I have been focusing on GE during the weekend. I see a significant potential in the "digital industrial" concept, and the company seems to be on the right track with its restucturing. A long-term buy? Most probably, yes.

However, the amount of uncertainty regarding the recent industrial revenue dynamics is somewhat concerning, and I would not expect a strong improvement over the short-term. The relatively unpredictable share price reactions to the ongoing segment disposals only further intensify my skepticism. I would also view the dividend freeze as a rather bearish catalyst taking into account the amount of dividend-related talk and the memories of the dividend cut in the past (even though I am not suggesting that one might happen soon, this might still impact the investor sentiment if the operating performance gets worse during the next quarters).

To sum up, the digital focus is a large plus, but the near-term risk of holding GE might not be entirely compensated by the dividend. The ongoing disposals and frequent news coverage makes the stock quite unpredictable over the short-term, and, given the current investor sentiment, I would view the possibility of a downside as more probable over the next 1-5 months.

Here are some good links to support my view:

- Jack Welch, the former CEO of General Electric came up with a bearish view on the company's near-term prospects and the overall economy: "We're in a slowdown. There's no question […] I will say clearly that we're in for a slowdown here. We have been in one, Neil. We had 0.7 percent (growth) in the fourth quarter and it's tough to see us doing a lot better in the first quarter of...this year […] You have got regulation on regulation on regulation. You're strangling this economy. And we're starting to see it. We haven't had a real recovery. It's been peanuts us all along," Jack Welch said during the interview with Fox News in February.

- The CEO's letter, published on February 29, shed more light on the company's long-term goal of becoming a Digital Industrial company. The letter, which can be accessed here, is a must-read for all GE investors. It clearly indicates the compelling future prospects and can be viewed as an ultimate base for long-term bullish thesis. However, despite clarifying the company's long-term focus, the letter does not sound too convincing when it comes to the near-term performance of the company: "To sustain this performance, we will have to win in challenging global markets […] What is unique in this cycle is the difficult relationship between business and government, the worst I have ever seen […] As a result, most government policy is anti-growth. In the U.S., we want exports but seem to hate trade and exporters; globally, governments love small businesses but then regulate them to death. And so, we perpetuate a cycle: slow growth, poor job creation, populism, low productivity, higher regulation, poor policy and more slow growth." The future will demonstrate the actual impact of the company's ongoing restructuring and will possibly make the company less recession-sensitive in the long run. However, for as long as the company faces headwinds during increasingly uncertain market conditions, the dividend might not compensate for the risk of holding it over a correction that might easily follow during the coming months.

- In early January, Motley Fool was wondering whether the company would keep its yield at 3% or increase the dividend over the course of 2016. " As noted in its plan to divest GE Capital, management remarked that "it plans to maintain its dividend at the current level in 2016 and grow it thereafter." CEO Jeff Immelt also told investors during the company's annual outlook meeting in December that it plans to sustain an attractive dividend yield - currently around 3% -- relative to peers," it wrote,"Dividends increases aside, GE still plans on returning a tremendous amount of capital in 2016 - roughly $26 billion, split between $18 billion in buybacks and $8 billion in dividends. In total, the GE Capital exit is expected to return more than $90 billion to shareholders in the form of dividends, buybacks, and a spinoff, by the end of 2018." That sounded like a great deal indeed. However, another Motley Fool's article was primarily focusing on the link between the ongoing disposals and the company's plans to return cash to its shareholders. It has pointed out a few relevant arguments:

- "Even though it's signed more than $146 billion in transactions, it's not getting $146 billion in cash to return to shareholders. For example, GE is selling its $30 billion commercial lending and leasing business to Wells Fargo. But it anticipates the sale will contribute just $4.2 billion to the $35 billion goal. The sale of its entire Mexican lending and leasing business will contribute just $100 million toward the goal."

- "Even if GE is able to raise $35 billion through GE Capital asset sales, it might have problems using the cash for buybacks. Because of GE Capital's former size and significance, it was designated a Systemically Important Financial Institution by the government. This comes with a lot of rules and regulations about whether and how GE Capital can return cash to its parent company."

- As of April 12, GE was the 3-rd most shorted stock on NYSE.

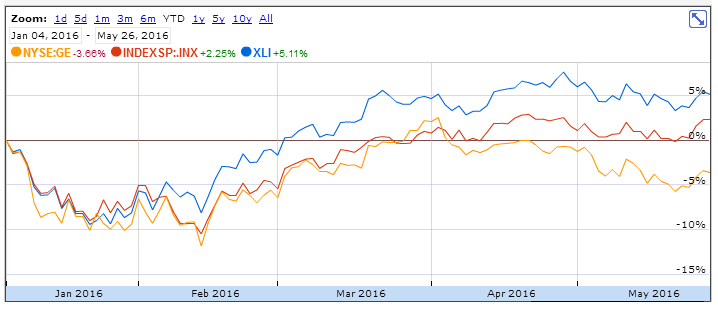

- And finally, middle of February marked the beginning of a significant uptrend for stocks. GE and the Industrial Select Sector SPDR ETF (XLI) have been close to replicating the performance of the broad stock market as represented by SPY (SPY), with GE underperforming both. It has briefly captured the leading position in late March, which eventually led to the stock reaching its short-term high in the beginning of April. It has been continuing to underperform both the XLI and SPY since then.

The digital segment's prospects are rather optimistic. However, for as long as the stock remains being market- and recession-sensitive, and its near-term prospects are just too uncertain, it might easily underperform the market in the nearest future.