The equity market in the U.S. has been moving higher for two reasons that are interrelated. First, the correlation between stock prices and crude oil has resulted in a rebound in equities as oil has rallied on prospects for the upcoming meeting in Doha. The potential for improving supply and demand fundamentals in the oil patch has bolstered price. Secondly, the dollar has been moving lower, meaning that U.S. exports have become more attractive increasing the odds of growth for corporate profits amongst U.S. multinational corporations.

However, two areas of the world continue to weigh on the outlook for equities in the U.S. and around the world. Europe continues to stagnate under the weight of a lethargic economy, an ongoing humanitarian refugee crisis and the potential for terrorist attacks. Asia continues to be a thorn in the side of the U.S. economy and the rest of the world. These two issues were recently highlighted in comments by the U.S. central bank with respect to short-term interest rate policy. Chairperson Janet Yellen has repeatedly stated that the Fed is practicing a new kind of monetary policy called "gradualism." This amounts to a "wait and see" orientation in terms of economic events in Brussels, Beijing and Tokyo. The Fed seems to have abandoned a U.S. data sensitive approach to interest rate policy and exchanged it for a watchful eye on foreign market events. If they are concerned, you should be, too.

While the chances of a new European meltdown are unlikely, the high odds play is that the economy on the continent will continue to limp along as the ECB prints money and charges storage for deposits with negative interest rates in an attempt to encourage spending and borrowing and discourage saving.

When it comes to Asia, things are different -- the Fed is fearful of Asian contagion.

China

The first severe shock to U.S. equity markets came on August 24, 2015 when the Chinese government suddenly devalued their currency, the yuan. Last year cracks began to appear in the Chinese economy. The economy of the nation that had experienced double-digit growth for years began to slow. In response to slower growth, the government introduced a number of stimulative measures. They lowered domestic interest rates, floated a massive bond meant to increase investment in infrastructure and when the domestic stock market started moving lower, new rules and regulations designed to inhibit selling and encourage buying were put in place. The Chinese policy of "new normal" amounted to an acknowledgment of slower growth in the nation and governmental action to create an environment of slower but stable growth. Meanwhile, the economy continued to cool and the effects were felt around the world.

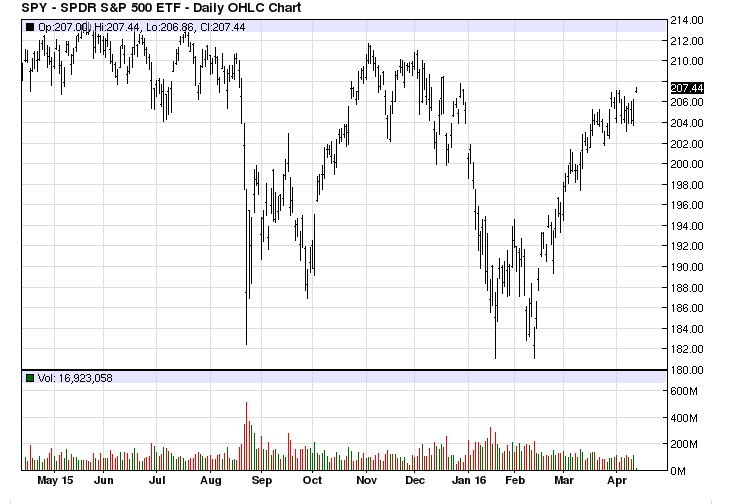

China has been the demand side of the fundamental equation due to their role as the world's leading consumer of commodities by virtue of their population and growth. As the economy slowed, commodity prices moved lower. When the Chinese stock market continued to move lower last summer, the government decided that encouraging exports by lowering the value of the yuan would spark growth. However, it resulted in a tsunami of selling around the world. Fear and uncertainty gripped markets, and the U.S. equity markets spiked lower in response to volatility in Chinese markets.  The daily chart of the SDR S&P 500 ETF highlights the first cascade of selling that hit U.S. markets late last summer. The market proceeded to recover from the sharp sell-off, however, on the first day of 2016 another wave hit world markets.

The daily chart of the SDR S&P 500 ETF highlights the first cascade of selling that hit U.S. markets late last summer. The market proceeded to recover from the sharp sell-off, however, on the first day of 2016 another wave hit world markets.

