Epiq Systems (NASDAQ:EPIQ) is an activist-related play in the legal service industry. Essentially, they provide a platform that enables integrated technology solutions for the legal profession combining proprietary software and a strong understanding of the subject matter to assist clients with the efficiency of technology. In late 2014 and early 2015, the shares were an activist buyout play with the largest current shareholder making a $20 per share bid for the company. The board rejected the offer and the shares have struggled since.

Our focus today is on the value of the core business at these levels and the efforts at growing the business's profitability. Their solutions are intended to streamline the administration of bankruptcy, litigation, and regulatory compliance areas. Their managed solutions for eDiscovery, document review, legal notification, and the controlled distribution of funds, are core assets to law firms.

We think the shares offer a compelling buyout target and value restructuring play at current levels.

(Source: Investor Presentation)

eDiscovery Potential Market Opportunity

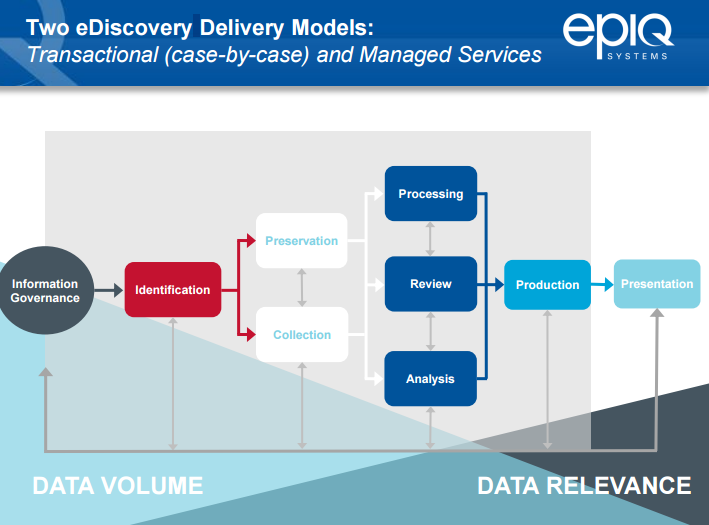

The electronic discovery (or eDiscovery) process in the legal profession is the exchange of information. Discovery allows their law clients to move away from the paper environment and organize large volumes of data and documents. The two parties in a civil suit exchange information in relation to each other's claims and defenses. This is the company's core asset and what we think where most of the value in the shares lay.

The competition in the space is increasing but we see Epiq as having a competitive advantage compared to the upstarts as they have a full service offering. The market for the business is growing very rapidly on the back of two strong trends: growth away from paper and towards electronically stored information, and increased litigation. The amount of data is projected by IDC to grow at a massive rate doubling every two years. In addition, the increasing amounts of litigation and regulatory inquiry is providing a secular growth story in the industry.

We think the market is overpricing its competitive pressures in both document review and in technology processing. While cost is a small factor in many client encounters, we think Epiq is uniquely positioned to benefit from its scale. Additionally, we think cost is not the primary driver for much of the competition. The growth in volumes and the scale of Epic allows it to market itself as the go-to solution for declining pricing advantages. The unique business model is also a differentiator has they have two delivery models, something not offered by most of the competition. (more below)

(Source: Investor Presentation)

We think the market in this space is likely to see some consolidation over the next several years as law firms will need to adopt the technology in order to compete effectively. We also see the business as having significant cost infrastructure that could be addressed despite the 50% gross margins and 20% EBITDA margin.

Bankruptcy Piece A Headwind But Under-Appreciated

The "problem" with the business is that it is counter-cyclical, so during bad times, the business thrives and during economic expansions, struggles. This is a highly misunderstood piece of their business. In 2015, the segment is expected to generate $76 million in revenue or approximately 16% of total firm wide revenue and 24% of EBITDA. But during 2010, the segment generated 45% of the firm's revenue and 55% of EBITDA.

The segment provides bankruptcy and settlement solutions focused on the debtors, creditors like banks, and bankruptcy trustee clientele. Their proprietary software product is called Automated Access to Court Electronic Records (AACER), which is used to track developments in all US bankruptcy cases applying sophisticated algorithms to classify docket filings automatically in each case. The product has a compelling return on investment given the significant cost savings they provide their clients by eliminating the manual attorney review of each case in the portfolio.

