management, and predictive traffic and weather analytics to improve the safety of surface transportation systems.

ITI derives 46% of its revenue from the Roadway Sensors segment. This segment provides various cameras, detection devices, processors, and systems used for traffic management systems. The customers for the Roadway Sensor segment are traffic installation contractors, government agencies, and independent distributors. ITI's proprietary products and entrenched position with these customers provides a competitive advantage and allows the business to earn attractive gross margins in the 40-45% range.

ITI derives 46% of its revenue from the Transportation Systems segment. This segment provides local, state, and federal agencies with traffic management services such as traffic engineering, traffic control, and transit system design. Transportation Systems also provides design, implementation, and operation of traveler information (511) services. The Transportation Systems segment is a steady business that offers a predictable revenue stream with gross margins in the 30-35% range and operating margins in the 10-15% range.

ITI derives the remaining 8% of its revenue from the iPerform segment. This segment provides traffic and weather-related data and analytics software to public and commercial customers. The business aims to utilize a software-as-a-service model and management expects the business will be able to generate gross margins of ~60%. While iPerform has the potential to be a significant growth driver, it currently generates an operating loss of ~$1.5m. We believe this performance can (and should) be improved. Removing this drain on the company would almost double EPS.

Accounting Issue Is Overblown

The "tension" in the stock is due to the company missing the deadline for filing its FY 2014 10-k. We believe this issue will ultimately prove to be a non-event. In typical manic fashion, Mr. Market has dramatically overreacted to the past several weeks. Below is a timeline of the pertinent events:

10/9/2013: James Miele (joined Iteris in 2001) notifies ITI that he will be resigning effective November 1, 2013 to become the CFO at Altura Communications. Craig Christensen (Controller since 2012) is named interim CFO.

12/4/2013: Iteris names Chuck McBride as the new CFO.

1/28/2014: Iteris reports Q3 2014. It's the company's first quarter with Chuck McBride at the CFO helm.

6/25/2014: Iteris announces that it will delay reporting Q4 2014 results, which had been scheduled for June 26th.

6/30/2014: ITI files NT 10-K indicating the FY 2014 10-K will not be filed with the SEC by the required deadline.

7/15/2014: Iteris announces that it will not be able to file its FY 2014 10-K by the July 16th extension deadline. ITI also announces that the recently-hired Chuck McBride has "resigned" as CFO. Our research indicates McBride was terminated following his inability to properly close the books in Q4 and support the FY 2014 audit. Craig Christensen is again named interim CFO.

7/16/2014: Iteris provides preliminary financial results for Q4 2014 and some context on the potential revenue recognition issue.

While this saga certainly has all of the makings of a classic stock market train-wreck: small cap stock, CFO turnover, accounting questions, etc. As we will detail below, the reality of the situation could not be more benign. Investors should take comfort that ITI has been a public company for 19 years and it has generated positive free cash flow each year for the past 7 years. We have spent considerable time with the CEO, Abbas Mohaddes (CEO since 2007, he owns 2.7% of the shares outstanding) and all of our background checks indicate that Mr. Mohaddes is highly respected in the Southern California business community.

Regarding the audit, our research indicates the 10-k was delayed due to a mix of bad luck and poor execution. McGladrey has been Iteris' auditor for the past nine years. Unfortunately, the two senior managers at McGladrey that cover the Iteris audit both had serious health problems just as the audit was commencing (bad luck). McGladrey had to staff the audit with a new team that was unfamiliar with the intricacies of Iteris' business. To make matters worse, it was Mr. McBride's first audit with the company and he proved to have a steep learning curve as well (poor execution).

Our research indicates that in mid-May, a revenue recognition question was flagged related to ITI's use of percentage-of-completion accounting for a contract(s) in the Transportation Systems segment. We believe this issue pertains to less than 2% of the total company revenue. Our research indicates the revenue recognition question only impacts the timing of revenue and has absolutely no impact on the total amount of revenue. Our research also indicates the financial data on the cash flow statements and balance sheets is correct and will not be restated. It is our understanding that McGladrey has not raised any concerns over prior years' financial statements. We also believe there is no disagreement between Iteris and McGladrey.