Even before U.S. markets opened on January 4, the first trading day of the New Year, the die was cast. Chinese equity markets greeted the New Year by plunging. This resulted in a six-week period of selling that took the market to lows on February 11, 2016. At those lows, the S&P500 stood 11.5% lower on the young year. Since then, the equity market has recovered but it certainly remains nervous in terms of worries about when the next shoe will drop in China. Aside from slower growth, China has a massive debt problem.

After the financial crisis in 2008, China experienced a huge credit surge with new loans increasing by 95% in 2009. The government offered cheap credit to build infrastructure from apartment complexes to airports and new roads. Lending grew at twice the rate of GDP -- many companies grew to multi-billion dollar valuations only to collapse when they could not profit; surplus capacity drove prices down. The number of non-performing loans mounted. The government has been considering swapping debt for equity but the value of that equity is dubious and this puts the banks in a difficult position. The Chinese are considering a $1 trillion yuan plan to address bad debts, but this might only amount to a band-aid on a gapping axe wound. Solving the debt issue will likely require a massive recapitalization of the Chinese banks.

At the same time, economic turbulence and the slowdown in China is causing wealthier citizens to sell their yuan to move money away from the nation to preserve value. One of the initiatives of the new normal policy is a crackdown on corruption, which is adding to the desire of some to get their money out of the country as the policy could be subjective and political in nature. As more money leaves the country, there is less left to be spent within China's borders exacerbating the economic problems.

