IBM is again at a crossroads as its stock price languishes and market analysts question if it is on the right path. The Company has doubled down on predictive analytics as a core element of its transformation strategy - however, the decline in its low growth legacy businesses is outpacing the growth in its new business initiatives. Consequently, overall revenue has declined in each of the past fourteen quarters and earnings have continued to disappoint, resulting in the stock price and market value of the Company declining; leading to talk of activist investors, spinning off the Watson business and other perceived value creation strategies.

This blog is not an analysis of the equity value of IBM's stock, rather it is an attempt to review the progress of the Company's investments in analytics. Currency movements, share buybacks and other financial events will influence the Company's value, but its core strategy will be the ultimate determinant of its value. I believe the Company has made the right strategic moves and its investments in analytics position it well to capitalize on the growth in this area. The question for the Company is when, and not if, this strategy will pay off. The Company's transformation will accelerate as its investments in analytics, the cloud and other key areas move beyond customized work and into a repeatable and high margin business model and customers begin to bake a data analytics culture into their own DNA. IBM is the global gorilla in the analytics world - its success is important not only to its shareholders, but to all analytics companies. I have no particular connection to the Company but believe that if IBM does not succeed then analytics may remain a technology niche that does not realize its potential and the entire industry will suffer.

Intuitively, the Company's move to exit lower margin and commoditized hardware businesses and to reinvest in higher margin IP-centric businesses makes sense. However, the Company has been underperforming the broader market for several years and has now fallen below $140.

IBM has been there before. In the late 1980's and early 90's the mainframe business was dying and Microsoft was ascendant - the Company did not appear to have a clear strategy and its future was bleak. Lou Gerstner was appointed CEO in 1993 when the Company was at death's door and he not only saved the Company but resuscitated its leadership position by setting out some key priorities including its culture and customer focus as well as a disciplined focus on execution. He set out his experiences in his book "Who Says Elephants Can't Dance?" which crystalized and simplified his thoughts and actions in such a way that I, for one, came away thinking that pretty much anyone could have managed the turnaround. Of course, very few people could have achieved what he was able to, and his book remains one of the best business books I have read.

However, while I digress, this anecdote does underscore that this article is as much about business strategy, culture, leadership and execution as it is about predictive analytics. At the end of the day, the business of analytics is about exactly those things. The business strategy is right - the open questions revolve around culture, leadership, execution - and timing.

IBM's stated strategy is to lead a rapidly reordering information technology industry. This led to its decision to shed business units that were becoming commoditized and were on a downward trajectory. In their place they identified certain key growth areas where investments would be focused. These areas became the key strategic imperatives:

- Transforming industries and professions with data (analytics)

- Remaking enterprise IT for the era of the cloud (cloud)

- Reimagining work through mobile and social technologies (mobile)

- Rethinking the challenge of security (security)

- Creating new infrastructure for a new era (social)

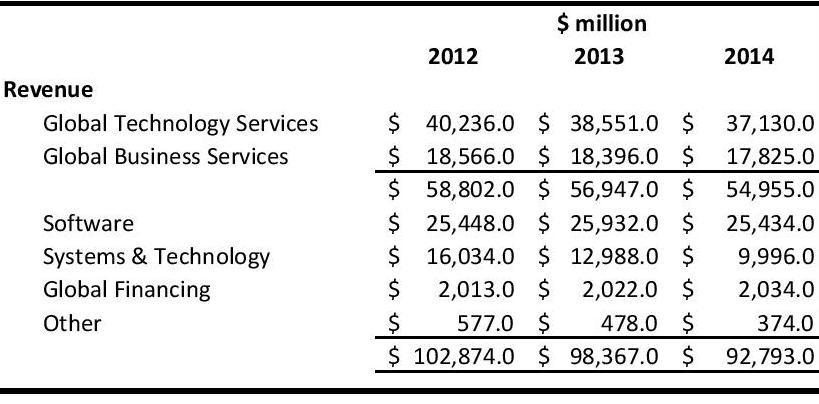

IBM is still a global technology leader, it operates in 175 countries, has 380,000 employees and revenue of $93 billion - changing the course of such a battleship is not easy. IBM's revenue by segment is as follows:

The cloud, analytics, mobile, social and security businesses generated $25 billion of revenue in 2014 and now represent 27% of total revenue, up from 13% in 2009. IDC estimated that the big data and analytics market would reach $125 billion in 2015 while the Company itself noted that this market is expected to grow to $187 billion. The cloud market was estimated to reach $250 billion by 2015. IBM is a big player in some very large markets. This blog focuses on the analytics initiative.

