Thesis: Having seen their business suffer from oversupply of ships combined with weakness in the global economy, dry bulk shipping stocks have hit multi-year lows. Business appears to have bottomed. Newbuilds will slow and scrapping has accelerated. The stocks appear set to rebound. Scorpio Bulkers, Inc. (SALT) has positioned itself to be the best performing stock in the group.

Dry Bulk Shippers Have Been Taking on Water for Years

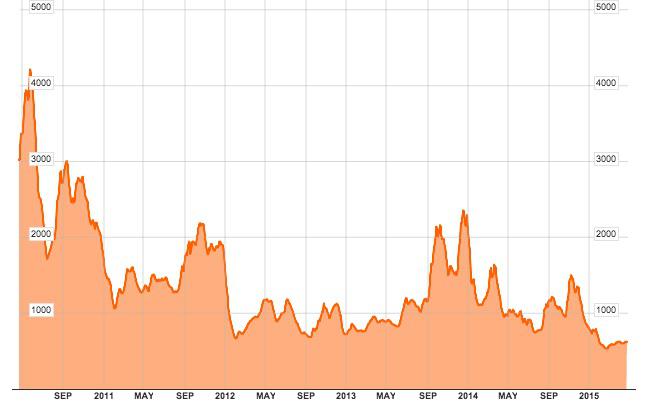

The market for bulk shipping has been declining since 2010. This is historically a cyclical industry, but this downturn has been especially harsh. Look at the chart below, which shows the Baltic Dry Bulk Index (from Bloomberg). From its peak of over 4,000 in late 2010, the index has suffered an almost 90% decline to a recent low of around 500.

This is the lowest the index has ever been, exceeding the previous low, set in 1986, by roughly 8%. This weakness is, of course, reflected in the charter rates. According to Navios Maritime, the current 1-year charter rate is $7,525. On an inflation-adjusted basis, this is the second lowest it has ever been and is within 4% of the all-time low, which was set in January of 1999.

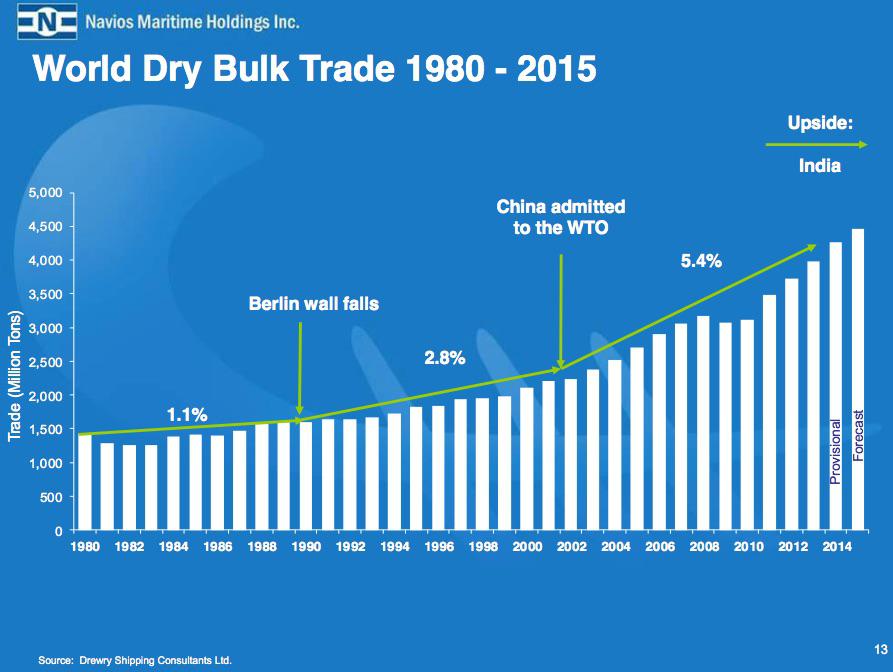

It's rather surprising, but this weakness in the dry bulk index is not a result of weakness in global trade. Yes, trade is very tied to economic growth and is cyclical in nature. But, there have been dramatic global forces, mainly the economic emergence of China, that have really caused an increase in trade right through economic cycles. As the chart below plainly shows, dry bulk has been a growth industry for quite a while.