Japan

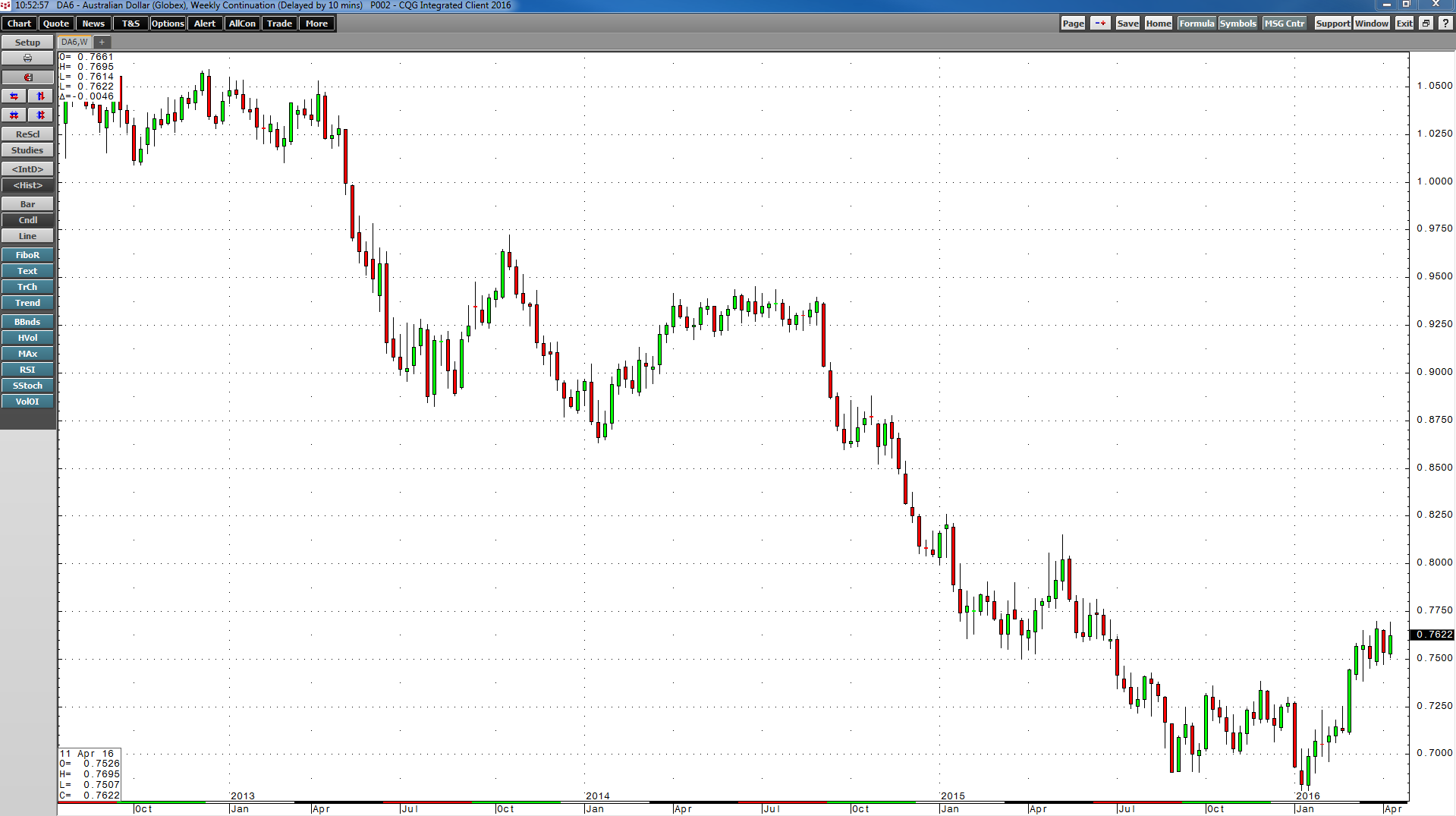

When China sneezes, the rest of the world catches a cold; when the Chinese economy slows, the rest of the world grinds to a halt. Just look at the action in currencies of nations that depend on raw material revenues. Less demand for commodities has caused the Australian dollar to plunge over recent years.  As the weekly chart of the Australian dollar highlights, the currency dropped from over $1.05 against the U.S. dollar in April 2013 to lows of around 68 cents in early 2016. Since then the A$ has recovered as commodity prices have bounced. Australia has been a supermarket for raw material hungry China over recent years and the slowdown has cut revenue flows to the nation. Other commodity currencies have also plunged on slower Chinese economic growth; the Brazilian real and the Canadian dollar are two such examples.

As the weekly chart of the Australian dollar highlights, the currency dropped from over $1.05 against the U.S. dollar in April 2013 to lows of around 68 cents in early 2016. Since then the A$ has recovered as commodity prices have bounced. Australia has been a supermarket for raw material hungry China over recent years and the slowdown has cut revenue flows to the nation. Other commodity currencies have also plunged on slower Chinese economic growth; the Brazilian real and the Canadian dollar are two such examples.

The effect of the slowdown in China has been felt most dramatically in neighboring nations in Asia. Recently, economic weakness in Japan has caused the central bank and Abe government to cut short-term interest rates further into negative territory. While the central bank intended this to be a stimulative measure to jumpstart a flat-lining Japanese economy, the response was a counter-intuitive jump in the value of the yen.

A prolonged period of low interest rates in Japan led to Japanese borrowing and investment in equity markets around the world. The biggest recipient of those investment funds were U.S. equity markets, the biggest and most liquid in the world. To make those investments with borrowed money in cheap yen, selling borrowed yen and buying dollars to invest in the U.S. markets or a "yen-carry trade" resulted. When the Japanese central bank made money even cheaper, the yen actually rallied as concerns about global equity markets caused selling of dollars and buying back those short yen. The stronger yen makes a weak economic landscape in Japan even weaker as Japanese goods become more expensive in other currencies, inhibiting exports. At the same time, demographics continue to weigh on the Japanese economy. The aging population has created a situation where productivity has declined dramatically. Japan now sells more adult diapers than baby diapers to its citizenry each year. Finally, the slowdown in China has not helped Japan.