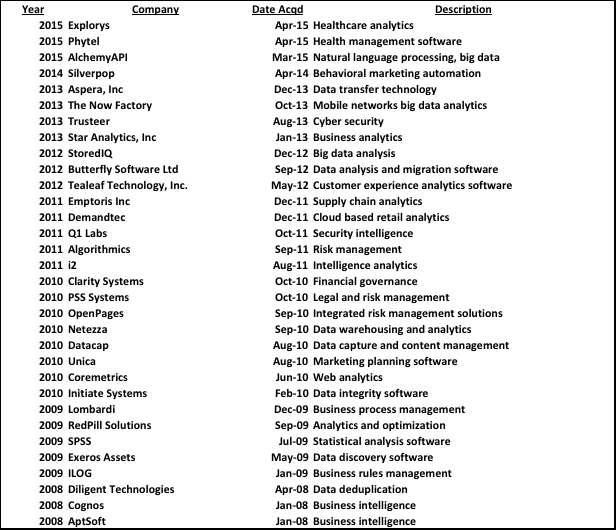

Clearly, transforming data into insight through analytics delivered through the cloud is a central tenet of the Company's strategy. To this end, the Company has invested over $26 billion to build its big data analytics capabilities, of which over $17 billion was spent on over 30 acquisitions. Further, it has invested over $8 billion to acquire 18 cloud related companies and spent $1 billion to expand its global data center footprint. This is not a trivial undertaking but the Company now boasts a portfolio of analytic assets that is second to none in the industry. Some of the more significant analytics acquisitions include:

I have outlined a structure for the analytics industry in a prior blog post (http://bit.ly/1HwXl4p). This structure categorizes analytics functions as either solutions or tools & applications. On the one hand, analytic solutions can be broadly divided into three categories:

- risk mitigation (credit risk, catastrophic events, fraud, compliance etc.)

- market opportunity (pricing, marketing, customer insight etc.)

- performance management (machine sensor analysis / IoT, sports etc.)

And, on the other hand, analytic tools & applications are comprised of the following categories:

- Data management (including Big Data and unstructured data)

- Business intelligence

- Data aggregation

- Analytic modeling

- Analytic consulting

- Decision management

IBM has capabilities and assets across the entire spectrum of these categories.

In fact, a number of the acquired companies are category leaders: Cognos is a leader in the BI space, ILOG is a leader in the decision management field, SPSS is a leading modeling company and so on. This has enabled the Company to build a comprehensive suite of analytic capabilities.

The objective is then to develop industry standard solutions (franchises) that are repeatable, and can drive scale and margins. IBM currently has solutions for a number of industries. Historically, these industries comprised data rich, high transaction volume and heavily regulated industries such as financial services, insurance, communications, retail etc. Today, every industry creates large amounts of data and IBM has responded by establishing industry solutions for such markets as education, media & entertainment, travel, aerospace, automotive, healthcare, life sciences and more. This puts them in a sound position to own the customer relationship as the market for analytics evolves. Further, the capabilities they have acquired or built can be redeployed across different application areas and business units - for example, I2's intelligence analytics are built on link analysis technology which is used in crime analysis but could also be purposed towards fraud and disease prediction.