Dry bulk has grown at over 5% per annum since 2002. This is tremendous growth, yet the Baltic Dry Index is in the toilet. Why is this happening? Well, it's due to the cyclicality of the industry... a cyclicality that is the result of the shippers themselves.

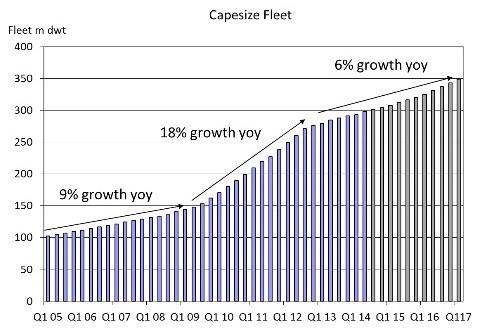

Shippers in general, and dry bulk is no exception, are their own worst enemies. They tend to build ships during good times and scrap them during bad. To the point where the good times become not so good due to their own actions. For an industry that has grown over 5% for the last decade, to have the index be hitting an all-time low would have necessitated a lot of building. And, this has been the case.

The above graph from SwissMarine Services SA shows the growth in Cape Size ships. Enough growth to dramatically overcome the strong growth in volumes in the dry bulk industry. It is a direct result of this growth in dry bulk shipping capacity that has caused prices to erode, balance sheets to weaken, and has left the industry in a precarious position should volumes weaken; a weakening that has happened over the last year with China slowing imports of commodities such as coal and iron ore.

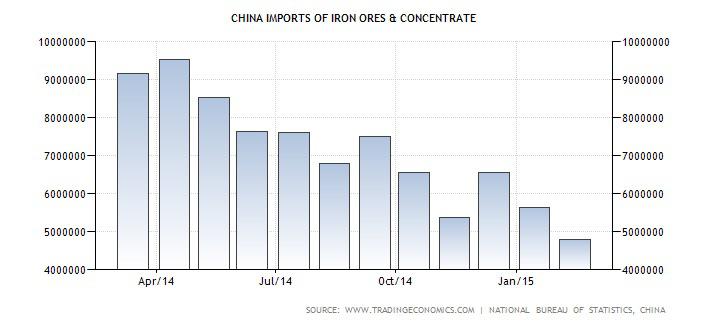

As the above graph shows, the world's growth driver for dry bulk is slowing down dramatically. It's this slowdown, coupled with overbuilding of new vessels, that has put the Baltic Dry Bulk index its lowest level ever.

As one might expect from looking at the index and the charter prices, there has been a dramatic selloff in the share prices of dry bulk shippers. Most of these companies have seen their share prices collapse in excess of 75% from their all-time highs. The last year has been particularly rough as low prices have put many of these companies in economic peril. Below is the chart of Diana Shipping (DSX). Considered one of the higher quality names in the industry, DSX's chart reflects the current woeful state in dry bulk.

This is an ugly chart and it's from one of the best companies in the group. Most of the other dry bulk shipping companies have suffered similar or worse fates with several players going insolvent or needing to raise money at very depressed levels. The industry has had a disastrous few years and is, like the Baltic Index, at historical low valuations.

Valuations May Have Hit Bottom

As with any cyclical industry, investors who have the ability to look fear in the face are the ones who get in at the cheap valuations. When the fundamentals appear worst, is when you want to be buying cyclical stocks. And, for dry bulk shippers the current fundamentals, with the Baltic at an all-time low, are the worst they've ever been.

However, with weak fundamentals comes low valuations. This is where the industry starts to get interesting. In dry bulk shipping, you have an industry that is growing, albeit slowing down, so demand for the ships exists. And, there is a lot of value in the ships for the steel that goes into making them.

Having a strong core trend to volumes, with buyers of scrap ships, creates an active marketplace for used ships. Thus, there is a pretty ability to put a fairly accurate NAV on the fleets of dry bulk vessels controlled by the operators.

And, this is where the industry starts to get attractive. Looking at these stocks as a percentage of NAV, investors can get comfort that there is real value to the names.

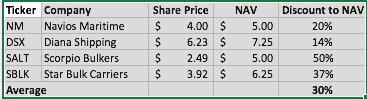

As the above spreadsheet shows, these four dry bulk shippers are trading a discount to NAV of 30% on average. I chose to represent these four as they are all buy rated by Stifel Nicolaus. The rest of the group trades with large discounts, as well.