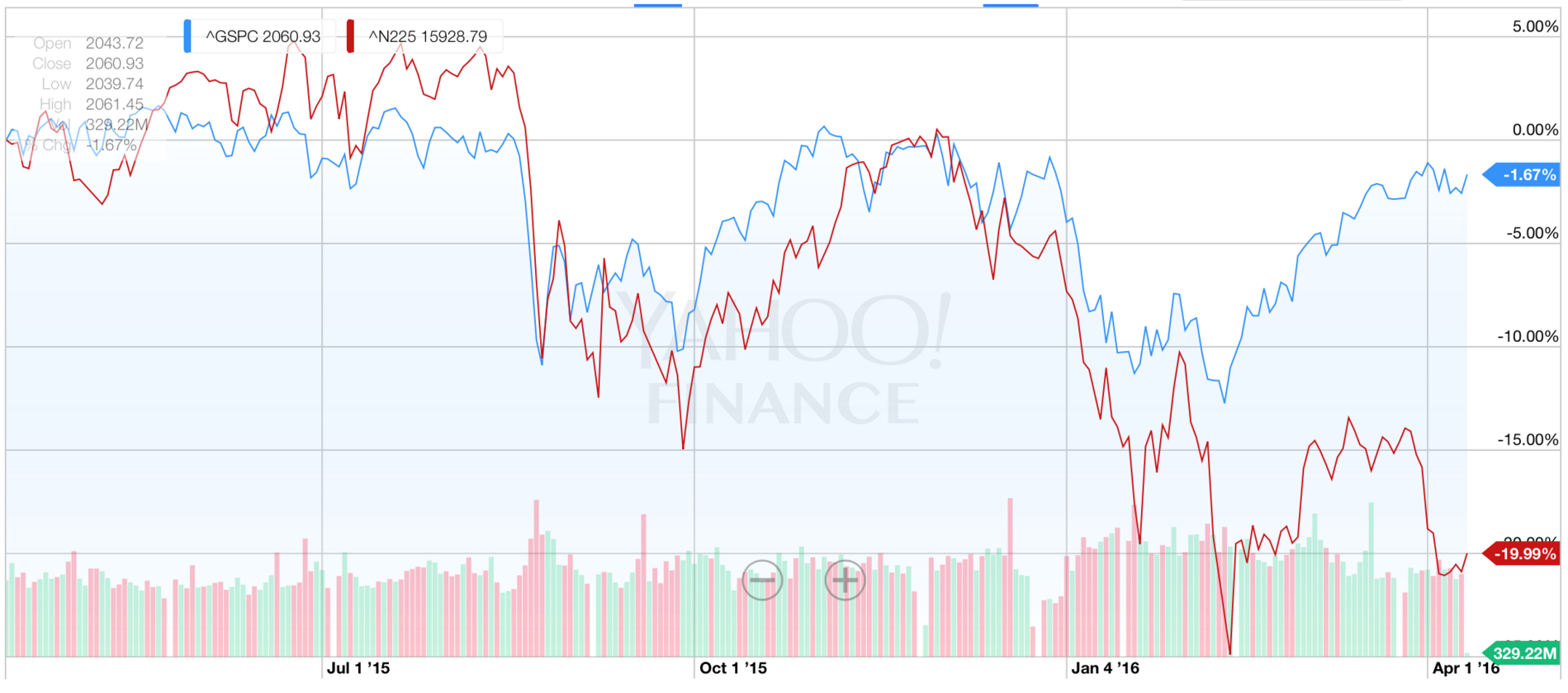

One of the starkest signs of problems in Asia is the divergence between the S&P500 index and the Japanese Nikkei equity index.  Recently, the S&P 500 was trading around unchanged in 2016 with the Nikkei down 20%. U.S. stocks are trading over 26 times earnings, according to the Shiller CAPE ratio, while Japanese stocks were trading at an average P/E of under 17 times earnings. Japan's stock market may be more in tune with the global economic landscape than the U.S. market.

Recently, the S&P 500 was trading around unchanged in 2016 with the Nikkei down 20%. U.S. stocks are trading over 26 times earnings, according to the Shiller CAPE ratio, while Japanese stocks were trading at an average P/E of under 17 times earnings. Japan's stock market may be more in tune with the global economic landscape than the U.S. market.

Central Bank Woes

Central banks around the world have been battling economic issues since the global economic crisis in 2008. Quantitative easing, lower interest rates, currency intervention and other monetary tools designed to provide stimulus have been the norm rather than the exception in Europe, China, and Japan. Central bankers have become monetary firefighters moving from one economic blaze to the next over recent years. There are few signs telling us that conditions are turning a corner in Europe and Asia these days.

