Week in Review

The holiday week in the U.S. markets was short on trading sessions and light on economic data, but it wasn't short on action. This week isn't likely to be so quiet.

Stocks: The major U.S. indexes advanced smartly last week, paced by a 3% rise in the NASDAQ 100. The Dow Industrials reached a new three year high at 12,505.99 (but it was not confirmed by the transports). We saw the SPX and NDX both gap up on Thursday and Friday. Volume remains on the modest side but not unusual at all. The VIX and put/call ratio both fell as breadth indicators turned bullish. After a few weeks of defensive sector leadership, growth oriented sectors moved out in front with the techs gaining nearly 3%, followed by materials and energy. Big moves in Apple (AAPL) and Intel (INTC) shares set the tone for tech. On the other hand, financials continue to struggle. Most major foreign stock markets also enjoyed broad advances.

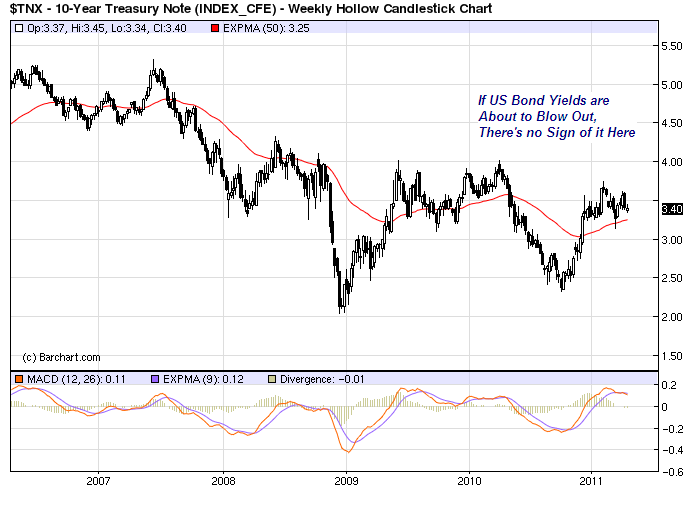

Bonds: Short term Treasury yields fell but yields on longer maturities hardy moved during the week. TIPs, municipals and corporate issues were also little changed. There just wasn't much action of note in the bond market, despite all kinds of bearish analysis and even the occasional apocalyptic vision.The world may yet collapse on bond investors, but it didn't last week.

Commodities: Like stocks, the CRB index picked up some ground, remaining in a rising trend channel. WTI crude added 2% to finish the week above $112 a barrel, but the bigger advance came in natural gas, up more than 5%. Grains, gold and copper were also on the plus side, and silver gained another 8.4% as it continues to go parabolic. Meats and softs were off marginally.

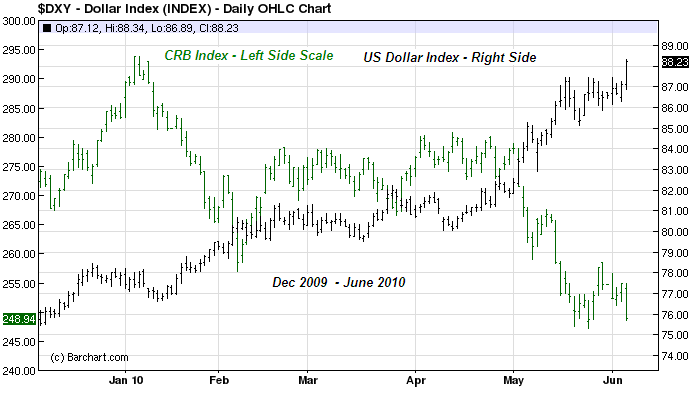

Currencies: After rising to 75.81 on Monday, the U.S. Dollar index fell sharply through the week, reaching as low as 73.73 before recovering to finish at 74.09. If you're looking for an explanation for the action in stocks and commodities last week, you could do worse than to look here. The index looks ugly, there's no other way to describe it. Several forex charts looked remarkably like stock index and commodity charts: several gaps up to reach new highs, with a few reversals at the end of the week.

The Week Ahead

Stocks: To this point earnings season has brought pretty good numbers on balance. Market reaction has been mixed. Earlier we noted the positive reaction to blue chips Apple and Intel; Travelers (TRV) is another notable example, but others such as GE and McDonald's (MCD) weren't so well received. Our theme of watching earnings, and the market's reaction has been reliable on balance, but the SPX remains below 1340 and ran out of short term momentum on Thursday.

For the coming week my position on stocks is still to be patient and wait for a clearer signal on the next major directional move. We have bullish bias in a number of stocks and sectors, and both earnings and economic data are positive, but I would like to see a little more follow through and new highs on the broader indexes before going with a buy call. That may mean missing a few points of upside, but to me this is like an insurance cost.

Click to enlarge

Bonds: What little there was to say about bonds in the short term, we've already said. Hold 'em if you got 'em is my approach here, but I'm not adding to positions at this point. Yields aren't very attractive, but a lot of the bearishness seems overwrought. The coming week will bring a heavy dose of economic data: housing, personal income and spending, consumer sentiment, GDP, Chicago PMI. There is plenty of potential to move rates and markets, so it's not likely this week will be as quiet as the last.

Click to enlarge

Commodities: Thanks to a stumbling U.S. Dollar, the commodity bull just keeps rolling along, vexing policy makers and many traders alike. WTI crude, which is rising again (in spite of ample supply) as of this writing, looks vulnerable to correction - but again much will depend on the Dollar. The futures are in contango through year end, backwardation beyond. Natural gas looks like a better long trade. It has made a higher bottom and turned back up with building open interest. We saw a similar type of move last fall, only to have it fail in the new year, so we can't get too excited just yet, but a move above $4.55 would be very positive. Gold and especially silver are pure momentum plays, and very dangerous. Long positions should be watched carefully for the first signs of trouble. When these moves reverse it will be fast and furious.

Click to enlarge

Currencies: The U.S. Dollar index reached a three year low. The last time we saw these levels, in Q4 2009, the index put in a bottom and rose to 88, coinciding with sharp corrections in both commodities and stocks. Technically, there is little evidence yet that the Dollar is putting in a bottom, but we need to watch for the possibility. If it does, then we will have to review our positioning.

Click to enlarge

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.