This oil market reminds me of a surrealist Dali painting. It just seems all warped, distorted and twisted out of shape. Here’s what I mean:

Want some oil delivered in the future, say a year from now? Take your pick.

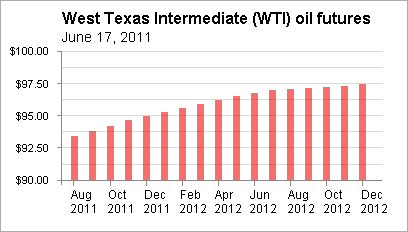

If you want West Texas Intermediate (WTI) crude, get ready to pay up. Sure it’s cheap, but oil for delivery in a year costs about $3 more per barrel. The market’s in contango, a sign of plenty of supply, so there’s a storage premium as you can see here.

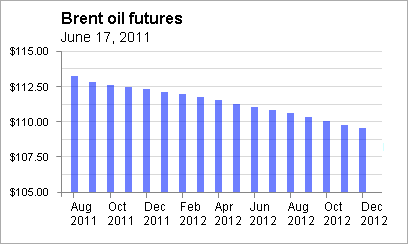

If you want Brent crude, you’re actually in luck. Yes, it’s more expensive and yields less energy, but delivery in a year would actually cost you about $2 less per barrel as shown on this chart.

That’s backwardation, of course. That signifies a tight market, where oil commands no storage premium. Unlike WTI, people want their Brent now and are willing to pay up.

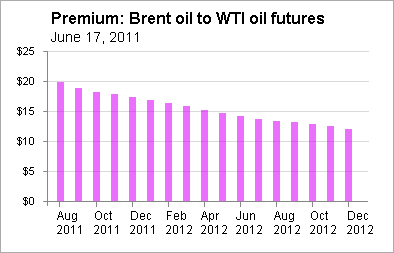

The net result is that the spread between Brent and WTI for August delivery reflects a $20 premium for Brent – a spread that’s usually negative, but those same two oils 18 months out are “only” $12 apart.

So essentially the spread between Brent and WTI is in its own weird backwardation as you can see here.

Arbitrage between Brent and WTI is somewhat difficult now with a bunch of oil stuck in Cushing, which I wrote about last week.

Arbitrage between Brent and WTI is somewhat difficult now with a bunch of oil stuck in Cushing, which I wrote about last week.

This is going to take some time to resolve, I guess, but unless these two oils dance together – either both in contango or both in backwardation – WTI just isn’t going to be a reliable indicator of what oil really costs worldwide, making it harder to figure out what gasoline and other distillates should sell for.

Trading Between Two Crude ETFs?

Two ETFs that invest in oil futures contracts are USO (for WTI crude) and BNO (for Brent crude). Each ETF invests in near-month contracts and rolls them out every month. They perform best when markets are in backwardation.

For example, when USO rolls out its contracts into the next month, that eats into returns because next month’s contracts are more expensive. With BNO, you have backwardation working for you because you’re selling this month’s contract and buying next month’s cheaper.

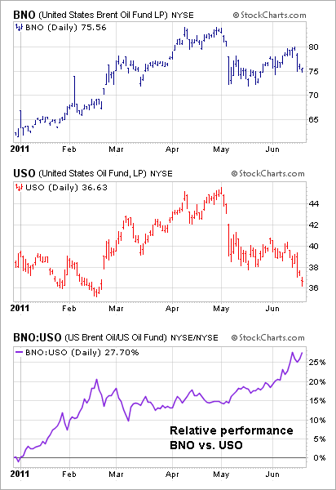

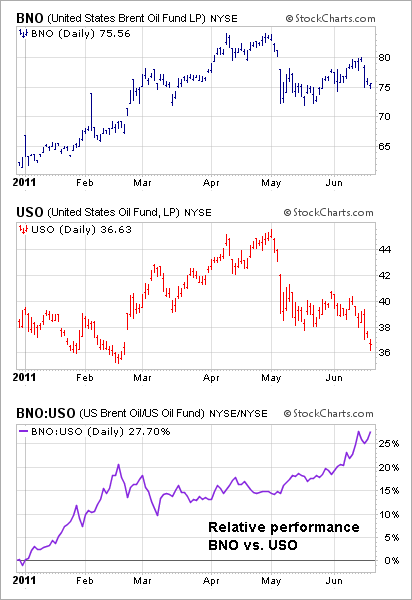

Although it’s tempting to consider a long USO/short BNO trade to take advantage of any narrowing of the spread between WTI and Brent, I’d be cautious. I may be late to the party, but long BNO/short USO has been the better move at least year to date as you can see here.

Click to enlarge

At the very least, I certainly would not be shorting BNO. One additional reason is that this ETF isn’t really all that good a trading vehicle anyway. Based on average three-month volume, USO is 100 times more liquid than BNO. Although volume has been perking up, it looks as if most days, only a few thousand shares might trade in a given hour in the middle of the day.

I hope this fund perks up more – especially if Brent is going to become some sort of a new oil benchmark. There’s another Brent ETF (OILB) run by ETF Securities that seems to be more liquid, but unfortunately, it doesn’t trade in the U.S.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.