We are into year 6 of the recovery and risk/reward picture for the multi-industry sector, and in particular General Electric (NYSE:GE) is more positive now than it was a year ago. Consensus likely became too negative on short-cycle industrial and oil & gas related demand; these are the two key areas where we could see significant swing in sentiment in 2015. Companies that are exposed to attractive end markets can avail themselves of self-help margin opportunities, and that enjoy balance sheet flexibility should outperform in 2015.

Low Oil Prices And GE

Among others, the three important questions that investors should ask themselves before investing in GE in 2015 are 1) how will the lower oil prices impact earnings, 2) what are the impacts of a strong USD, and 3) how sustainable is the dividend? The multi-industry sector is largely a pro-cyclical group and given the net economic benefit from lower oil prices, one has to view it as aggregate net positive for the sector. Lower oil prices basically mean a transfer of wealth from producers to consumers and consumers are more likely to spend a windfall than producers. This should help boost global growth.

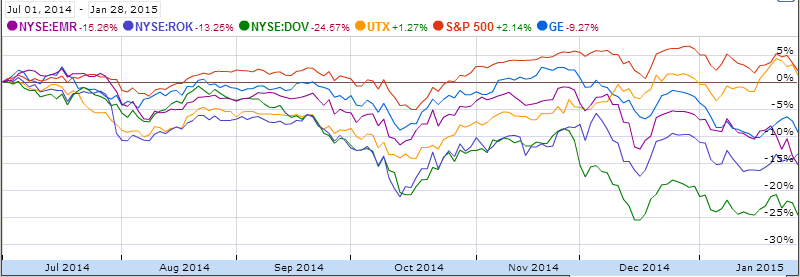

However, these are the medium-to-long-term impacts. The immediate impact of a correction in oil price is usually negative for the sector. As you can see from the chart below, General Electric, Dover Corp (DOV), Emerson Electric (EMR), Rockwell Automation (ROK), and United Technologies (UTX) all underperformed the S&P500 since July last year. This is normal during supply driven corrections. However, capital goods growth is positively correlated with global growth and lower oil prices should eventually prove to be net positive for the group.

Having said that, the stocks, such as GE, which are over-indexed to energy capex are still likely to underperform the rest. While GE is less exposed to oil & gas capex than many other companies, such as DOV or ROK or EMR, still the company has significant exposure to the oil & gas sector. The past super-cycle downturns, such as defense, agriculture, and mining tell us that multiple of the companies with greater exposure will remain discounted vs. historical averages, until the market moves beyond the point of negative sales momentum.

Source: Google Finance

GE's Aggressive Oil & Gas Guidance

Despite negative 4Q14 orders and pricing headwinds in 2015, GE has maintained its flat to -5% organic growth outlook for oil & gas in 2015. There is no doubt that the oil environment is weaker than what GE forecasted at its December analyst meeting. The company is taking aggressive steps to cut costs, but I think its growth outlook is a little too optimistic given its subsea/drilling exposure. Drilling orders were down 72% in the fourth quarter.

As I mentioned earlier, the overall earnings risk for GE is unlikely to be as significant as for the oil-rich peers like Dover and Rockwell Automation; low oil prices will hurt the results for the oil & gas segment nonetheless. Equipment orders in the most recent quarter were down 15% and service orders were down 4%. The company believes that the challenging oil and gas environment is manageable and is taking steps to help offset the impacts of lower oil including restructuring, headcount reduction, and simplification. In its power segment, GE has shown its ability to absorb sharp declines in customer capex; however, I believe the company is being too optimistic and oil & gas pricing remains a risk in 2015 as customers seek to share the pain of lower oil prices.

Strong USD

Another major theme for 2015 is the strong U.S. dollar. The USD continues to gain strength and the outlook for Fed tightening and the announcement of $1.1 trillion quantitative easing program by the European Central Bank mean that this trend is likely to continue in 2015. The euro is trading at significantly below its historical average. While it is difficult to predict when the U.S. policy makers will decide that the USD has strengthened too far and intervene, the strong USD does have implications for the sector, including GE.

