Timmins Gold (TGD) and Newstrike Capital (NWSKF) have announced that both parties have entered into a definitive arrangement agreement, where Timmins will acquire all of the issued and outstanding shares of Newstrike by a way of a court-approved plan of arrangement.

Newstrike will receive .9 of a Timmins Gold common share and $.0001 in cash for each Newstrike common share, which represents the equivalent of $1.15 per Newstrike share, a 20% premium based on Newstrike's closing price on Feb. 13.

I think this deal makes a whole lot of sense for both companies, as the combined company will have a leading growth profile capable of increasing annual gold production by 175% over the next few years, at industry leading cash costs.

While I previously was somewhat bearish on Timmins Gold following the Caballo Blanco acquisition, I now have a more bullish stance on the stock because of this announced deal. Here's an overview of both companies, and why I feel this is a good match.

Timmins Gold

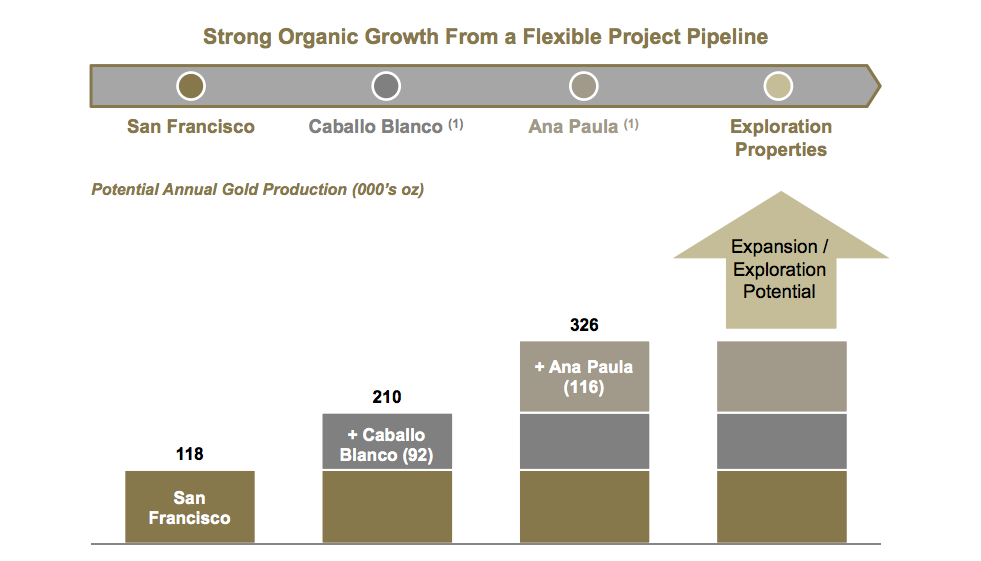

Timmins Gold owns and operates the currently producing San Francisco gold mine and owns the Caballo Blanco project after completing the acquisition from Goldgroup Mining on Dec. 24, 2014, for total consideration of $10 million plus 16 million Timmins shares.

The San Francisco gold mine is an open pit heap leach operation that currently produces 115,000 to 125,000 ounces of gold annually, at cash costs of $717 per ounce. Current reserves at the mine are 1.6 million ounces of gold with 9.5 years of mine life remaining, assuming 122,000 ounces of gold production per year.

Production has increased steadily since 2010, from 47,032 ounces to 2014's record production of 121,573 gold equivalent ounces, while reserves have jumped 170% since 2008, from 611,000 ounces to 1.6 million ounces. All-in sustaining costs are projected at just $843 per ounce for the remaining of the mine life as major capital expenditures have already been committed and spent.

As mentioned, Timmins also owns the Caballo Blanco project, which has close to 1 million ounces in gold resources with exploration upside. Once in production, this mine could add 90,000 ounces of gold production annually, at projected cash costs of $784 per ounce. Even better, initial capital costs are very reasonable at just $84.8 million. On the downside, however, the project still needs permits, which the previous owner Goldgroup applied for but has not received - so this is one risk Timmins was willing to take when it purchased the asset, and one risk investors need to be aware of.

Finally, Timmins has a strong balance sheet, with $50.2 million in cash as of the end of the last quarter, and $11.5 million in debt that was recently refinanced into a $13 million credit facility with Sprott Resource Lending and Morgan Stanley.

Newstrike Capital

Newstrike's 100%-owned flagship asset is the Ana Paula project in Guerrero, Mexico, which was acquired from Goldcorp (GG) in June of 2010. The deposit currently contains a resource estimate of 2.2 million ounces of gold, with life of mine annual production projected at 116,000 ounces over 8 years. Initial development capital is also reasonable at $164 million. At 2.24 g/t gold, this is one of the highest-grade open-pit gold projects in the Americas.

Based on the company's preliminary economic assessment, the Ana Paula project carries a pre-tax net present value of $405.3 million with a pre-tax rate of return of 47.5%, although this is based on a $1,450 gold price. Still, at a $1,300 gold price, the project has an after-tax net present value of $232 million (more than double Newstrike's market cap), and the mine projects cash costs of $527 per ounce, which should result in all-in sustaining costs of under $800 per ounce (includes sustaining capital, exploration, etc.) So Ana Paula looks like it will be quite profitable at current gold prices.

While Newstrike carries a market cap of $101.56 million, the company has just $3.65 million in cash at the end of the last quarter, according to Yahoo Finance, so it was very unlikely Newstrike would have been able to raise the necessary funds to advance Ana Paula to production, without significant shareholder dilution or a debt issuance. Both are risky moves that could destroy shareholder value, in my opinion.

Timmins shareholders also get an exploration portfolio that looks like it has excellent upside potential, especially the Aurea Norte and Aurea Sur exploration properties, which are located adjacent to Ana Paula.

The combined company has the potential to reach approximately 326,000 ounces of annual gold production if the Ana Paula and Caballo Blanco projects are successfully put into production, which is the plan. However, these also happen to be very economical gold mines, with projected all-in sustaining costs to be less than $780 per ounce of gold for all of the combined mines.

Bottom Line: The Deal Makes Sense

For Newstrike, the company gets a takeover at a 20% premium to the company's closing price on Feb. 13, and gets exposure to gold production from the profitable San Francisco mine, plus growth potential from Caballo Blanco. But Newstrike will also be in a stronger financial position following the acquisition, as Timmins has $50 million in cash and operating cash flow from operations that it can use to help develop Ana Paula. Newstrike had less than $4 million in cash at the end of the last quarter, so this solves that problem for Newstrike shareholders.

For Timmins, Ana Paula is a high-quality asset that is added to its portfolio, as the project has a 32.8% internal rate of return at a gold price of $1,300, with projected cash costs of just $486 per ounce, based on the project's preliminary economic assessment. So this gives Timmins a more diverse, high-quality asset base in Mexico which could help the company achieve a new status as an intermediate gold producer. If the new Timmins can successfully get both Ana Paula and Caballo Blanco into production, the share price should rise significantly.

I am still on the sidelines, but after the acquisition goes through, I will look at initiating a position on any pullbacks.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.