This morning. U.S. equity futures are modestly lower. U.S. equity markets are in correction. This morning’s earthquake, about 80 miles off Japan’s northeastern coast, struck 10 minutes before the local close. At the time of the quake, Asian markets were trading about -60 bps lower. In the final minutes, equity markets lost approximately -1.0% more. One Japanese trading desk reports that at the height of the quake, its traders were buying building and construction stocks. European markets opened 2 hours after the quake; after an initial steep sell-off, equities rallied, sold off again, and are rallying again from intraday lows. Friday’s Saudi “day of rage” appears not to have found the planned traction. The SPX opens at 1295.11, down -3.28% below its February 18th high. March SPX futures are at 1287.70, down -1.81 points after fair value adjustment. Next SPX resistance is at 1309.15. Next support is at 1287.64.

Thursday’s equity markets closed lower, as a confluence of economic reports and macro-events sent the risk trade to the sidelines. A slowing of Chinese exports, while expected, was worse than anticipated. Middle East unrest in front of a planned “day of rage” in Saudi Arabia kept buyers on the sidelines. U.S. equity indexes opened lower, consolidated through the morning, lost ground on a report of Saudi police action, and ended near intraday lows, below 50-day moving averages, but above key support levels. Volumes rose. Market breadth was negative. The U.S. dollar was stronger. U.S. Treasury yields rose.

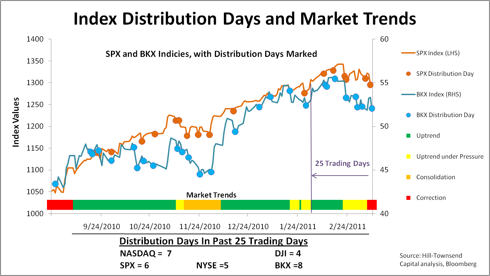

All major U.S. equity indexes were lower on greater volume. All recorded another distribution day, and all closed below their 50-day moving averages. Distribution days infer institutional selling by tracking declines of more than -0.25% on increased volume, in the past 25 trading days. U.S. equity markets are in correction. Market corrections typically end on an intraday reversal on increased volume, when confirmed in a subsequent trading.

World equity markets are lower. In Asia, the Nikkei and Hang Seng closed down -1.72% and -1.55%, respectively. The Shanghai composite fell -0.79%, on lower volume. On February 25th, the SHCOMP confirmed a new uptrend, and while it sustained a distribution day last week, there were none this week, despite the past two day’s lower trade. In Europe, equity indexes are lower, but rebounding from intraday lows. The Eurostoxx50, FTSE, and DAX are down -0.76%, -0.71%, and -1.02%, respectively. On the EuroStoxx, financials are the 3rd best performing market segment, down -0.46%.

LIBOR trends remain unremarkable. Overnight USD LIBOR is lower at 0.21550%, compared to 0.21600% the prior day and compares to 0.25188% at year-end. USD 3-month LIBOR is unchanged at 0.30950%, compared to 0.30281% at year-end. In early trading, the dollar is stronger against the euro and pound, and lower against the yen. The dollar has trended lower since last June and now trades well below its 50-, 100-, and 200-day moving averages. The euro trades at US$1.3768, compared to US$1.3798 Thursday and US$1.3909 the prior day. The euro trades above its 50-, 100-, and 200-day moving averages. The dollar trades at ¥82.27, compared to ¥82.98 Wednesday and ¥82.74 the prior day. Treasury yields are higher, with 2- and 10-year maturities yielding 0.641% and 3.382%, respectively, compared to 0.633% and 3.358% Wednesday. The yield curve spread narrowed to +2.741% compared to +2.725% the prior day. In the past year, the 2- and 10-year spread has varied from a low of +1.959% on August 26, 2010, and a high of +2.889% on February 3, 2011. Commodities prices are generally lower, with lower petroleum, but slightly higher natural gas, lower precious metals, but higher aluminum, lower copper and agricultural prices.

U.S. news and economic reporting. Economic reporting includes weekly jobless claims (initial claims registered 397,000 compared to survey of 376,000 and prior period claims of 371,000 while continuing claims registered 3,771 thousand compared to survey of 3,750 thousand and prior period claims of 3,791 thousand) and January’s trade balance (-$46.3 billion compared to survey of -$41.5 billion) at 8:30 and the monthly budget statement at 2:00.