The world has become a smaller place due to technology. Economic events around the world have a direct impact on the U.S. economy. The U.S. Fed used all of those tools to battle its own economic crisis in the years following 2008 and moderate growth has returned to the economy. The Fed closely monitors world economic events and incorporates this data into their decision-making process about U.S. interest rate policy. The U.S. economy has experienced growth and stability over recent quarters that justify further rate hikes. However, the Fed has recently displayed a heightened degree of sensitivity to the data that comes from outside U.S. borders in 2016. "Gradualism" these days is synonymous with concerns about the state of the European economy, but even more with the potential for more Asian contagion. The Fed is worried about more shocks like the ones seen last August and at the beginning of 2016 coming from Asia. It seems that they are willing to risk getting behind the inflation curve to be gradual and sensitive to these foreign risks.

Gold and the IMF

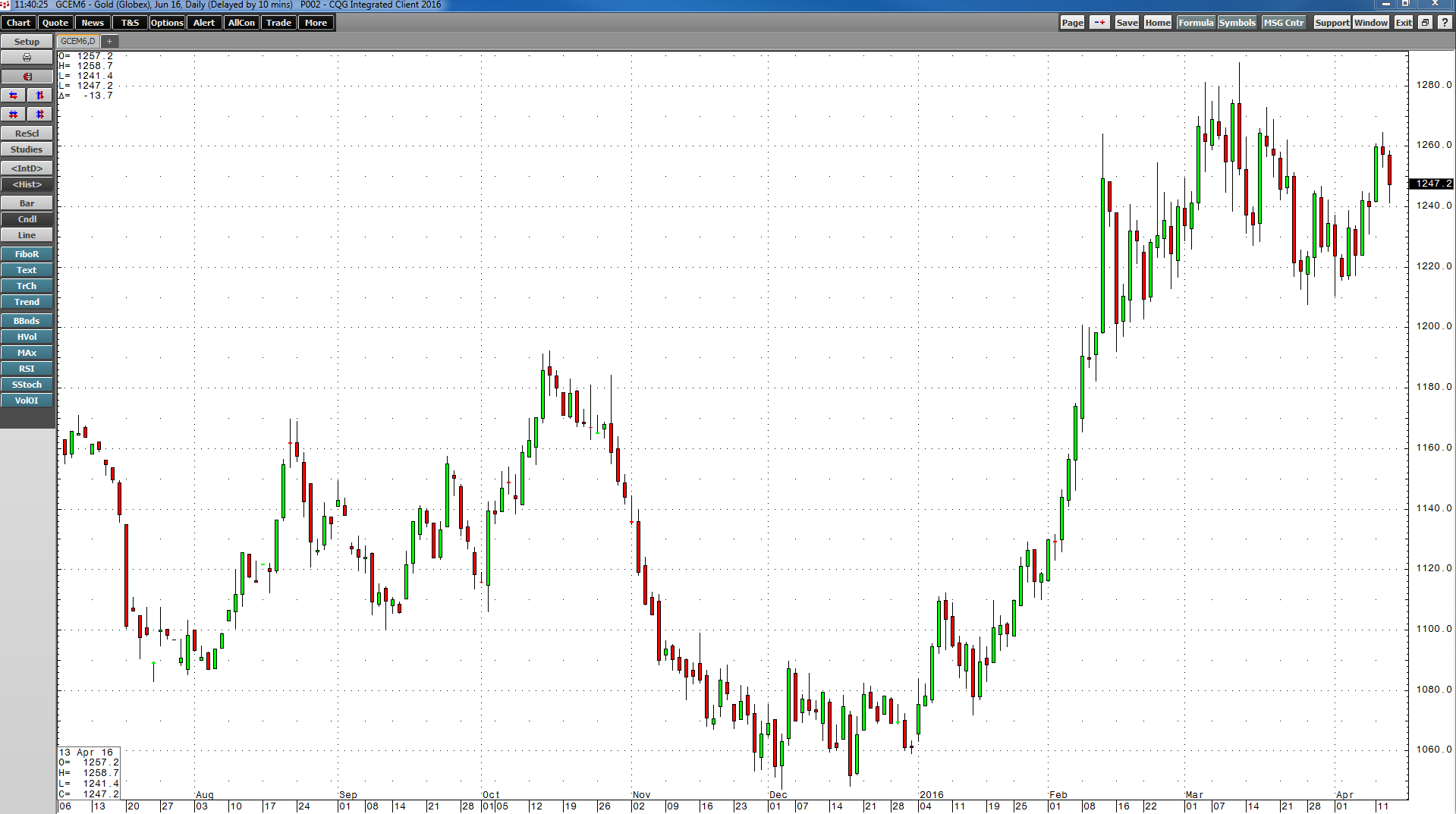

Gold is a barometer of fear and uncertainty; it is also a time-tested hedge against inflation. Gold has been a means of exchange, a currency for thousands of years that pre-dates all paper currencies in circulation around the world today. Central banks hold over 30% of all of the gold ever produced in the history of the world as part of their foreign exchange reserves. Gold has been one of the best-performing assets in 2016.  Gold finished 2015 at around $1060 per ounce. As of Wednesday, April 13, 2016, the price stood at around $1245 -- an increase of over 17.4% in three and a half months. Gold has been signaling that all is not well with the global economy. Recently, many major commodity prices have bounced sharply off multi-year lows. Gold could be signaling that inflation is starting to rise.

Gold finished 2015 at around $1060 per ounce. As of Wednesday, April 13, 2016, the price stood at around $1245 -- an increase of over 17.4% in three and a half months. Gold has been signaling that all is not well with the global economy. Recently, many major commodity prices have bounced sharply off multi-year lows. Gold could be signaling that inflation is starting to rise.

At the same time, the International Monetary Fund recently downgraded its forecast for global economic growth in 2016. They lowered the growth outlook to 3.2% from their 3.4% forecast in January. The IMF cut the growth rate in the U.S. from 2.6% to 2.4%. While they increased the outlook in China to 6.5% from 6.3%, they halved their forecast for Japan to negative 0.5%, citing that 2017 may even be worse as a new consumption tax hike takes effect. In Europe, they cut their forecast from 1.7% to 1.5% growth. They also cut their outlook for growth in Latin America and Sub-Saharan Africa.

