In today's market with most biotech companies sporting bloated valuations it can be hard for investors to find stocks with significant upside. I have written some recent articles on a couple of my favorite small cap biotech companies that are significantly undervalued and are primed to pop on upcoming catalysts. These include the newly uplisted immuno-oncology company OncoSec (OTC:ONCS) which has an enterprise value of only ~$60M despite impressive clinical results and a Phase2b clinical trial combining their technology with Merck's PD-1 inhibitor in advanced melanoma which just started. I'm also a big fan of Tokai Pharmaceuticals (TKAI) which has surged ~25% since I detailed their personalized medicine prostate cancer drug Galeterone a little over a month ago. However, in my opinion the king of all undervalued biotech companies right now is Cytokinetics (NASDAQ:CYTK), the industry leaders in developing drugs that modulate muscle function. I cannot find a biotech on the market as cheap as Cytokinetics which has the advanced pipeline, partnerships and hoard of cash that they possess. The current market cap of the company is ridiculously low at ~$260M, with over $100M of that in cash. Their lead drug, Tirasemtiv, just entered Phase 3 last week and is easily the most advanced drug for amyotrophic lateral sclerosis (ALS) in development. I'll explain below why this trial is highly de-risked and provides a good long term investment opportunity. In addition, Phase 2 data for the Amgen (AMGN) partnered drug Omecamtiv Mecarbil (OM) is expected in the second half of this year and will significantly boost the stock. If these two drugs weren't enough to illustrate how absurd the current market cap is, Cytokinetics third muscle activating compound CK-2127107 has been partnered and funded by Astellas and will enter a Phase 2 study for spinal muscular atrophy (SMA) this year. Over a decade of research is coming to fruition for Cytokinetics and it's time for investors to take notice. Cytokinetics offers one of the best risk/reward profiles on the market and in agreement with Roth Capital who just slapped an $18 price target on the stock, I think investors who get in now will have no problem doubling their money by years end.

Tirasemtiv Will be First Approved Drug for ALS in Over 20 years

When investors look at the potential for a drug to get approved they need to analyze not only the clinical trial data but also take into account the disease being targeted. For example, when Geron's Myelofibrosis (MF) drug Imetelstat was placed on clinical hold due to low level liver toxicity the stock tanked. However, since Imetelstat is the only drug to ever produce a complete response in advanced MF I encouraged investors to load up on the stock as the FDA would soon release the hold based on the risk/reward profile. Those that listened are up over a 100%. Tirasemtiv treatment for ALS is a similar scenario. ALS is a rapidly progressing neurodegenerative disease which is generally fatal in 3-5 years following diagnosis. There is no cure. The only ALS drug approved by the FDA is Sanofi's Riluzole which only delays disease progression in a small subset of patients by ~ 3 months. This drug was approved in 1995, so it has been over 20 years with nothing new. The ALS community and the FDA are primed to approve a drug for this disease state. Enter Tirasemetiv.

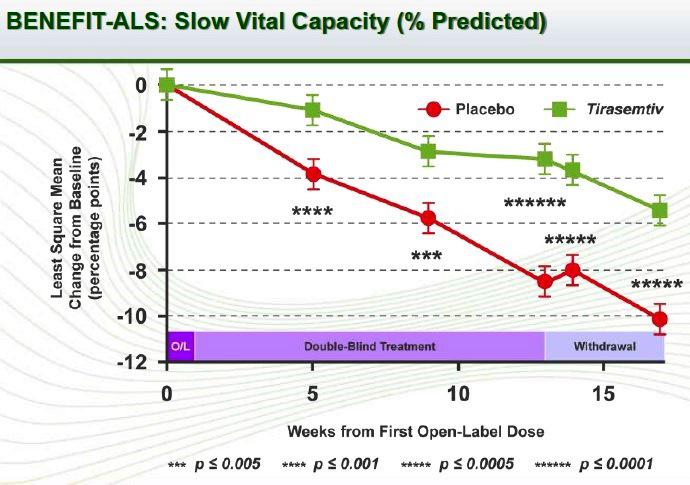

Tirasemtiv, a fast skeletal muscle troponin activator, is extremely well characterized having had 11 clinical trials, with 5 of them being specific for ALS where over 850 ALS patients participated. The drug has been granted orphan drug status and fast track status by the FDA. In one of the biggest ALS clinical trials ever conducted consisting of over 700 patients from 75 different centers, the double-blind placebo-controlled Phase 2b BENEFIT trial failed to meet the primary endpoint of improvement in the Functional Rating Scale-Revised (ALSFR-R), which measures everything from speech to walking ability. The stock crashed on the news. However, upon analyzing all the data, it was revealed that there was a highly statistically significant improvement in secondary endpoints measuring the decline of slow vital capacity (SVC), the measure of strength of the skeletal muscles during breathing and the muscle strength Mega-Score, the measure of strength from several muscle groups. Importantly, respiratory failure is the most common cause of death in ALS patients and improving SVC could increase survival or at the very least, significantly improve the quality of life of patients by making it easier to breathe. The data was impressive, with a significant reduction in SVC decline at every time point measured, which was even more pronounced as time went on.

