Since 1998, Second Sight Medical Products, Inc. (EYES) has been working on implantable prosthetic devices that can restore sight to the blind. Last November, it debuted on the NASDAQ with the intent to use the capital received in the IPO to further develop and market its Argus II System for retinitis pigmentosa [RP] and develop the Orion I visual prosthesis for age-related macular degeneration [AMD] and other causes of blindness. Its outstanding breakthrough technology immediately resonated with retail investors as the stock shot up over 100% over its IPO price but the gains haven't lasted as bearish investors question the company's burn rate, product quality and size of the market opportunity. I believe that this medical breakthrough for the blind is worth billions, particularly in this frothy environment for biotech stocks where companies with no revenue can be worth well over $1 billion in market cap. Second Sight's market cap of less than half a billion presents a tremendous opportunity for investors who want to invest in this disruptive technology that can drastically change people's lives and give people the security of never being in complete darkness as they age.

The market opportunity: cost of vision problems to reach $717 billion by 2050 in the United States

Anyone who believes that the market for EYES is limited because of its specialized approval for RP as an early-stage medical device company is greatly underestimating the effect our society's lifestyle has on our eyes. Diabetes, heart disease and cancer are scorns of humanity and staples of the biotech sector as many companies are working on solutions and monitoring devices to control and detect these diseases. These illnesses have been on the rise as humans drastically changed their behavior from hunter-gatherer societies evolved over tens of thousands of years to the post-industrial revolution era over the past few hundred years which has resulted in a spike of intake of sugar, salts and fats and increasingly sedentary lifestyles. Evolution can't keep up with the change, leading to adverse health impacts.

The way we use our eyes has also drastically changed. Human eyesight was developed over millions of years from predecessor species primarily to spot predators to escape from and prey to hunt. That's the reason why we spot facial patterns so easily in something like clouds, a pile of leaves or the "Face of Mars" when nothing exists - it's an evolutionary survival mechanism. Just like how much of our diet and lifestyle has changed, particularly since WW2, the ways we use our eyes have drastically changed, particularly over the last 30 years, with the rise of computers and smartphones. We have gone from using our eyes primarily to locate things at a distance to a society where more than half of the waking day is spent staring at a screen a few inches to a few feet away from us.

Just as we are dealing with increased health risks now from behavioral changes that really got started in the second half of the 20th century, I believe we are on the cusp of seeing a society with vastly increased eye problems. The online pamphlet titled "Your Phone May Increase Your Risk for Macular Degeneration" outlines the risk from blue light as well as what you can do to help prevent eye problems in the future. This article links smartphone use at night to long-term eye problems as well as other health issues.

A society that is generally living longer will also have vastly increased cases of AMD as it is an age-related disease just like many others we face today. Researchers at NORC at the University of Chicago came out with a report that the cost of vision problems will increase 376% from $150 billion today to $717 billion by 2050 in the United States alone. I believe that an investment in EYES now is akin to an investment in healthcare stocks in the 1980s. The returns will be outstanding over the very long run if you can tolerate the short-term spikes and dips. Second Sight is the first entrant to a market that will give blind people some functional vision. The technology will only improve from here to the point that EYES should be a major player in truly bionic vision that society will need in the future.

Second Sight is undervalued in this hot market for healthcare

When putting together this estimate for EYES, I am aware that there will be people bearish on the stock who will disagree with my conclusions. I refer those people to a recent bearish article of mine on ACADIA Pharmaceuticals Inc. (ACAD). I think ACAD makes a great proxy in which to judge other healthcare stocks as it is a highly liquid stock that has largely been forgiven by the market for its corporate bumbling because of the potential of its drug. JPMorgan has a $40 target on ACAD, implying a $4.4 billion valuation on 110.7 million fully diluted shares that is 50% based on a risk-adjusted DCF model. Within that DCF model lies an assumption of nearly $1 billion of revenue and $660 million of EBITDA in 2017, while the company is submitting the NDA filing to the FDA in the latter half of 2015. I believe that targets on ACAD are too aggressive but the market disagrees with me as the stock price is over $37, almost at JPM's rather bullish target.

I'm cognizant of the fact that ACAD and EYES lie on the opposite ends of the healthcare spectrum. One has a drug to manage psychosis in Parkinson's Disease and the other is a medical device to try to give blind people some vision. But the framework for valuing each company is the same. ACAD doesn't have a penny of revenue now and is expected to reach a billion dollars in 2017. EYES achieved $1.5 million in revenue in Q4 2014 and it will be at least until 2021 before the company comes close to a billion dollars in annual revenue in my model.

If you're bearish on EYES, understand the biotech and healthcare market that we live in. In the context of this biotech "bubble", EYES is not overvalued. If you believe it is, then you must believe other medical stocks are also highly overvalued and a bearish fundamental story is going to be an easier sell on them than on EYES.