Overseas news. Overnight, an 8.9 magnitude earth quake struck Japan, triggering significant tsunamis. In February, China’s consumer price index rose +4.8% over the prior year’s month, ahead of estimates. France became the first country to recognize Libya’s main opposition group. Today, press reports indicate Saudi Arabia is quiet in spite of calls for large scale “Day of Rage” protests.

Company news/research:

· BBT – raised to buy at Janney Montgomery, price target of $33.00

· XL – added to Top Picks list at FBR Capital

4Q2010 Earnings. The latest quarterly earnings results have exceeded EPS and revenue expectations. Of the 475 S&P500 companies that reported earnings to date, 71% (337 of the 475) beat operating EPS estimates, versus the historical average of 62%. Companies beat by an average of +5.3% (versus a historical average of +2%). EPS is up +37.1% over the prior year. Though challenged in the current operating environment, 366 companies (77%) reported increased revenues and 312 companies (66%) beat revenue estimates. In the fourth quarter of 2010, the SPX earned $22.47 per share, a +4.9% and +28.3% increase over 3Q10 and 4Q09 EPS of $21.42 and $17.51, respectively.

With all 24 BKX members reporting, 75% (18 out of 24) beat operating EPS estimates. Bank revenues disappointed slightly, missing estimates by -0.59% on average. Fifteen banks (63%) reported increased revenues over the prior year’s quarter and 17 banks (71%) beat revenue estimates. In the fourth quarter of 2010, the BKX earned $0.93 per share, a +31.0% increase over 3Q10 EPS of $0.71, and compared to 4Q09 EPS of -$0.52.

Thursday’s equity markets. On increased volume, the major indexes fell sharply at the open, with the SPX trading though support at 1305 to test 1295 just after 10:00. After a period of consolidation, markets sold off again after 1:30, on a report that Saudi police had fired into a crowd of protesters. The DJI, Nasdaq, NYSE composite, and SPX ended the day near their lows, off -1.82%, -1.84%, -2.14%, and -1.89%, respectively. Traders attributed the sell-off to reports that China’s export growth slowed and Moody’s cut in Spain’s credit rating. Combined with Middle East concerns regarding threats to petroleum shipments, the investor conversation has seemingly returned to threats to the economic expansion and away from improving fundamentals and earnings. Trading desks reported mixed experiences, with some saying they had buyers on dips, others that they were better sellers, but with long sellers primarily. With a dearth of corporate news here in the U.S., investors have focused more on the “macro” landscape and headline risk. Notably, the VIX failed to break through the 22 level and ended the day at 21.88, up +8.21%.

Technical indicators have worsened. The SPX broke through 1305, which had been support during the last dip on February 24th, but held key support at 1294 before closing at 1295.11. The next SPX support levels are 1286-1289. All of the major indexes closed below their 20- and 50-day moving averages, but above their 200-week and 100-, and 200-day moving averages. The Bloomberg 52-week new net highs was 134.00, up from Wednesday’s reading of +121, but below its 10-,20-,50- and 100-day moving average. The relative strength indicator fell to 43.03 from Wednesday’s 54.58, near the lower end of a neutral range.

The most recent AAII bullish sentiment index fell again to 35.98 (March 10th), down from its 36.8 on March 3rd, and well off most January and early February readings. Sentiment indexes are highly variable and often best regarded from a contrarian perspective.

All market segments closed lower. Oil and gas, basic materials, and financials led the way down, off -3.59%, -2.40%, and -2.07% respectively. Telecommunications, consumer services and consumer goods were off the least.

Financials were sharply lower, with regional banks RF, BK, and KEY leading to the downside, off -5.05%, -4.36%, and -4.05%. Every name in the BKX was down. In the KRX and XLF, all were down save one name in each index, TCB in the KRX, and VTR in the XLF. The BKX, XLF, and KRX closed off -2.36%, -2.01%, and -2.51%, respectively. All the indexes closed below their 20- and 50-day moving averages. All closed above their 100- and 200-day moving averages. While the broader indices have recovered their post-September 2008 losses, bank stocks have not, with the BKX closing -10.2% below its April 2010 high and -36.9% below its best level of 82.55 in September 2008.

NYSE Indicators. Volume rose +28.6% to 1.120 billion shares, from 871.20 million shares Wednesday, 1.10x the 50-day moving average. Market breadth was extremely negative. Up volume lagged down volume by a large margin. Advancing stocks lagged decliners by -2118 (compared to -123 Wednesday), or 0.17:1. Up volume lagged down volume by 0.08:1.