First, a strong USD impacts the foreign earnings currency translation. According to Morgan Stanley estimates (report published January 12, 2015), a strong USD is expected to have an impact of 250bps on revenue/EPS (based on a $1.2 euro rate). A strong USD also impacts competitive dynamics across the global capital market goods. A weaker euro and Japanese yen will make both Japanese and European capital-rich companies more competitive in export markets. This could also lead to price-based competition in export markets, especially for large capital equipment orders.

GE's Credibility Issues

Aside from the above-mentioned themes, the biggest issue with GE right now is one of credibility. The company has been making promises and assuring investors it will deliver on them for some time now, but so far it has been unable to make good on these promises. GE's gross margins have fallen by 200bps in recent years. Recently GE expanded its cost-cutting initiatives beyond SG&A to include COGS in a move to give a boost to margin outlook for its industrial businesses. The second wave of simplification the company unveiled in December and the reduced headwinds from the business mix should make it relatively easier for GE to hit its margin expansion target, but it remains uncertain how much traction can be gained in one year given the headwinds in power & water and oil & gas.

Simplification wave 1, which was focused on SG&A, is bearing fruit, and this combined with efforts to expand gross margins should help GE to grow earnings even as the top-line outlook for both oil & gas and power & water remains weak. The scope for the company to reduce its direct spend in COGS, particularly direct materials costs, remains significant. There is also scope for meaningful savings from the manufacturing footprint, keeping in mind GE's weak sales per facility performance compared to peers in recent years. However, execution remains important and this will be a key acid test for GE in 2015.

Dividend Provides Downside Protection

Despite the macro challenges and delivery issues that have mired GE in recent years, the company continues to offer a sector-leading dividend yield of 3.9%. This is compared to the industry average of 2.3%. Though there are some concerns about the sustainability of the dividend, given weak industrial free cash flow generation and a downside bias to the GE Capital dividend, I think the continued portfolio actions, margin improvement, cost-cutting initiatives, and successful integration of Alstom should help GE address these concerns. While there is little likelihood of a material dividend growth for the next two years, at the same time I do not think GE's dividend is vulnerable.

Another Okay Quarter

General Electric reported another okay, largely in-line quarter. Expectations were already low before the earnings release, and that situation does not seem to have changed post earnings. Post earnings, the stock did not move much in either direction. As I have stated in my previous articles on GE, this tells us that a large section of the market, particularly institutional investors, has lost interest in GE. The market is indifferent to GE's earnings reports. As one Barclays analyst noted in his report (published January 23, 2014) "GE probably could have dropped a bomb on us today and it wouldn't matter much."

The slower growth in the quarter was offset by better than expected industrial margins and higher earnings from GE Capital. The company's restructuring efforts are bearing results, as is evident from the 50bps increase in industrial margins. General Electric remains on track to reach its 17% industrial EBIT margin target by 2017. However, the margin expansion could decelerate in 2015 driven by headwinds in power & water and margin contraction in oil & gas.

Conclusion

While a strong USD and oil prices weakness present headwinds for GE in 2015, at the same time an almost 4% dividend yield, which is meaningfully higher than its peers, provides downside protection. I agree that GE has failed to deliver in the past few years, but GE of today is different and largely it's because the market today is different than it has been in the past several years. Moreover, the company's muted EPS growth is no longer way below its peers.

GE has more oil and gas exposure than its peers, and sure there will be headwinds, but the company has shown in its power segment that it is able to absorb sharp declines in customer capex budgets. Moreover, on the positive side, the company has more exposure to end markets, such as medical, aerospace, and transportation, which are expected to perform well in 2015. I believe the company needs to earn back its lost credibility to see a meaningful improvement in share performance, and in this regard GE not only needs to deliver on its targets but also needs to shrink the size of its finance business. GE does not have a competitive advantage in its non-captive financing businesses and it is unlikely investors will ever pay a premium for this segment. However, in the meantime, the company continues to offer a healthy dividend yield of 3.9%.