*Slide from Cytokinetics 2015 Corporate Presentation

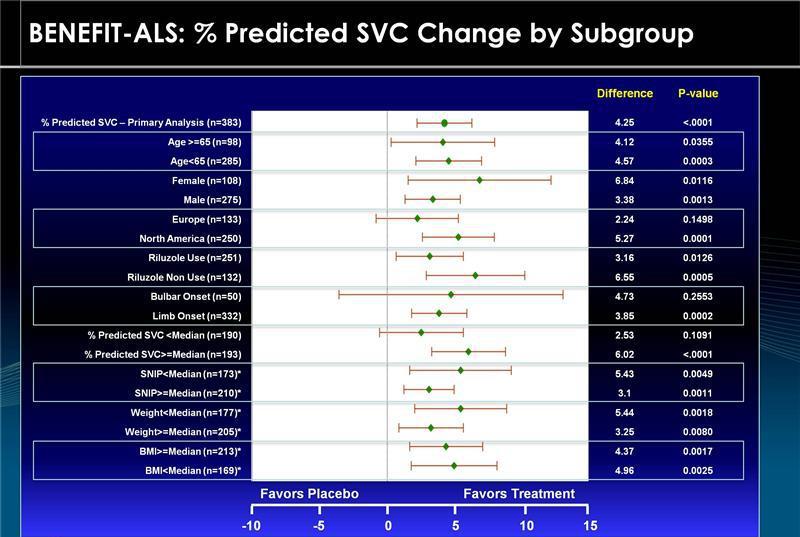

In addition, the impact on SVC was seen in all subgroups.

*Slide from 27th Annual ROTH Conference in March 2015

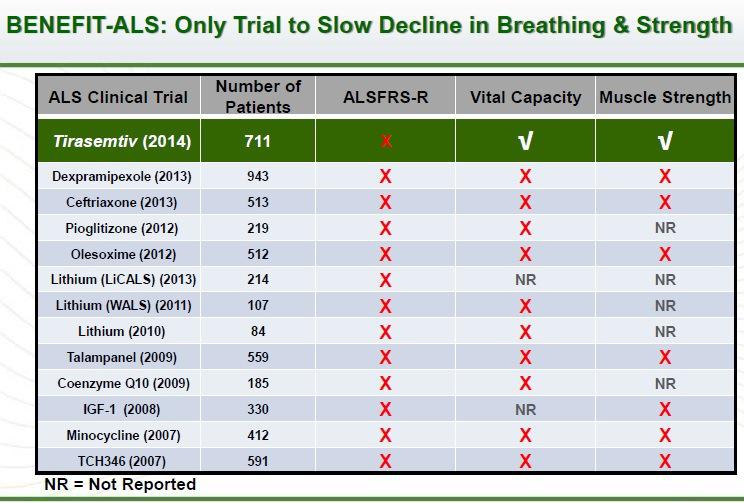

BENEFIT-ALS was the first clinical trial to ever demonstrate a positive effect on respiratory or skeletal muscle function. The first clinical trial in over 20 years of any relevant enrollment size to have any positive outcome.

*Slide from Cytokinetics 2015 Corporate Presentation

I detailed in numerous articles that Tirasemtiv would progress into Phase 3 clinical trials and that the FDA would be amendable to SVC as a primary endpoint. Investors that bought on my recommendation are up over 100%. As expected, last week Cytokinetics announced the start of the Phase 3 VITALITY-ALS which is designed to enroll 445 patients at more than 75 centers in North America and Europe with a primary endpoint of change from baseline in SVC after 24 weeks. Also included will be several secondary endpoints such as measuring SVC at 48 weeks, measuring respiratory factors in ALSFRS-R scale, time to assisted ventilation or death, change in Mega-Score, etc.