Addressing the addressable market

One criticism of EYES is that it has not explicitly stated what it believes to be its addressable market. In its IPO documents, the company mentions those who are legally blind from retinitis pigmentosa [RP], age-related macular degeneration [AMD] and any other cause for blindness but recognizes that its addressable market is a subset of those individuals. Perhaps there is no set definition of the addressable market because the absolute baseline of the Argus II System is a moving and undefined target, particularly as the technology improves with time. Someone with 20/16000 vision may not feel comfortable with this new technology, while someone with 20/1600 might want to give it a try.

The definition of legal blindness is best-corrected visual acuity of 20/200 or worse or a visual field of view of 20 degrees or less. Out of those people, 15% have no light perception whatsoever. That would be the absolute baseline for EYES. The amount of people with very low vision but some light perception who would unquestionably benefit from this technology is likely going to be greater than that. Second Sight estimates the number of people who are considered legally blind from RP, AMD and other causes, which is summarized in the following table.

I have outlined the company's estimates on the legally blind per each cause for the United States, Europe and worldwide. The company wasn't clear on what worldwide meant, but I took it to mean everywhere excluding the U.S. and E.U. as that would make the most sense when looking at cases relative to worldwide population figures. The addressable market is my estimate of the subset of legally blind people that the Argus and eventually Orion products can help - 33% of people in the United States and Europe and 10% of everywhere else, leading to a total addressable market of just under 60,000 people. I believe the addressable market is substantially lower for regions outside of the U.S. and E.U., because while regions like the Middle East, Canada, Japan, Australia and the BRIC countries will likely approve the device and achieve comparable market acceptance, people with RP in developing nations won't easily be reached with this expensive and specialized device. For AMD and the other categories I used a 25% addressable rate for the U.S and E.U. and 8% for worldwide. While I did not stray from the company's impacted population estimates, it appears that it is understating worldwide AMD figures. I believe there are worldwide individuals in the other category with undiagnosed cases of AMD.

The final line, percentage of success, is my estimate of the company's likelihood in gaining approval for sale in these three markets. For RP, I give a 100% chance of success as it already received the CE mark in Europe and got FDA approval. Chances are that it will obtain regulatory permission from any further markets it applies to for RP. For AMD I give it a 30% success rate. A previous incarnation of the technology in Argus II obtaining approval leads me to believe that Orion I will have a decent one in three shot of obtaining approval as well. I have given a 15% chance of success for any further application for this technology which I believe is reasonable given the early-stage success of Argus and Orion.

The competition

The BrainPort V100 is a device currently on the market which allows blind people to "see" with their tongue as the brain can learn to interpret stimulation signals on the tongue as visual patterns. While it's a non-surgical device, it doesn't appear to be very user-friendly as shown in the picture.

While it certainly provides great utility for when it can be used, I can't imagine that anyone would be willing or able to hold this device in their mouth for any significant length of time during the day. Technology like this serves as a great placeholder for when better solutions like the one provided by EYES come along, but it can't be considered a real competitor to options going forward except for people who absolutely refuse surgery or otherwise cannot rely on EYES or other companies to help restore some vision.

The Alpha IMS by Retina Implant AG also received a CE mark and is currently selling in Europe. Pixium Vision (PIX.PA) has developed technology similar to Argus II with IRIS and plans to submit for a CE mark in Europe in 2015. Neither company has gotten approval in the U.S. Pixium hopes to get FDA approval in late 2017 or early 2018. Other solutions either in device form or through cell therapy are pre-clinical and appear to be years away from a marketable product, if successful.

Argus II has achieved nominal visual acuity of 20/1260 with magnification techniques achieving 20/200 for which the patient could read from a notebook from a foot away. Alpha IMS has achieved 20/546 top visual acuity, so Argus II remains slightly ahead in terms of best vision achieved from its implant. The multi-year advantage Second Sight has will lead to favorable market share assumptions and pricing that I have baked into my model.

Q4 results show substantial improvement

A criticism immediately after Second Sight's IPO was that the company had vastly negative gross margin so the burn rate was very high relative to revenue. 2014 results, and in particular, its Q4 results have put those criticisms largely to rest. Below is a chart of key financial and performance data for year-to-date Q3 and Q4 results for 2013 and 2014.

Q4 2014 was the company's best quarter ever as it implanted and sold 15 devices, more than any other quarter and more than the first 9 months of 2014. What was particularly encouraging is that merely 15 implants already led to significant economies of scale as the company attained positive gross margin for the first time. The cost of sales per implant dropped by more than a third compared to the rest of 2014, while the company managed to stabilize the price per unit at above $100,000 all throughout 2014. I believe that this is a precursor to the company achieving profitability as early as 2017. EYES will still show a heavy burn rate in 2015 and 2016 but that will be through operating expenses as the company will need to hire and train qualified people in marketing, production and operations as it grows.