Iteris released preliminary financial results for Q4 2014 on July 16th, which provided some context on the scope of the accounting questions. The range provided for cash balance, total assets, total liabilities, and total stockholder equity all suggest this accounting issue is contained solely to revenue recognition. The Q4 results implied in the FY 2014 preliminary results show the amount of revenue recognition in question is very small (less than 2% of total revenue) and the underlying business continues to grow and experience strong fundamentals. It was this information that dramatically increased our level of conviction surrounding this buying opportunity.

Niche Market Leader with Solid Growth and Recent Contract Wins

Iteris competes in the niche market of traffic technology and solutions. Our research indicates ITI is the market leader in its space. Iteris competes primarily against Econolite, FLIR Systems (NASDAQ:FLIR), and Imaging Sensing Systems (NASDAQ:ISNS). Iteris roadway sensor solutions also compete against legacy loop systems that use induction loops installed in the payment. The roadway sensor technology that ITI provides is less expensive and easier to install than traditional legacy loop systems. Legacy loop systems can be unreliable for bicycles, scooters, motorcycles, and some small cars. The replacement of loop systems with roadway sensor is a large secular tailwind for Iteris.

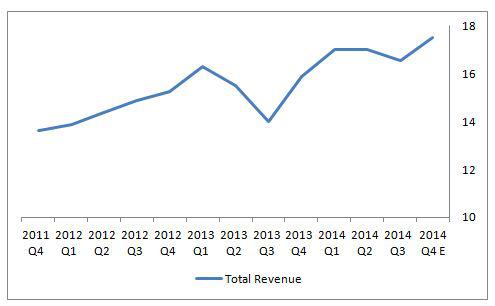

More broadly speaking, "smart" traffic management is a growth industry as more vehicles flood the roadways. Iteris is well-positioned to benefit from this secular growth and its success is evident when looking at the recent revenue levels. According to the Q4 2014 preliminary results, Q4 will be a record quarter in terms of revenue.

Source: Iteris

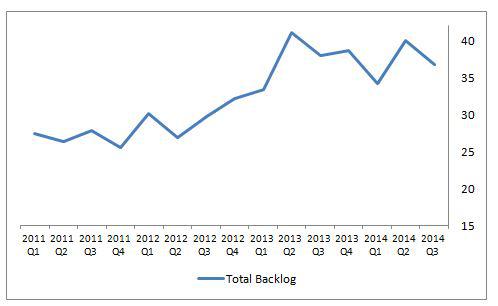

The fundamental strength at Iteris can also be seen via the growth of the backlog.

Source: Iteris

Recent contract wins suggest Iteris solutions have momentum; this should bode well for FY 2015 performance.

6/14/2014: Iteris to Help Power the I-95 Corridor Coalition with Performance Measurement and Traffic Analytics

6/23/2014: Iteris Enters into Precision Agronomy Weather Agreement with Agrian

Additionally, international expansion should provide growth opportunities for the foreseeable future.

Stock Price Significantly Undervalued Following Recent Drop

With the stock down -29% YTD and -40% from its peak in mid-January, we think Mr. Market has overreacted and served up a compelling buying opportunity for discerning small-cap investors.

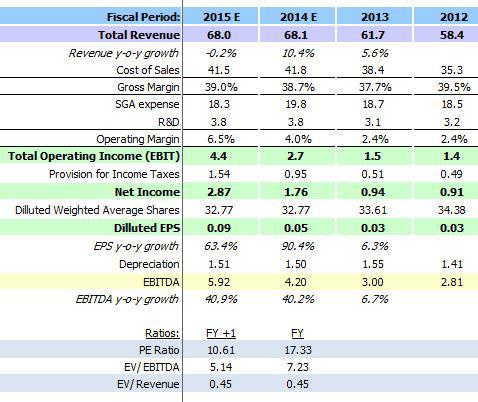

Following the recent drop, the stock is now trading at 7.23x EBITDA and 17.3x earnings (after adjusting for cash balance of $20m or $0.62 per share), which is a significant discount to its 10-year historical multiple of 13.4x EBITDA and 21x earnings.