Valuation. The SPX trades at 13.4x estimated 2011 earnings ($96.68) and 11.8x estimated 2012 earnings ($109.70), compared to 13.7x and 12.0x respective 2011-12 earnings yesterday. The 10-year average median Price/Earnings multiple is 20.0x. Since the beginning of 2010, analysts increased 2011 and 2012 earnings estimates by +4.5%, and +5.4%, respectively. Analysts expect 2011 and 2012 earnings to exceed 2010 earnings ($84.78) by +14.0% and +29.4%, respectively.

Large-cap banks trade at a median 1.54x tangible book value and 12.9x 2011 consensus earnings, compared to 1.61x tangible book value and 13.2x 2011 earnings yesterday. These compare to the 10-year average median multiples of 3.08x tangible book value and 15.9x earnings. Analysts expect 2011 and 2012 BKX earnings to exceed 2010 operating earnings by +27.3% and 70.6%, respectively.

SPX. On higher volume, the SPX fell -24.89 points, or -1.89%, to 1295.11. Volume rose +30.5% to 895.18 million shares, up from 685.78 million shares Wednesday and above the 796.56 million share 50-day moving average. For the 98th consecutive day, its 50-day moving average closed above its 200-day moving average (1300.86 versus 1178.08, respectively). The SPX closed above its 200-week moving average (1177.60).

The SPX gapped lower at the open to 1305, crossing first resistance immediately. China’s surprise February trade deficit renewed global economic weakness fears, driving markets lower and moving U.S. markets into correction. The SPX crossed the 1300 threshold at 9:35 and fluctuated around this level through 11:00. Equities appeared to gain some strength after 11:00, crossing back above 1300 and using that level for support to move higher. The SPX reached 1305 at 1:15 when reports that Saudi Arabian police fired on protesters sank the market back below 1300 and to an intra-day low of 1294.21 at 1:40. The SPX bounced off of 1295 and made an attempt to retake 1300 at 2:45. Stocks sold off at 3:00, the index returned below 1300, and the SPX ended near the day’s lows. The index closed -0.44% below its 50-day moving average, closing below that average for the first time since September 1st, 2010. The SPX closed +9.93% above its 200-day moving average. The SPX closed below its 20-day moving average (1321.06) for the third straight day. The 20-day average decreased.

Technical indicators have turned negative. The SPX closed below 1300 for the first time since January 31st. The index closed above its April 2010 highs for the 68th straight session. The directional momentum indicator is negative, and the trend is stable. Relative strength fell to 43.46 from 52.97, a neutral range. Next resistance is at 1309.15; next support is at 1287.64.

BKX. On higher volume, the KBW bank index closed at 52.05, down -1.26 points, or -2.36%. Volume rose +38.41% to 130.12 million shares, up from 94.02 million shares Wednesday but below the 139.52 million share 50-day average. The index closed +21.10% above its August 30 closing low of 42.98, the trough of the recent prior correction, but -10.18% below its April 23rd closing high.

Financials underperformed the market, and regionals underperformed large-cap banks. The BKX gapped lower at the open, losing -1.70% at the bell. The index crossed 52.40 at 9:35 and fluctuated between that level and 52.20 until the 1:15 sell-off in the broader markets pushed the index to its intra-day low of 52.00 at 1:40. The index bounced off of 52.00 and rebounded to 52.40 by 2:40. The rally was sold and the index fell into the close, finishing just above its intra-day low.

Technical indicators turned negative. The index closed above 50 for the 56th straight day. The BKX closed above its 100- and 200-day moving averages (50.64, and 49.01, respectively), closing above the 200-day average for the 63rd straight session. The index closed below its 20- and 50-day moving averages of 53.70 and 53.59, closing below them for the 12th and 8th straight days, respectively. The 20- and 50-day moving averages fell. The 50-day moving average closed (by +4.58 points) above the 200-day moving average for the 39th straight session, but the divergence contracted. The 100-day moving average closed (by +1.63 points) above the 200-day moving average for the 22nd straight session, with the positive divergence still expanding. The directional movement indicator switched to negative, and the trend is declining. Relative strength fell to 42.20 from 49.52, a neutral range. Next resistance is 52.90; next support at 51.60.

Disclosure: I am long

BBT,

XL.