In my opinion this trial has a very high chance of success. First, the Phase 2 trial was one of the largest ALS trials ever conducted and in 75 different centers. Due to the enormous size of the Phase 2 BENEFIT-ALS trial and the resounding statistical significance in SVC decline (<.0005), there is a high probability the data will be reproduced at 24 weeks in Phase 3. Most of the same ALS centers which participated in Phase 2 are included in Phase 3 so they are already knowledgeable about the drug and how to manage the side-effects. Again, this is ALS, any significant sign of clinical efficacy will result in FDA approval. Critics of the Phase 3 trial are quick to point out that Cytokinetics did not receive a special protocol assessment (SPA), which is a sign-off by the FDA that they agree on all the endpoints and trial design for approval. Cytokinetics management has designed the trial after numerous meetings with the FDA and ALS thought leaders and have stated numerous times they would not have progressed to Phase 3 if the FDA was not amendable to a SVC primary endpoint. In today's regulatory environment many drug companies do not apply for a SPA review by the FDA. In 2014, in an article published in the Journal of the American Medical Association, researchers found that 20% of approved drugs came without any meetings between the drug makers and the FDA before beginning Phase 3. In addition, more than 25% of drug makers that got SPA did not follow the FDA recommendations, making their SPA void, and still went on to get their drugs approved. Importantly, an FDA spokesperson commented on the report stating:

This system has worked well for over 50 years, and as the authors note, in many cases sponsors are successful in gaining approval for their new drug even if they did not accept and follow FDA's advice...

Cytokinetics has met with the FDA numerous times to discuss the design of the Phase 3 clinical trial and per my communication with Cytokinetics they are actively engaged with regulatory authorities concerning the trial. Make no mistake, SPA or not, Tirasemtiv will be approved if the primary endpoint of the trial or even secondary endpoints are met. Cytokinetics certainly has the support of the ALS Association having been granted $1.5 million towards the Phase 3 Tirasemtiv trial last week. With over 22,000 ALS patients estimated in the US and another ~14,000 in Europe the potential for Tirasemtiv to be a billion dollar blockbuster drug is real. Cytokinetics has retained the full rights to Tirasemtiv and has the money to fund the Phase 3 trial to completion. With no effective treatment options available, a minimal sales force will be able to capture the majority of the global market.

Omecamtiv Mecarbil Progression to Phase 3 Will Double Stock

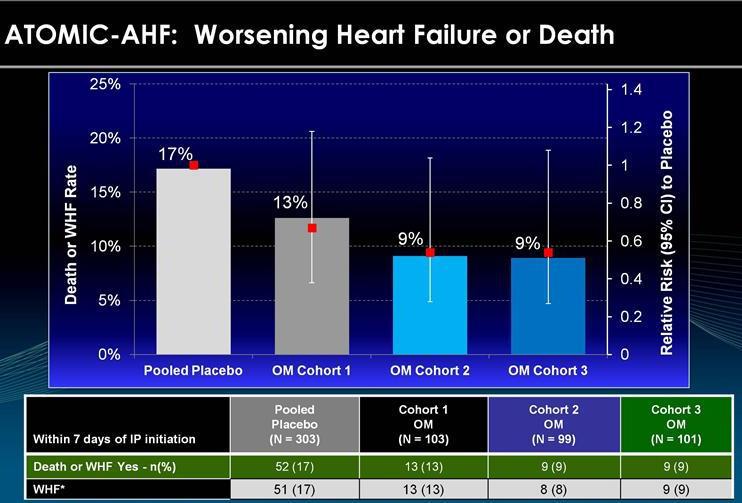

OM, a cardiac specific myosin activator drug being co-developed with Amgen, is currently in clinical trials for treating acute and chronic heart failure. The stock took a beating last year when the 613 patient ATOMIC-HF Phase 2b trial, a study to evaluate the safety and efficacy of IV infusion in acute heart failure, failed to meet the efficacy endpoint of dyspnea relief. However, as I've written about previously, the trial was never powered to meet this endpoint and the data was actually quite impressive with a 45% reduction in the 7-day incidence of worsening heart failure, compared with the 17% rate in controls.

