silvestra

Co-authored with Hidden Opportunities

The commonly held belief is that retirement readiness hinges on reaching a specific dollar figure, often based on personal calculations or whispers within social circles. However, this approach overlooks a crucial reality: everyone's retirement needs are unique. Unexpected expenses lurk around every corner, potentially shattering carefully crafted plans. Consequently, individuals may find themselves toiling away for years, striving to hit an arbitrary financial milestone they don't need, or worse, retiring only to realize their funds fall short of sustaining their desired lifestyle.

As an income investor, my calculations are based on recurring cash flows from my nest egg than the value of my nest egg itself. Do you remember Gwen Stefani's song "Rich Girl" from her 2004 debut solo studio album "Love. Angel. Music. Baby.?" The lyrics describe her dreams of fame and riches from the perspective of an Orange County girl.

If I was a rich girl

Na-na-na-na-na-na-na-na-na-na-na-na-na-na-na

See, I'd have all the money in the world

If I was a wealthy girl

No man could test me, impress me

My cash flow would never ever end

'Cause I'd have all the money in the world

If I was a wealthy girl

As Ms. Stefani sings, consider the emphasis on a never-ending cash flow. This is the most important element of financial independence. Let us look at two excellent sources of long-term cash flows.

Pick #1: RLJ-A Preferred - Yield 8%

RLJ Lodging Trust (RLJ) is one of the largest U.S. publicly traded lodging REITs in terms of the number of properties and room count. The REIT operates 96 hotels across the country, with 2/3rd of its portfolio comprising urban properties and ~51% of the adjusted EBITDA from sunbelt states in the U.S.

The company has demonstrated a strong rebound since the global pandemic, with FY 2023 occupancy rising to 71.8% (up from 68.9% in FY 2022), and Average Daily Rate going up to $196.4 (from $187.8 and exceeding pre-pandemic levels), and RevPAR rising to $141.09 (from $129.4). During FY 2023, RLJ grew its RevPAR by 9% YoY, exceeding the industry average by 2x. Notably, during Q4, the RevPAR growth was 5.2% YoY, beating the industry by 4x despite being a relatively slow season.

During the fiscal year, the hotel REIT repurchased $77.2 million of common shares and raised its dividend twice, essentially doubling the payout vs. FY 2022. Since 2018, the hotel REIT has purchased $300 million of common shares, representing ~13% of the float, demonstrating an excellent commitment to returning value to shareholders.

RLJ is heavily focused on external growth catalysts, pursuing acquisitions and internal conversions to boost profitability. Since 2021, the hotel REIT has made four high-quality accretive acquisitions, with a NOI (Net Operating Income) Yield (a financial metric used to evaluate the profitability of an income-producing property) between 7.5-8.5%. In addition, the company is pursuing two conversions, projected to provide $14-18 million in incremental EBITDA.

89% of RLJ's debt is fixed-rate or hedged, with a weighted average interest rate of 4.12%. The hotel REIT has only $200 million worth of debt maturing this year, adequately supported by its ~$1.1 billion liquidity, including its $500 million cash position. Source

March 2024 Investor Presentation

RLJ has one convertible preferred (RLJ-A) that has an interesting element that makes it a perpetual source of income. RLJ cannot redeem this preferred but can force conversion to common stock only if RLJ trades at or above $89.09 for 20 out of 30 trading days. As such, for the preferred to become convertible, the common stock has to experience a staggering 672% upside, making it quite an improbable situation.

- $1.95 Series A Cumulative Convertible Preferred Shares (RLJ.PR.A)

RLJ-A is attractively priced, offering an 8% annualized yield. During FY 2023, RLJ generated $76.4 million in net income and spent $25.1 million towards the preferred dividend. The preferred dividend is covered 10.3x by the company's adjusted FFO of $260 million and 14.5x by the adjusted EBITDA of $364.4 million. RLJ raised its common stock distribution twice in FY 2023, resulting in a total expense of $49.1 million.

For FY 2024, RLJ expects 2.5-5.5% YoY RevPAR growth and adjusted EBITDA between $360 - $390 million. Based on these projections, we expect the hotel REIT to continue growing its common distribution, thereby providing solid protection for the cumulative preferreds.

Pick #2: BTI - Yield 10%

British American Tobacco p.l.c. (BTI) (will be referred to as BAT in this article) has started FY 2024 with a bang, cashing in on its prudent investment from over 100 years ago. BAT sold a 3.5% position in India-based ITC Limited (NSE: ITC) to raise over $2 billion. With the proceeds, BAT executed a share buyback program, purchasing 280,000 of its shares at prices ranging between $30.15 to $30.45/share.

ITC's market cap stands at ~$65 billion, and BAT still owns a 25.5% position in the company. Contrary to popular opinion, ITC is not owned by the Government of India, nor is it a tobacco-focused business. It is a public company with a diversified presence across industries such as FMCG, hotels, software, packaging, paperboards, specialty papers, and agribusiness. The conglomerate has 13 businesses across five segments and exports its products to over 90 countries. BAT's stake in ITC is currently worth ~$17 billion, compared to BAT's market cap of $65 billion.

