Earlier this month, Disney (DIS) set off a firestorm among the media stock when the company announced ESPN experienced modest subscriber losses during the quarter and gave a candid view of where technology is going over the next several years. Disney CEO, Bob Iger, even went as far as to say he can see a day when ESPN could be sold directly to customers in an "over-the-top" platform.

This frank discussion by one of the most powerful media entertainment companies in the world caused a dramatic sell-off across the industry. Investors and analysts feared cord cutting is the wave of the future and the traditional massive cash cow TV packages that Disney, CBS (CBS), Viacom (VIAB), and Comcast (CMCSA) (CMCSK) have enjoyed over the decades could be replaced by over-the-top content.

Akamai Technologies (NASDAQ:AKAM)

Akamai is a global leading CDN with over 175,000 servers in over 100 countries with over 1,300 networks. Akamai's infrastructure is responsible for delivering 15-30% of all web traffic and accounts for over 2 trillion daily Internet interactions. The company serves the top 30 media and entertainment companies, all top 20 global e-commerce sites, 9 out of the top 10 social media sites, iTunes, and all the major US sports leagues. Akamai is perfectly situated to benefit from cord cutters and media content providers adopting OTT service options. The company has been heavily investing in its infrastructure to provide expanded capacity to meet growing demand that it expects in 2016.

While the largest content and media sites, such as Netflix (NFLX), Facebook (FB) and Amazon (AMZN), have built out their own CDNs, this option is far too expensive for many companies. Akamai offers its customers enhanced web performance to handle large fluctuations in traffic, cloud security solutions to protect against the largest distributed denial-of-service and web application attacks without reducing performance, and media delivery solutions for instant access to high definition video content on any screen.

Through the first 6 months of 2015, revenue is up 15%, with particular strength from its emerging cloud security business. The company has increased capital expenses over 50% to $233 million through the first half of the year as the company gears up for what they expect to be a substantial increase in OTT traffic in 2016. In particular, the company expects to benefit from a major increase in streaming video worldwide from the 2016 summer Olympics in Rio de Janeiro, as well as the growing cord-cutting trend.

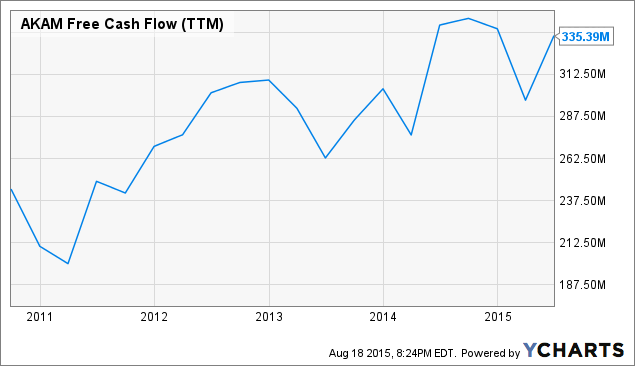

Once Akamai winds down their increased capital expenditures, the company should see a big jump in free cash flow. Through the first 6 months of 2015, cash flow from operations is up 25% to $363 million. The $79 million increase in capex has resulted in flat free cash flow YTD. Once capital expenses stabilize in 2016, free cash flow should increase 25-35% year over year to roughly $425-$450 million.

AKAM Free Cash Flow (TTM) data by YCharts

Akamai has been widely rumored to be gearing up for the eventual launch of the new Apple TV (AAPL) subscription service. While rumors have persisted for years about when Apple would launch its TV subscription service, a new Bloomberg report states the company is now aiming for a 2016 launch. According to the report, negotiations to license programming from TV networks, such as those owned by CBS and 21st Century Fox (FOXA), are progressing slowly. If rumors are true, Apple could eventually revolutionize television the same way it did for the music industry through iTunes. In order to accommodate the potentially massive new internet traffic that such a service would generate, would be a huge catalyst for Akamai. Even if Apple spent the millions and millions of dollars needed to develop a massive CDN, like Netflix did, it would still take time and Akamai would still be an immediate beneficiary.

Takeaway

Whether it's through Google's (GOOG) (GOOGL) Chromecast, Amazon's Fire TV, Hulu, Netflix, HBO Go, the revamped Apple TV, or the widely rumored Apple subscription TV service, content is rapidly migrating to an online streaming platform. To achieve the most reliable performance for high definition on multiple devices without buffering, these services will widely depend on CDNs. With Akamai's extensive CDN, it is perfectly positioned to benefit from this trend. The company has been heavily investing to expand its infrastructure to prepare for the increase in OTT traffic in 2016.

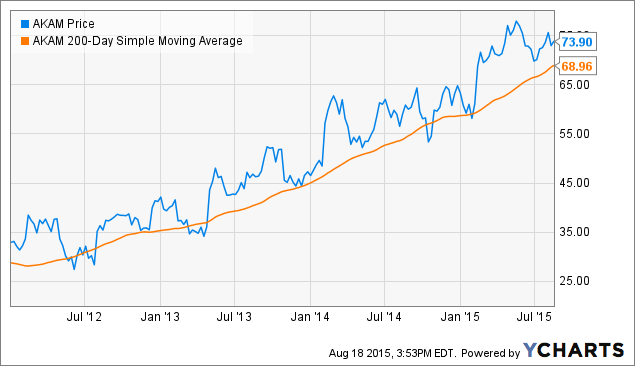

I've put Akamai on my watch list to buy on any significant pullback. When the company provided soft Q3 guidance in late July, the stock fell 10% before regaining all that lost ground the next day. The stock historically tends to only briefly hit its 200-day moving average before sharply bouncing higher.

AKAM data by YCharts

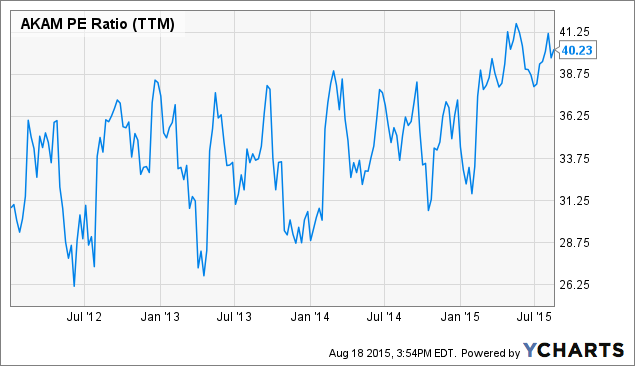

I plan to remain on the sidelines in the immediate future and hope the stock can pull back to more attractive levels. Based on the strong catalysts and the company standing to capitalize on a shift in consumer habits, I think the stock is fairly valued at current levels.

AKAM PE Ratio (TTM) data by YCharts

As you can see from the chart, the stock's P/E value is slightly higher than its historical performance, which unfavorably skews the risk/reward ratio. Based on the charts, I believe, in the short term, the downside potential outweighs the upside. Other than the September Apple event where the company is expected to unveil a revamped Apple TV set-top box, there aren't many catalysts on the horizon. The company is banking on 2016 to be a record breaking year for content delivery, so there's likely time to be patient to wait for a pullback. I'll look to be a buyer when the stock pulls back closer to its 200-day moving average around $68/share.