*Slide from 27th Annual ROTH Conference in March 2015

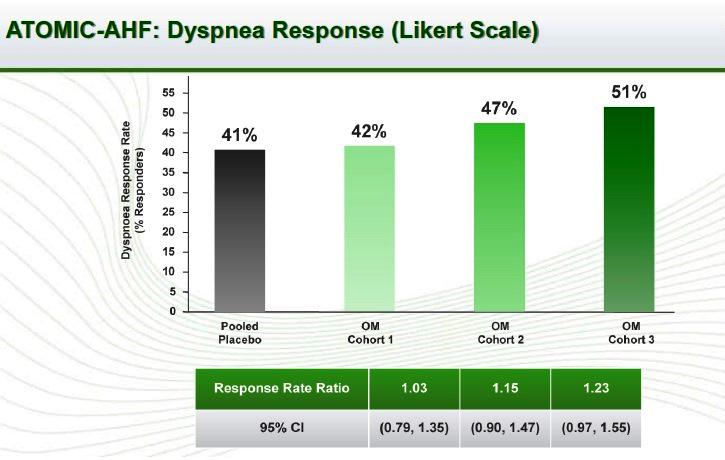

Remember, patients were only dosed for 48 hours, so the ability to see a therapeutic benefit after such a small treatment window is encouraging. Wall Street missed the fact that the trial was designed to pick the correct dose going forward and the data was analyzed with lower doses though to be sub-therapeutic. When looking at the data there is a dose dependent reduction in dyspnea with cohort 3 (therapeutic dose) having the greatest impact.

*Slide from Cytokinetics 2015 Corporate Presentation

In addition, the safety profile was similar to placebo and the Pharmacokinetic (PK) and Pharmacodynamic (PD) profiles were consistent with the drugs mechanism of action. Amgen and the cardiovascular clinician community appeared happy with the data. As a vote of confidence, after seeing the data Amgen paid Cytokinetics $25M to expand the OM license to include Japan.

The COSMIC-HF trial is a double-blind, placebo controlled study enrolling ~530 patients with a primary endpoint of pharmacokinetics and tolerability following 20 weeks of oral formulation exposure. The trial has completed enrollment and is expected to report out in Q4 2015. I believe the trial has a high chance of success as the main objective is to assess the pharmacokinetics and tolerability of OM in patients, which has been consistent in all trials, including ATOMIC, in over 1000 patients. There is no pre-specified clinical efficacy endpoint like in the ATOMIC trial which can be misinterpreted by investors. Following the release of the COSMIC results, Amgen and Cytokinetics will review the totality of the combined data and determine the path forward.

Amgen's launch of their cardiovascular division with the approval of the PCSK9 inhibitor Repatha provides good timing for OM. In accordance, during Amgen's earnings call they mentioned OM and Cytokinetics several times as an important piece of their cardiovascular portfolio. Amgen has paid Cytokinetics ~$150M to date for OM and recently extended the research program with Cytokinetics to discover new cardiac sarcomere activator compounds. All signs point towards OM moving into Phase 3 studies and a continued strong relationship with Amgen. Progression into Phase 3 will trigger a substantial milestone payment and will be a major stock catalyst.

CK-107 Phase 2 for Spinal Muscular Atrophy to Begin This Year

It is very surprising that Cytokinetics sports such a cheap market cap with Tirasemtiv and OM in their pipeline. Throw another drug in the pipeline CK-107 and a partnership with Astellas and the current valuation is ridiculous. This trial will be funded completely by Astellas and will begin this year. This achievement resulted in a $45M milestone payment recently to Cytokinetics. The safety, tolerability and PK/PD have been well characterized in five Phase 1 clinical trials in over 100 patients. To date, the drug has illustrated statistically significant dose related effects on muscle force measures compared to placebo. Recent preclinical data suggests the drug could be used in treating a wide variety of diseases and conditions associated with muscle fatigue. For example, a recent publication illustrates the drug could also be effective in increasing exercise performance in heart failure patients. CK-107 is another exciting compound being developed by Cytokinetics with the backing of a strong partner in Astellas.

Risks and Financial Position

All small cap biotech traders realize the risks involved in investing in these highly volatile stocks. Cytokinetics has several catalysts on the horizon which all have a significant chance of being positive and sending the stock much higher. At the current enterprise value hovering around $150M, I see very little downside in the stock price. The financial position of the company is strong, holding over $110M in cash or cash equivalents. In addition, Amgen and Astellas fund a significant portion of the OM and CK-107 studies respectively and are both over 5% owners of Cytokinetics.

Conclusion

The mature pipeline and partnerships that is coming to fruition is a long time in the making. The value of Tirasemtiv entering Phase 3 would typically be enough to justify the current market cap. In addition, Cytokinetics has OM, which I believe will move into Phase 3 and CK-107 for SMA moving into Phase 2 which are funded in collaboration with Amgen and Astellas respectively. Trading under $300M market cap with a diversified mature pipeline, strong collaborations and a war chest over $100M in cash I would challenge any investor to find a biotech on the market that is a bigger bargain. Expect to double your money as catalysts mature.