Furthermore, ITI is currently losing ~$1.5m per year from the iPerform segment. If we assume that ITI eventually stops the bleeding and divests or right-sizes iPerform, the stock is trading at only 5.1x EBITDA and 10x earnings based on our estimates for FY 2015 (the current fiscal year).

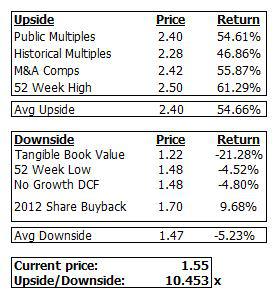

If we apply the historical multiples to ITI, fair value for the stock is $2.28 per share.

Source: Iteris & author estimates

ITI is also trading at a significant discount to its peer group, which is trading at a median EV/EBITDA multiple of 11.9x, EV/Sales of 1.02x, and PE ratio of 19x. If we apply the peer group multiples to ITI, fair value for the stock is $2.40 per share.

Source: Capital IQ

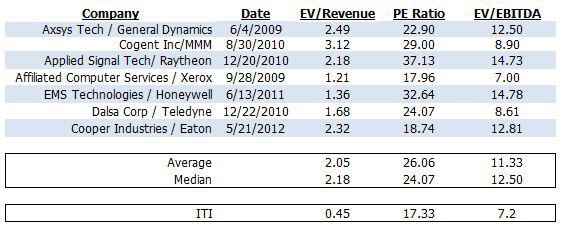

We analyzed M&A deals for comparable companies and found that ITI is trading at a meaningful discount to the valuation multiples of these transactions. The average M&A deal was done at 11.3x EBITDA and 26x earnings. If we apply the M&A group multiples to ITI, fair value for the stock is $2.42 per share.

Source: Bloomberg

We believe the stock offers a compelling 10:1 risk/reward profile. We see the risk of further downside being minimal as the stock is already at or below several of our traditional downside indicators. ITI has a Book Value of $1.75 per share and the company bought back a significant amount of stock at $1.70 per share, which implies that they see value in the stock at that price. Our research indicates the company has an active buyback plan in place, which we expect to help provide support for the stock.

Potential Acquisition Target

We think the current stock price is unsustainable; either the stock will migrate back above $2 per share or some entity will make a play to acquire the company. We think several natural buyers exists that would likely be willing to pay $2.50+ per share given the existing revenue run rate, entrenched customer relationships, brand recognition, intellectual property portfolio, and potential cost synergies. Our list of most likely suitors includes FLIR Systems, Econolite, Google, IBM, Accenture, Cubic Corp, Xerox, and Verint Systems.

With the stock price currently valuing the entire enterprise (market cap less cash) at only $30m and 5.1x potential EBITDA, we think it is possible that a private equity firm could also make a play for ITI.

Conclusion

The accounting drama sounds scary but when you peel back the layers and dig into the facts, we believe the issue is trivial in size and fully contained to the timing of revenue recognition between quarters. There is an awful lot of fear and pessimism baked into the current stock price (delayed 10-K, CFO fired, Sidoti downgrade) and we believe as things get sorted out, the stock will revalue higher. ITI provides consistent free cash flow generation; last year's audited free cash flow yield for ITI was almost 9%. Over the past 6 years, ITI has generated an average of $4.4m in free cash flow. This amount of FCF is compelling for a company with an entire enterprise value of only $30m (equates to an average FCF yield of 14.5%).

While the accounting snafu is disappointing, we don't think this matter impacts the intrinsic value of Iteris. The underlying business is experiencing fundamental strength despite what the stock chart says. With the stock trading below book value and a pristine balance sheet ($20m in cash and zero debt), we think the current stock price offers an attractive risk/reward profile. We estimate the intrinsic value for ITI is $2.40 per share or +55% upside.

Disclosure: The author is long ITI. The author wrote this article themselves, and it expresses their own opinions. The author is not receiving compensation for it (other than from Seeking Alpha). The author has no business relationship with any company whose stock is mentioned in this article.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.