BAT CEO Tadeu Marroco recently dismissed the news about a potential change to having a primary listing in the United States as a distraction, pointing out the benefits of the U.K. listing and its no withholding taxes for international investors.

Kenneth Dart, a Cayman Islands-based billionaire heir to the American foam cups fortune, is also one of the largest shareholders of BAT. His investment vehicle, Spring Mountain Investments, recently increased its stake in the tobacco company.

Note: BAT is a U.K. corporation that declares and pays dividends in GBP. The amount received by U.S. investors will vary based on USD-GBP conversion rates. The U.K. does not withhold taxes on dividends paid to international investors.

BAT has been focused on internally growing its new categories, with consistent innovation in products since 2013. Source

British American Tobacco Website

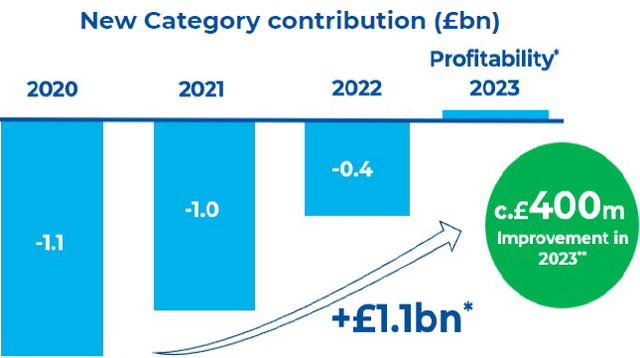

These new non-combustible products segment delivered a terrific 21% YoY revenue growth in FY 2023, and achieved profitability two years ahead of schedule. Source

March Investor Presentation

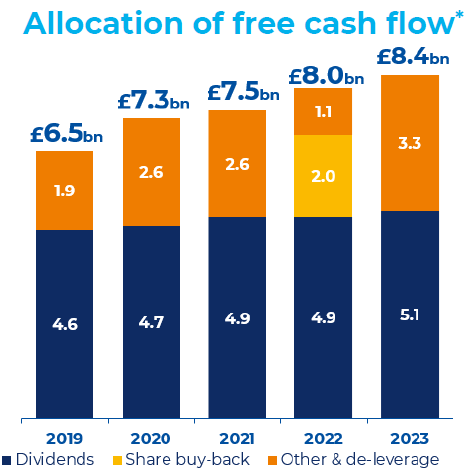

BAT's new category growth is fueled by the company's massive exposure to emerging markets like Bangladesh, Pakistan, and Indonesia, where combustible cigarettes are very popular. This "legacy" category still achieves top-line growth in these markets despite price hikes. Thanks to rapidly growing new categories and a highly sticky combustible business, the company is a Free Cash Flow machine, with £8.4 billion generated in FY 2023. This places the £5.1 billion annual dividend at a modest 60.7% payout ratio. The company utilized £3.3 billion towards deleveraging and other expenses.

March Investor Presentation

BAT reported reduced leverage of 2.6x at the end of the fiscal year, and the tobacco company carries an investment-grade BBB+ rating from leading credit agencies.

For FY 2024, the company's guidance includes low single-digit revenue and organic adjusted profit from operations growth, and management expects progressive improvement in 2025. For 2024, we expect continued FCF growth and a modest dividend increase.

Author's Calculations

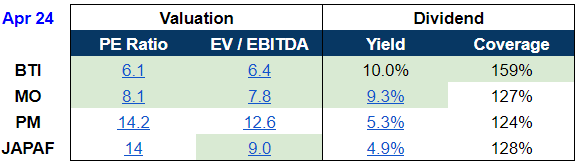

BAT is currently the cheapest tobacco stock and sports the highest yield and dividend coverage. We consider the recent sell-off to be a terrific buying opportunity for long-term income generation protected by a highly stable and inflation-resistant business model.

Conclusion

The Amazon River flows continuously, perpetually carrying water from its headwaters in the Andes Mountains. Due to the large amount of water it receives from rainfall, and its extensive drainage basin, the river is expected to remain a vital and flowing water body for the foreseeable future.

Investing in RLJ-A and BAT can provide a similar sense of perpetuity for your income, akin to the enduring flow of the mighty Amazon. We strive to grow passive income through a diversified portfolio of dividend-payers. Our model portfolio of over 45 securities is designed to provide an overall yield of +9% to enable a rich lifestyle in retirement. Our approach emphasizes not only diversification by ticker, but also by industry and security class, safeguarding your income against the volatility of markets and securing the retirement you deserve.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

If you want full access to our Model Portfolio and our current Top Picks, join us at High Dividend Opportunities for a 2-week free trial.

We are the largest income investor and retiree community on Seeking Alpha with +8000 members actively working together to make amazing retirements happen. With over 45 picks and a +9% overall yield, you can supercharge your retirement portfolio right away.

We are offering a limited-time sale for 17% off your first year. Get started!

Start Your 2-Week Free Trial Today!