A strong gold price and slower global growth are signals that all is not well in the global economy. The Fed's reluctance to hike U.S. interest rates and their policy of "gradualism" provides validation of a weak economic landscape.

Bad news for stocks

After the rebound in equity prices in the U.S. from the carnage over the first six weeks of 2016, the S&P500 is now around 1.9% higher on the year as of April 13, 2016. Since the February 11 lows, this equity index has climbed over 13%. It seems that equity markets have shrugged off the concerns that have held the U.S. Fed back from increasing rates. The rebound in stock prices has created an "all is well" mentality in investors' minds. The emotional impulse of missing ever increasing equity values is a powerful motivating force. However, in successful investing it, is important to remove emotion from the equation and take an objective look at the economic landscape. The Carden Smart Wealth Indices provide an emotion-free view of markets and can dampen volatility when market activity flashes warning signs.

While U.S. equity prices have been on the rise for over two months now, the Carden Smart Hedge Index remains in cash since mid-December before this recent bout of volatility commenced. The Fed is concerned about contagion. Be careful out there. In all markets, volatility is likely to continue throughout 2016.

As of the publication date of this report, Carden Capital LLC, Carden Futures LLC and their affiliates (together the "Carden Companies"), may have positions in (whether long or short) and or options positions (whether long or short) in any of the securities, futures, or companies covered herein and may stand to realize gains in the event that the price of any security, future or stock changes. Following publication of the report, the Carden Companies may transact in the securities, futures and derivatives of any company or market covered herein.

Neither I nor the Carden Companies have any obligation to continue offering reports regarding the securities, futures or companies covered herein. Reports are prepared as of the date(s) indicated and may become unreliable because of subsequent market or economic circumstances.

Any investment involves substantial risks, including, but not limited to, pricing volatility, inadequate liquidity, and the potential complete loss of principal. This document does not in any way constitute an offer or solicitation of an offer to buy or sell any investment, security, or commodity discussed herein, or any security in any jurisdiction in which such an offer would be unlawful under the securities laws of such jurisdiction.