DCF Model Part 1: Argus II on RP

I will now present my forecast and DCF model for EYES' Argus II System for RP. I provide quarterly estimates for 2015 and annual estimates to 2020. The business model is pretty easy to understand so it's not a particularly complex model. Revenue and cost of sales per implant are multiplied by implants per period to calculate the gross margin. Operating cost run rates are increased with time. The company made mention of potential revenue opportunities from upgrades but has not provided any details on how that model will work. I have excluded upgrades from my forecast so they can be thought of as untapped upside.

Based on the impressive growth in implants and positive gross margin achieved, I expect small but steady growth and margin improvement throughout 2015. For Q1, I expect a total of 17 implants which continues to increase 2 per quarter for the rest of the year. The price per device remains at an average of $110,000 but cost per device declines steadily to $77,164 by Q4. By 2017 I expect the company to be cash flow positive based on a gross margin that improves to 53% with 600 implants done throughout the year. Planned capacity expansion and an increase in the number of implant centers should make this possible as this figure still represents only a very small portion of the addressable market.

By 2020 I expect the company to attain $164 million in operating profit based on 2,700 implants for RP during the year. Gross margin is 75% and opex as a percent of revenue is 14.3% for an operating margin of 60.7%, a reasonable margin percentage for a disruptive technology that has a several-year head start on its competition. The company won't start paying taxes until 2020 as it will have built up a significant net operating loss balance which should last to the end of 2019. I assume the tax rate against its worldwide net income will average out to 30%.

The revenue per implant declines around 2% a year, but the company still maintains a $100,000 price tag as it would have set up the framework for reimbursement by payers. The competition will start entering the market by then, but on heavy losses from upfront capital investment. I doubt that it would be too interested in creating a price war any time soon. EYES will only have a maximum of 3 or 4 realistic competitors before this decade is out and will have a first-to-market advantage on each of them. The cumulative implants that the company will have done by 2020 is 6,934 which is only 12% of the addressable market. I feel that this is a very achievable forecast for the company over the next 5 to 6 years.

With a model built out to 2020, I now provide some assumptions on terminal value and a valuation of the company based solely on RP.

Using a 15% discount rate, the NPV of the cash flow generated from 2015 to 2020 is $101.5 million. Assuming a 25% growth rate from 2020, 2021 net profit is $143.4 million. To calculate terminal value, the 2021 net profit figure is divided by the discount rate less the growth rate (10%). Using the 15% discount rate to calculate the NPV of the terminal value to 2015 will lead to $619.8 million for a total value of $721.3 million.

EYES currently has 35.3 million shares outstanding. I expect 5 to 10 million shares to be issued between IPO shareholder rights, stock options and warrants during that time, as well as another 10 to 15 million share issuance to support working capital until the company achieves profitability. Therefore, I expect 55 million to be a reasonable estimate of the fully diluted float. Dividing $721.3 million by 55 million shares leads to $13.12 per share value. The value of the RP business alone justifies the current stock price.

DCF Model Part 2: Future Argus and Orion products on AMD and other causes of blindness

Assuming success of the Orion I in providing a sight solution for people living with AMD, my forecast for the business from 2019 to 2024 is provided below.

By 2024 the company is performing 18,000 implants in-year and has performed a cumulative total of 33,050 implants for AMD. The revenue per implant starts to fall faster as other companies mature and price competition increases. The losses for the first two years in AMD help to offset the tax burden of the RP business which will be profitable by this time. Forecasting so far in the future becomes difficult but discounting cash flows at 15% a year help to alleviate that risk of inaccuracy.

Using the same discount and growth rate assumptions as for RP and a 25% growth rate from 2024 to 2025, the 2015 NPV of 2019 to 2024 operations and terminal value leads to a total value of $2,353 million. I estimated the chance of success in AMD to be 30%, so multiplying the total value by this 30% estimate and dividing that by 55 million shares leads to a $12.84 per share value for the potential in AMD.

The tremendous potential of the AMD market leads to a valuation that's nearly as high as the RP business even when risk-adjusted for the chance of success and revenues are further into the future with much heavier discounting.

My third estimate is for the "other" business which captures all other possible uses for Argus or Orion outside of RP and AMD. I assume uses outside of those two causes for blindness start in 2021, with the model running to 2026.

27,000 implants are done in 2026 with 49,575 cumulative over those 6 years. The price continues to decline while margins are similar to previous forecasts.

The total value of the business is $2,363 million when cash flows are discounted back to 2015 at 15% annually. Multiplying this figure by a 15% chance of success leads to a $6.44 per share value.