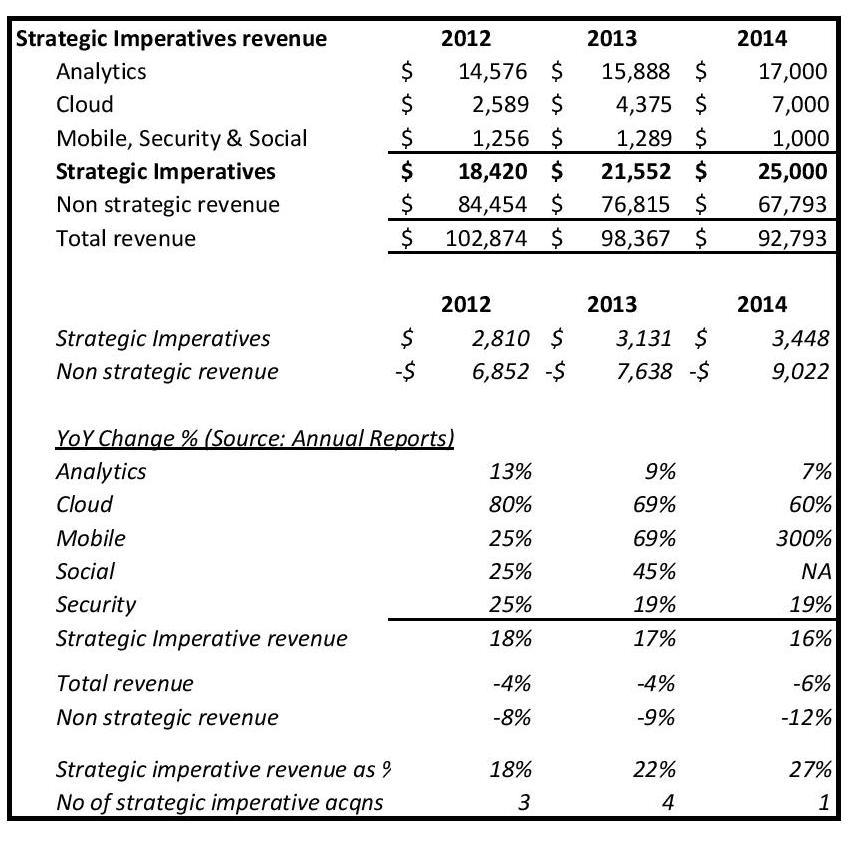

Given this, the Company appears to be doing all the right things to create a gorilla in the analytics space. Unfortunately, management does not make it easy to understand how its Strategic Imperatives are faring. It continues to report its segments along the lines noted in the table above; consequently, the Strategic Imperative revenue is buried within those legacy units. In an effort to better understand the composition of the strategic imperative revenue I constructed the table below based on extrapolating from information included in annual reports. Clearly, these numbers are approximate and include some inconsistencies - for example, the Company noted total Strategic Imperative revenue in 2014 was $25 billion of which Analytics totaled $17 billion and Cloud revenue was $7 billion meaning that Mobile, Security and Social contributed the balance of $1 billion. Backing into 2013 numbers results in Mobile, Social and Security revenue at a higher level in 2013 than 2014 which does not make sense. However, I have included the table as it does provide some directional guidance as to the the trends of the various business lines.

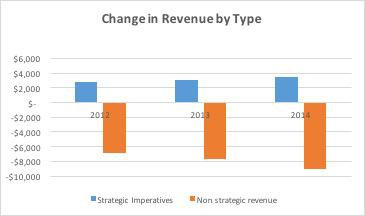

A couple of points emerge from this table. Firstly, and most obvious, revenue from non-strategic businesses is declining at a faster rate than revenue from Strategic Imperatives. As non-core asset disposals stop, this position should stabilize and revenue return to positive growth.

Secondly, Strategic Imperative revenue has a CAGR of 17% over the past 3 years and the Analytics business has a CAGR of 10%. This includes the impact of acquisitions - we cannot calculate the organic growth rate. We do know that the Company has made about 30 analytics acquisitions since 2008 at an aggregate cost of $17 billion. Of these, Cognos was acquired in 2008 at a cost of $5 billion and SPSS was bought in 2009 at a price of $1.2 billion. Therefore, we can assume that the Company has spent about $10 billion since 2011 to drive $4 billion in revenue growth. The Company expects its organic growth rate to settle back to the mid-single digits as the transformation is completed - this would translate to about a $1 billion annual increase in Analytics revenue going forward.

