As Barthes (1987) suggests, "[t]he narratives of the world are numberless." We can't help it; we think in narratives. They're useful, cognitive shortcuts that allow us to organize the world into patterned meaning. In that way, narratives are extraordinarily useful: they simplify the world, making it easier for us to understand.

But as investors, are we storytellers? Is the mission of analysis to craft stories, fitting all stock news into those narratives? Or is our mission to eschew narratives in favor of information, so that we can look at investing objectively? As Tom Gilovich explains in his book Why We Know What Ain't So:

Human nature abhors a lack of predictability and the absence of meaning. As a consequence, we tend to "see" order where there is none, and we spot meaningful patterns where only the vagaries of chance are operating.

Narratives may help us order the world, but they can also cause us to believe in things that aren't there. As Gilovich continues:

While praying for his critically ill son, a man looks at the wood grain on the hospital room door and claims to see the face of Jesus; hundreds now visit the clinic each year and confirm the miraculous likeness. Gamblers claim that they experience hot and cold streaks in random rolls of the dice, and they alter their bets accordingly.

[...] The predisposition to detect patterns and make connections is what leads to discovery and advance. The problem, however, is that the tendency is so strong and so automatic that we sometimes detect coherence even when it does not exist."

In Nassim Nicholas Taleb's The Black Swan he popularized the idea of the narrative fallacy: our tendency to construct stories around facts becomes problematic when we narrate facts to fit into our stories.

Investors can be seduced by narratives and entire stocks can become shrouded in them. One surprisingly helpful indicator for story-stocks whose prices may not be based in reality is something we've dubbed the Rudeness Indicator. Of course, we too may be seeing patterns in the grain where none exist; but we've noticed a strong connection between the number and intensity of rage-filled responses to our articles and subsequent contraindicating stock performance. Our article on Fortinet, Inc. (FTNT) is a recent, strong example of this. When an article interferes with the narrative some investors have built for a stock, instead of rationally responding to the arguments laid out in the article, they respond with vitriol.

Why the anger? Well, nothing angers people more than challenging the truths they tell themselves. It can be a painful experience to find out that our presumptions may be wrong, as Peterson writes:

Your presumptions about the nature of the world are in error. The world you know has just crumbled around you. Nothing is what it seemed; everything is unexpected and new again. [...] How could you have been so mistaken in your judgment?

In NNT's notes he talks about how journalists' need to narrate hinders their ability to report factually. He writes:

Soc Gen sold $70 billion worth of stock on Monday Jan 22, 2008, to liquidate the rogue trader's positions. They did it the French way (clumsily, one single stressed out trader; they did not realize -or did not take into account -that NY was closed for the Martin Luther King holiday). They kept selling at lower and lower prices. The NYT journalists (they were not alone) attributed the move in markets to "fears of a recession". They can't just provide facts and avoid narrating.

Even worse, it's becoming more and more tempting to fall back on narratives to deal with our increasingly complex world. Roughly 90 percent of all the data in the world was generated in two years ending 2013. We create as much data in two days as we did from the period of the dawn of civilization to 2003.

That's a lot of data. And this barrage of information presents a unique problem for us as investors. It means that if we have a belief about a stock, we can probably find countless facts to fit into our bullish or bearish narrative, allowing us to impose narratives on data patterns after the fact. Even if those narratives might be misleading--or false.

We ourselves fell for the compelling water narrative, with its bold projections for a ~40% rise in demand over the next 15 years, when we wrote that overpriced Mueller Water Products (MWA) "has a very compelling narrative. It sells products that move water, measure water, and repair leaky pipes to save water. All of these are great businesses." We succumbed, similar to Ryan Floyd writing for the CFA magazine:

My eye saw a perfect investment, fitting the evidence into a story familiar from books and speeches on great businesses. [...] But the reality behind the perception was quite different. Years of inflation and currency depreciation obscured the value of the company's fixed assets, making return on invested capital look higher than was actually the case. The company was losing its dominant market share (a legacy from earlier government regulation against competition), and its main product didn't come from its own research facilities but instead consisted of repackaged imported goods. The point is that my senses deceived me.