It is this author's belief that, with discounts to NAV averaging 30%, we are at a bottom in the group. The question is, what, if anything, will get us off the bottom?

Potential Catalysts in Dry Bulk

The good news for dry bulk is that there are several potential catalysts for the industry. With valuations so low, and charter rates stuck right around opex, any of these catalysts could spark a meaningful change in rates for the industry and cause a large relief rally in the share of dry bulk shippers.

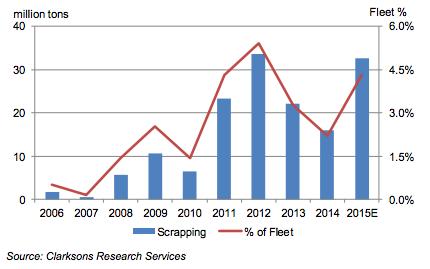

The first catalyst is happening now. Much like the overbuilding when times are good, ship owners are now cutting back on newbuilds and increasing scrapping rates. According to Clarksons, newbuild orders for dry bulk went from 201 vessels in 2013 to 342 in 2014. Where have they projected 2015 newbuilds to come out? At a grand total of 23 vessels. Clearly ship operators are finally reacting to the oversupply in the industry. This is also reflected in the numerous articles published recently about bankruptcies for ship builders. We are seeing a definitive collapse in newbuilds.

Simultaneous with a decreased order book for newbuilds, scrapping rates are remaining at high levels. Clarksons estimates 4.5% of the fleet to be scrapped in 2015. Between slowing building and increased scrapping, the first potential catalyst for prices is happening. Now it's just a matter of having demand pick up to see this impact flow through to charter rates.

The rest of the potential catalysts all surround increased levels of shipping activity. If any of these happen, prices should reflect the tightening of the supply/demand equation and could be the catalyst to spark growth. I'll list the catalysts below.

1. Increased iron ore shipments to China. With the price of iron ore at multi-year lows, it is now cheaper to export iron ore from Australia or Brazil to China than it is for local Chinese producers to sell into their own market. Brazil in particular is a very long haul route. Volumes here have been weak of late. However, any significant pickup in the amount of iron ore shipped to China could be a major catalyst. Worth noting: steel prices have picked up recently.

2. Increased coal shipments to Asia. Chinese demand for coal has been a major driver of this commodity's volumes. Of late, it has dropped off quite rapidly. However, the dropoff is much larger than any decrease in domestic Chinese consumption of coal. Quite possibly, Chinese demand for coal has bottomed and will pick up over the course of 2015. Meanwhile, India's appetite is increasing. There's a good chance coal shipments increase throughout this year.

3. Grain shipments increase. This has been a great summer (in the Southern Hemisphere) for grain crops. Expect volumes of this commodity to be stronger than usual in 2015.

Business is weak now for the dry bulk shippers. But, they are taking the necessary steps to right-size their fleets. And, several potential demand catalysts exist. This combination of lessened supply and, possibly, increased demand positions the industry for a nice rebound from historically low valuations.

Scorpio Bulkers is my top pick

Based on the above arguments about historic low valuations, combined with potential increases in charter rates, I have been looking to get involved in the group. The stock I have bought is Scorpio Bulkers .

There are two things I like about SALT. The first is its large discount to NAV. As the aforementioned spreadsheet showed, SALT had the largest discount of its peers, at 50%. I expect this to close. So, even if I'm wrong on the catalysts, SALT has a chance to perform well regardless.

The second thing I like about SALT is also the reason why I think their discount to NAV spread will narrow. SALT has been penalized in the market for a very large new order book. SALT was overly aggressive during the last few years in terms of booking new vessels. And, the market has been (justifiably) worried about SALT's ability to pay for these ships.

However, on April 21, SALT announced the sale of a number of their newbuild vessels, pre-delivery. While SALT took a loss on this sale, it was a manageable loss and one that greatly reduced their financing risk. SALT now has a manageable, and fundable, order book.

I expect the street to revalue SALT on a smaller discount to NAV as a result of their financial derisking. If any of my potential catalysts come to fruition, and, in a cyclical business, something always does turn around, there is potential for a meaningful uptick in rates. As a result, I'm long SALT with a near-term target of $3.25 just based on a smaller discount to NAV. And, if rates pick up, there might be substantially more upside over the course of 2015.