Can the Company achieve this sort of organic growth? The answer will most likely depend on Watson and, to a lesser extent, on the downstream synergy benefits of the Cloud business on the Analytics business as well as some fundamental assumptions about the penetration of analytics within organizations including the rise of the "citizen data scientist" and self-serve data discovery, and finally, internal execution matters.

Much has been written about Watson - IBM's cognitive computing initiative. There is considerable excitement about it's capabilities to discover and present data relationships, the $1 billion invested, growth in the customer base, robust partner ecosystem and application development activity and the potential for Watson to be a $10 billion business by 2023. The IBM Watson Group was formed in January 2014 and comprises both the more far reaching, natural language-based cognitive computing area as well as the Watson Analytics Group which is building an ecosystem of partners to build more traditional predictive analytics solutions leveraging tools such as SPSS and Cognos. It appears that the future of Watson is still ahead of it with the unit having generated total revenue of less than $100 million as of October 2014 (according to a Wall Street Journal article). So, there is much work to do. The Company is taking a very open and collaborative stance to the development of the business model and is actively working on revenue share opportunities with members of the Watson ecosystem. It clearly shows great promise in the healthcare and life sciences fields and the Company sees opportunity in cross-industry/synergistic analytic areas (the basis for the formation of a travel, retail and healthcare unit specific to Watson).For now, Watson is still in the early adopter phase - many industries are still coming to terms with basic descriptive analytic tools let alone considering more advanced initiatives. So, while it may currently be difficult to point to hard evidence of revenue momentum; if, in the year 2020, one were to provide the answer "This business analytics technology is finally changing the paradigm of knowledge creation." Watson would be able to ask the question "Who am I?"

Part of the ultimate success of Watson and of more mainstream (descriptive and predictive) analytics tools is the trend towards what Gartner is calling the "citizen data scientist" or self-serve analytics. In and of itself, the concept of business users, rather than highly qualified data scientists, taking over the reins of increasingly user-friendly analytic applications is compelling. However, to maximize the chance that such efforts will be successful, companies will need to embrace a focused approach:

- Data should be viewed as a corporate asset and be freely available to those in the organization who can best use it.

- Business users should have a curious mind but managers should provide some direction as to the nature of the business problems that it is trying to solve while allowing latitude to the person tasked with solving it.