As like the writer above, our narrative-inspired call was one of the few times we've gotten away from our philosophy of analyzing businesses based on fundamentals and price, and it wasn't a great trade. The narrative caused us to overlook things we normally wouldn't have.

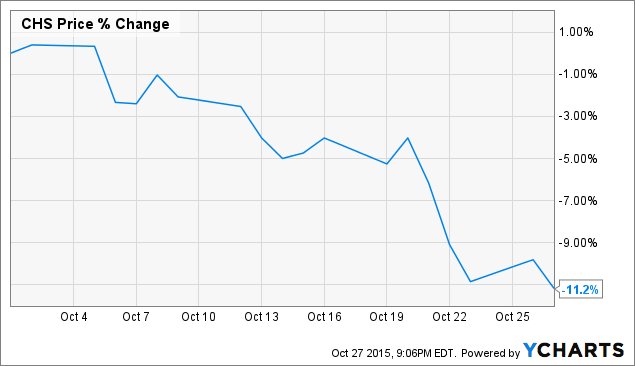

One company that recently scored off the charts on our Rudeness Indicator was mature women's clothing chain Chico's FAS (CHS). We received a ton of rude comments (some of which have been since removed) such as "you are an idiot," "what a stupid article.. in 4 words," and "go drink some cranberry juice." That last one was just kind of bizarre.

And not even a month later, the stock has lost over ten percent of its value.

Source: YCharts

Did CHS really represent value for investors at that earlier price? Better yet, could something have warned those optimistic investors? Perhaps. Research comparing the effectiveness of forecasts based on algorithm vs. human shows that algorithms consistently outperform humans in predictions. So could it be that an objective focus on the fundamentals would've warn investors to steer clear? Let's look at a few proven strategies:

Overall, the best performing strategies are EBIT to enterprise value and return on capital, EBIT to enterprise value alone, and earnings yield (the inverse of the P/E ratio).

In reality, CHS would have failed based on the above algorithmic requirements. CHS's EV to EBIT, for example, has gone from bad to worse. Its earnings yield has been in disastrous decline for years, lower than a high-interest savings account.

Source: YCharts

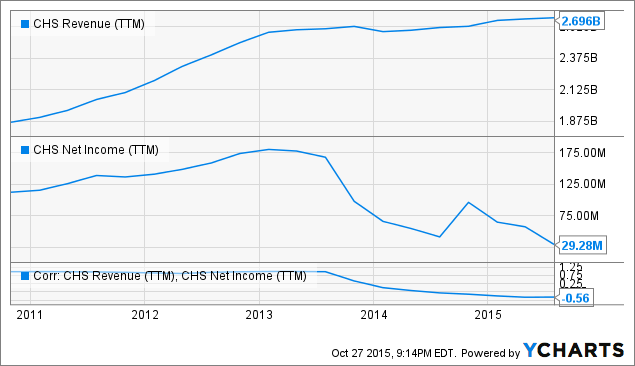

While bullish investors provide story-telling narratives about how nice Chico's FAS stores are to shop in, or how fashionable the clothes, or how America is getting older, the reality is that its fundamentals don't paint the same rosy picture. Consider, further, that its revenue and net income are actually negatively correlated.

Source: YCharts

Source: YCharts

When it looks like more growth is a bad thing for investors' bottom line, we think it's a sure-fire sign to avoid that company, at least until that situation improves.

When it looks like more growth is a bad thing for investors' bottom line, we think it's a sure-fire sign to avoid that company, at least until that situation improves.

As investors, we can't afford to become comfy in our narratives. As Polkinghorne (1987) suggests, narratives "exhibit" an explanation -- they don't "demonstrate" one. That means that the burden is on us to prove our perspective, to turn off our simple stories, to strive to understand the opposing point of view and not lash out in a fit of anger worthy of the Rudeness Index. There may be no cure-all for our story-telling brains. But as Chico's FAS investors have discovered, ignoring fundamentals in favor of a comfy narrative is a dangerous way to invest.