There are only a handful of real competitors in the space, such as Garden City Group and Kurtzman, Carson Consulting. Epiq is the number 2 player in the space with a strong competitive position in the market. Most of their revenue in the segment comes from Chapter 11 bankruptcies (restructurings) which we think is likely to see growth over the next two years.

We think the counter-cyclicality of the business coupled with the long-term potential uptick in restructuring activity as the large amount of leveraged loans globally mature, is likely to drive the business near-term. This is especially acute in the bank loan and high-yield loan space especially related to the energy sector. We think this is likely to drive bankruptcy and loan restructuring over the next two years which could substantially increase revenue in their bankruptcy business beyond what the minimal Street coverage expects.

(S&P Capital IQ)

We think the amount of leveraged loan defaults are likely to jump in 2016 due to the lower oil prices affecting the energy market. The current default rate around 1.9% is expected to climb as more and more energy companies enter into bankruptcy protection. In December, three more energy companies filed including Vantage Drilling, Energy and Exploration Partners, and Magnum Hunter Resources. We would point to the current institutional term loan market trading down below 90 cents as indicative of unease in the space, down from over 95 in early December.

But looking out beyond the very near-term, we think historic default rates will top long-term averages as early as late 2016. This should have the effect of improving the bankruptcy segment as the litigation surrounding the amount of issuance, which has been massive these past several years, is likely to be enormous. Between now and then, the results of the segment will likely be very lumpy owing to the nature of the business model. However, it is a highly profitable business with significant barriers to entry.

Valuation

The company generates revenue through data hosting and volume-based fees, professional services fees, and deposit fees on a set percentage of Chapter 7 assets assigned to Epiq's clients. Pricing pressures, which we addressed above, has masked the true revenue growth potential of the business. There is little sell-side coverage on the name with just three analysts assigned to the business. We think this adds some of the mispricing in the name.

EBITDA margins have declined in recent years on the back of increased SG&A spend. In 2015, they made a number of changes to the operations of the business. One of the primary areas of focus was on efficiency and productivity while reducing the spend on investments to support growth. Many of these programs aimed at new products were not viable and have since been shut. SG&A expense was just $117 million in 2012 but rose substantially to $166 million by 2014.

In response, the company reduced their occupancy expenses given their New York City location- as well as Miami, London, and Chicago- reducing their overall space and lowering fixed costs significantly. This should assist in the growing of their operating leverage capabilities as the fixed cost base is reduced. They have also consolidated their offshore facilities and managed headcount down. Lastly, they have completed the integration of their sales, financing, and human resources departments.

We believe there is an upside move in the shares that is likely in the next year on the back of the outperformance expected in the bankruptcy segment along with pricing stabilization in the eDiscovery business. We do not think investors are currently incorporating this into their forecasts. Below is our segmented forecasted breakdown of our expected results over the next two years.

| Revenue | 2014 | 2015 | 2016 | 2017 |

| eDiscovery | 298 | 350 | 395 | 440 |

| Bankruptcy | 83 | 90 | 100 | 105 |

| Settlement | 64 | 70 | 70 | 70 |

| Reimbursed Costs | 30 | 30 | 30 | 30 |

| Total Revenue | 475 | 540 | 595 | 645 |

| EBITDA Margin | 20% | 20% | 20% | 20% |

| EBITDA | 97 | 110 | 120 | 130 |

| Multiple | 8 | 8 | ||

| EV | 960 | 1040 | ||

| Net Debt | 400 | 400 | ||

| Equity | 560 | 640 | ||

| Shares | 38 | 38 | ||

| Value | $ 14.74 | $ 16.84 | ||

| Upside | 19% | 36% |

We think the shares are worth just under $15 and that the shares offer a compelling, albeit higher-risk (speculative) play on niche technology that we think is oversold. Our valuation is primary due to the 30% drop in the shares over the last twelve months, while EBITDA estimates have fallen by just 4%. We believe the shares are cheap enough to warrant another buyout offer but that may not be $20 like the previous.

Conclusion

We believe the low coverage by the Street and the misunderstood business model which incorporates significant amounts of pricing pressure into their core business, and nearly permanent headwinds into their bankruptcy segment, is decreasing sentiment and creating the opportunity. Our thesis is driven by our expectation of stabilization in the core eDiscovery business which, on the back of generally accepted volume growth, would grow the segment's revenue by low double-digits over the next two or three years. Meanwhile, the misunderstood asset is their bankruptcy business which we think stands to benefit from the massive leveraged loan and high-yield market, especially surrounding energy companies.