In my two PRO-articles on Newstrike Capital (OTCPK:NWSKF) I explained why I thought the company was 'in play' as it was one of the last remaining advanced stage projects in the Guerrero Gold Belt which wasn't owned by a much larger company. My suspicions have now been proven true as Timmins Gold (TGD) has announced an offer to acquire all outstanding shares of Newstrike Capital. In this article I will briefly advise what the Newstrike-shareholders should do.

A. The offer

Newstrike had been up for sale for quite a while, but I admit I'm surprised Timmins Gold made an offer as I would have expected one of Newstrike's direct neighbors to have the best chance to make a successful bid.

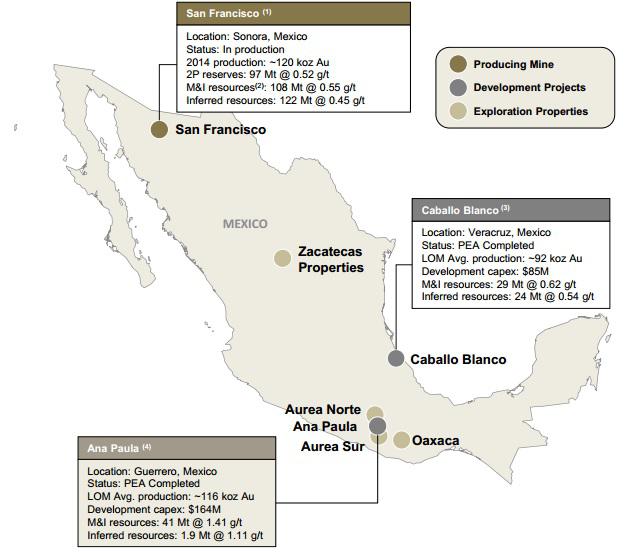

Source: company presentation

Timmins offers to acquire Newstrike by issuing 0.9 new shares of Timmins and C$0.0001 in cash (or fiscal reasons) per share of Newstrike. This originally was a 20% premium but as the offer was announced on what was a terrible day for the gold price, Timmins' share price went down and the premium disappeared. The deal pretty much seems to be a 'done deal' as the Lundin family,which is Newstrike's largest shareholder, has committed to tender its shares to Timmins Gold and on top of that, the Lundin trust will participate in a private placement conducted by Timmins Gold at a premium of the current share price.

B. Is it a fair offer?

A lot of Newstrike shareholders were unhappy with the offer as the premium was quite low and eventually totally disappeared when Timmins' share price went down. Even thouh I'm a Newstrike shareholder and was hoping for an offer in the C$1.25-1.5 range, I took a step back and based my decision on the bigger picture.

First of all, Timmins is a logical partner as it already has several projects in Mexico of which one is producing at a rate of 120,000 gold-equivalent ounces per year. Needless to say the Timmins-guys have a lot of experience in Mexico and are familiar with all the necessary procedures.

Secondly, Newstrike was facing an initial capital expenditure of in excess of $160M and the dilution to raise some cash for the capex would have been quite severe. This problem/risk is being mitigated by being bought out by Timmins Gold as Timmin' San Francisco project should generate an annual free cash flow of in excess of $20M at the current gold price. So by the time Ana Paula will get built, Timmins Gold will (should) have a nice war chest and should be in a position to avoid further dilution. I think this is an important factor which is being ignored by the majority of the Newstrike shareholders.

Yes, the offered price isn't very high, but I do believe it's a fair offer as the risk perception of the combined entity will drop fast as the financing risk will go down.

C. What action should you take?

I currently own shares in Newstrike Capital and at this point in time I'm leaning towards offering my shares to Timmins Gold. One could always hope some kind of white knight could turn up but I'm not holding up my hope. If you look at the Canadian listing of both companies (which is the most liquid listing as both companies are Canadian), Timmins Gold is trading at C$1.14 which gives the offer a theoretic value of C$1.026. However, Newstrike Capital is trading at a discount to the offered price as its last share price was C$0.98 which means it's trading at a discount of 4.5% to the offered price.

So I do believe owning and holding shares of Newstrike Capital is the best move here. If the deal goes through you'll be able to buy shares of Timmins Gold at a 4.5% discount and if a white knight would suddenly appear, your profit could be larger.

I still hold my Newstrike shares and plan to tender them to the Timmins Gold offer. The offered premium was low (and non-existing right now), but I strongly believe the combined entity will create value.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.