Long-term market share and capital spending needs

The above forecasts are a lot of information to take in at once and it's hard to judge how realistic they are by looking at them separately. Below is a summary of my forecasted annual volume assumptions for EYES per each model, multiplied by the chance of success. For RP volume is taken as is in the above forecast. For AMD it is 30% of volume forecasted above and 15% of volume for the other category.

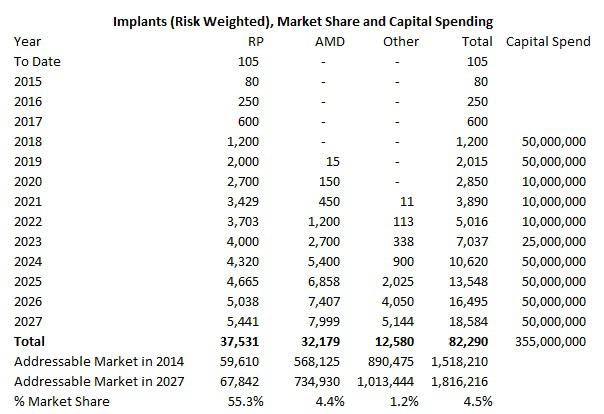

Using RP as an example, notice that volume growth from 2020 to 2021 increases 27% from 2,700 to 3,429. This is in line with the 25% growth assumed in 2021 for the terminal value calculation offset by the price declination per each implant. Every year thereafter assumes an 8% increase in implants to support the 5% in growth in perpetuity. The other two models have the same structure for growth after the time period of each forecast enters into the terminal value stage.

Adjusting for the chance of success, the total implants achieved by EYES in all forms of blindness would be 82,290 by the end of 2027. For the RP market, 37,531 implants would have been performed by the end of 2027. I assume the addressable market grows 1% per year, following world population growth, to 67,842 by the end of 2017. That means that EYES would capture 55% of its addressable market for RP. I believe that is reasonable as a first-to-market technology, especially as it is just a small subset of the total RP market and as the technology improves, the addressable market can grow to include a higher percentage of those who are legally blind from the disease. The 37,531 implants will represent less than 10% of the worldwide population of individuals legally blind from RP by that time.

I have used the same process to calculate market share for AMD and other forms of blindness except that I have assumed the AMD addressable market grows at 2% per year as the population ages and more cases of AMD occur. EYES would have to capture only 4.4% of the AMD addressable market and 1.2% of the other market to support my forecasts when adjusted for chance of success. When assuming a 100% success rate in entering these markets, EYES would only have to capture 15% of the AMD market and 8% of any other form of blindness. There would be 229,000 cumulative implants by 2027 and the one-year price target on EYES would be $96.

The biggest challenge the company will face won't come from sales as I believe the technology will sell itself. But it will be from being able to scale itself to produce and implant thousands of devices each year from the 15 we saw last quarter. From the production side, the company states in its IPO that it can produce up to 100 devices per month based on current capacity. The number will start to face challenges as early as 2018 in my model, so I have built in a large capital expenditure assumption of $50 million each in 2018 and 2019. The company's accumulated deficit by the end of 2014 was $153 million (most of that appears to be in salaries and cost of sales) and there are minimal long-term assets listed on the balance sheet as the company rents its facilities. The costs incurred to increase expansion beyond 1,200 units a year aren't likely to be outstandingly expensive so I believe $100 million combined in 2018 and 2019 is sufficient and will also provide a buffer for other costs such as training or possible understatement of operating costs in my model. The capital spend amount I have assumed in all years to 2027 is $355 million which is $129 million in present value terms or $2.35 per share.

I believe the market share assumptions I have laid out are achievable for EYES and support the valuation conclusions I have laid out below.

Conclusion: EYES fair value of $30 per share

My one-year price target for EYES based on potential future cash flows of the RP and AMD markets as well as any other forms of blindness is $30 per share, broken down as follows:

EYES represents a tremendous opportunity for risk-tolerant investors who like to invest in the healthcare sector. EYES is a first-to-market entrant with outstanding technology that gives people suffering from a complete or near-complete inability to detect light due to retinitis pigmentosa a chance to see again. The technology will only improve to impact more people's lives in an extremely positive way. Second Sight and only a handful of other companies a few years behind it will be able to impact our society and tap into a significant portion of that $717 billion market for eye problems to be faced by Americans by 2050. That number is going to be in the trillions worldwide. A $30 target on 55 million shares leads to a $1.65 billion market cap but this technology is worth billions. I believe those investors who are patient enough to hold this stock for a decade or longer will be seeing prices that are multiples beyond $30 if EYES comes anywhere close to the success I have forecasted and there is still plenty of opportunity for the company to surpass my estimates.