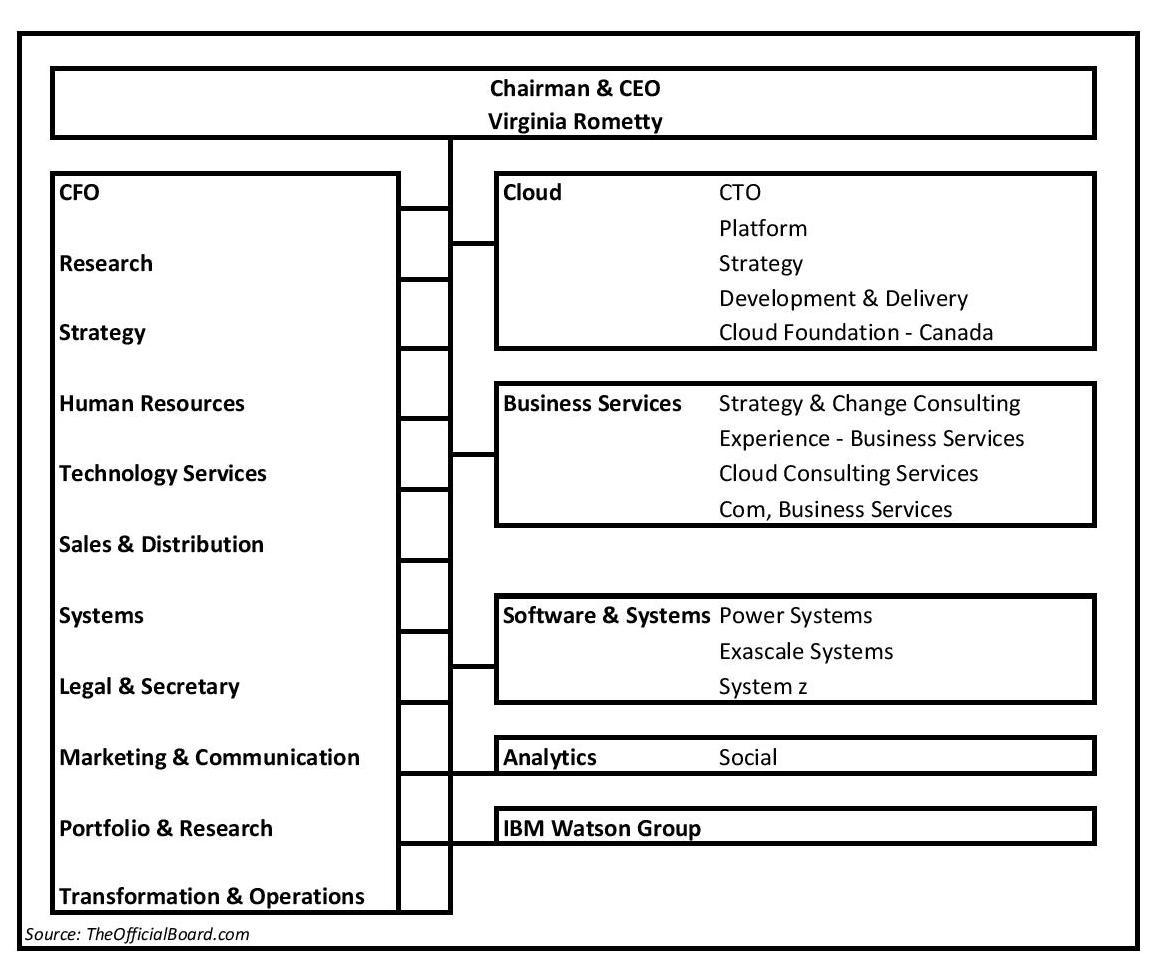

Of course, as with all things in business it comes down to execution. IBM is a very large and complex organization. The transformation of such a behemoth takes time. It is trying to lead its clients down a new path and some resistance is only natural. It is creating new solutions which is necessarily a high touch, services driven process but must then look to productize and scale those custom solutions to the broader market and generate higher margin annuity streams. I am not in a position to critique what IBM management is doing in this regard, but I do believe several points are worth making. The right management structure is critical to getting the most out of the assets. The Company's organization structure is as follows:

The organization chart looks to align with the financial reporting structure. It is reasonable to assume that the Company has all the right incentives in place to minimize organizational friction and maximize the potential to cross-sell etc. Managing the cultural integration of acquired companies is also important - especially in IP oriented businesses. Big company politics can be brutal! While some businesses can be easily absorbed, others will perform better with some degree of brand autonomy. The trend towards a remote workforce is cost effective but can come at the risk of missing the benefits of informal (water cooler) collaboration. As the Strategic Imperative business units mature they will naturally become less services oriented and more productized at which point it would be helpful for the Company to describe the financial performance in more detail.

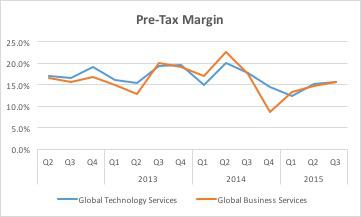

There is a lot of noise surrounding IBM's strategy - but what signals will emerge to indicate that the transformation is delivering results? Management can continue to quote all manner of statistics promoting some form of progress but until it is borne out in the numbers the market will remain skeptical. My sense is that the key leading indicator will be an improving trend in the Global Services Unit pre-tax margins. The targeted business model should be characterized by developing new custom analytic solutions and then productizing those solutions and creating industry standard "franchises" that can be rolled out to multiple clients. This will lead to IBM having more of a lower growth, higher margin business model. They are not there yet - quarterly net margins (based on external revenue) have trended as follows.

Margins have bounced back from the lows at the end of 2014 but the improving trend needs to continue and move back to the mid to high 20% range in order to validate the strategic plan. If the next several quarters continue the recent trend then the transformation may be considered successful and, just as important, the rest of the industry will benefit from the halo effect and the data analytics industry will enjoy a sustained period of strong growth and innovation and will be a core part of every company's management information toolkit.