Automotive components supplier Magna International (NYSE:MGA) has gained impressive momentum in the past three months, with its shares appreciating more than 7%. This is despite the fact that Magna's Q1 results were not that great, as the company saw an year-over-year drop in revenue on account of weakness in certain segments. However, Magna had outpaced analysts' expectations in the quarter. But, will Magna be able to sustain its recent momentum going forward? We'll try and answer this question by focusing on those specific areas where Magna is facing challenges

Vehicle assembly will get better

Last quarter, Magna's vehicle assembly sales fell 28% year-over-year to $584 million on account of a 23% drop in assembly volumes to 27,000 units. The drop in volumes was attributed to weakness in the production of BMW's Mini Countryman. However, BMW is restructuring the Mini brand by cutting three models from the line-up. According to a Bloomberg report late last month, BMW will "cease production of its coupe, roadster and Paceman crossover, reversing course on a strategy of adding variants that failed to spark growth."

BMW will now be focusing on the remaining five models in the Mini line-up, including the Countryman. The Countryman is an important model for the Mini brand since it accounts for 80% of overall sales. As such, BMW is doing the right thing by right-sizing the Mini portfolio and focusing on more successful cars such as the Countryman. This will act as a tailwind for Magna as it could see an increase in the Countryman's assembly as BMW ceases the production of slow-selling models.

On the other hand, Magna's vehicle assembly business was helped by an increase in the production of the Mercedes-Benz G Class SUVs. Looking ahead, it is likely that Magna will receive more orders for the G Class as this line of vehicles is selling at a fast pace. As reported by Just Auto:

"In the SUV segment, Mercedes-Benz not only celebrated the world premiere of the new GLC last month, but also a new sales record (+17.3%). During the first half of the year, sales of the GLA, the GLK, the M-Class, the GL and the G-Class increased by 25% to 232,406 units. The G-Class - the prime father of all Mercedes-Benz SUVs - set a new sales record in the first six months of the year (+27.6%)."

As a result, the production of the G-class Mercedes-Benz SUVs should increase going forward as the company will be ramping up production in order to meet increasing demand. Moreover, Magna should also benefit from the secular growth expected in the SUV segment going forward. For instance, Lucintel is of the opinion that the SUV manufacturing industry will increase at a CAGR of 5.7% until 2017, so Magna's vehicle assembly business should get better going forward.

The European car market should pick up pace

During the first quarter of 2015, Magna struggled in the European market as it witnessed a marginal decline in vehicle production in the continent. As a result, the company's European production sales dropped 17% to $2.18 billion. This is not surprising, as automotive growth in Europe is anticipated to be slower this year than 2014.

Earlier this year, the European Automobile Manufacturers Association said that new car registration in Europe will increase 2% this year to 13 million. In comparison, new registration growth was more robust at 5.7% last year. However, the good thing is that the European car market seems to be gaining pace.

For instance, at the end of April, French car maker PSA Peugeot Citroen raised the European auto market's growth forecast from 1% to 4%, which is why it is ramping up production in the continent to meet increasing demand. Additionally, Peugeot is a Magna customer, so a ramp up in production will have a positive impact on its sales.

Thus, it is likely that Magna will witness growth in European vehicle production going forward, and this will act as a tailwind for the company.

Challenges to consider

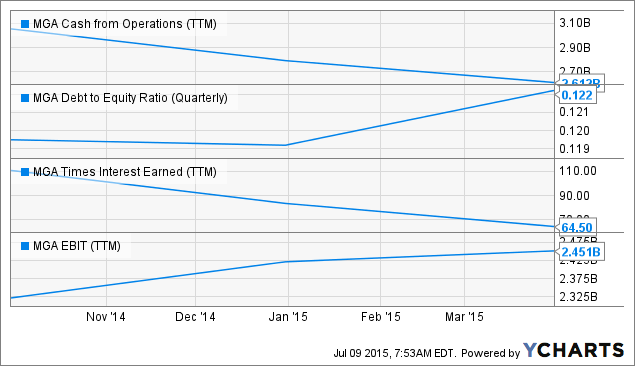

Investors, however, need to keep an eye on Magna's deteriorating fundamental position. The company's current cash position is better than its debt, while its cash flow position is also robust. But, a closer look at its fundamental position in the past year indicates that Magna is seeing weakness in its fundamentals. This can be gauged from the following chart:

MGA Cash from Operations (NYSE:TTM) data by YCharts

From the above chart, it is clear that Magna's cash from operations has been declining steadily over the past year. Additionally, the company has seen a rise in its debt-equity ratio, which means that its interest burden has increased. As a result, despite an improvement in EBIT, Magna's interest coverage ratio has declined, which means that the company's interest burden has increased at a greater pace than the EBIT.

This could keep the company's bottom line performance under pressure, and lead to further weakness in the cash flow. Thus, this is one threat that could derail Magna's recent momentum going forward.

Valuation and takeaway

From the above discussion, it is evident that demand for Magna's components will increase on the back of a pick-up in demand in Europe, while its assembly business will be positively impacted by growth in Mercedes' SUV sales. This probable recovery, along with a favorable valuation, indicates that Magna is a good investment.

The stock has a trailing P/E ratio of 12.4, while the forward P/E stands at 10. This indicates that its earnings are expected to increase in the future, a possibility that's further reinforced by a PEG ratio of 0.97. A PEG ratio of less than 1 is considered desirable as it indicates strong earnings growth. Thus, considering Magna's valuation and improving prospects in the auto industry, it should be able to sustain its recent momentum going forward.