A recent CNBC story asked whether investors, looking for safety, should park money in the defense industry.

The writer argues the recent Russian incursion into Ukraine, along with conflicts in other hotspots, will help push defense stocks higher.

Is the writer correct? Is there a viable play in defense stocks, given current valuations?

In short, the answer is a resounding no.

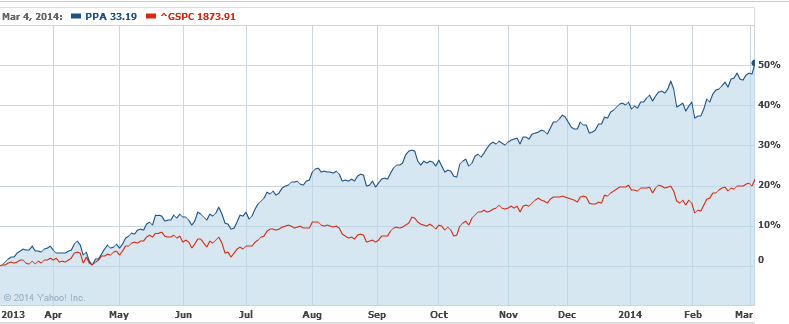

A cursory look at the spread between the S&P 500 and the PowerShares Aerospace & Defense Industry ETF (PPA) over the past 12 months shows how far ahead of the market defense stocks have risen.

Defense Stocks in the Near-Term

No matter which pricing metric an investor uses to determine fair value, defense stocks are significantly over-priced, and offer neither short nor long-term potential for value and dividend investors.

Need evidence?

In the chart below, we have included information on seven large cap defense stocks. As you will see, their prices are lofty by most value metrics.

Take Lockheed Martin, for example. Lockheed is priced at a fairly rational P/E of 18.33. A closer look, however, shows Lockheed with a CAPE (Cyclically Adjusted Price Earnings) ratio of 24.22 and a price to book value of 10.74 - a premium of 777 basis points to the industry average of 2.97!

Additionally, Lockheed's P/CF ratio of 13.51 is 12.7% higher than the industry average of 11.98. By most measures, Lockheed is too expensive at these levels - even with its better than average yield of 3.21%.

Boeing is in worse shape. It trades at 21.83x earnings and sports a CAPE ratio of 33.74 and a P/CF of 15.06 - both well above acceptable valuation standards. While the yield is 37bps higher than the S&P 500 average of 1.87%, the 2.24% yield is hardly worth the risk of buying the stock at such high-flying prices.

| Company | Yield | P/E ttm | CAPE | P/B | P/CF |

| Boeing (BA) | 2.24% | 21.83 | 33.74 | 6.54 | 15.06 |

| General Dynamics (GD) | 1.99% | 16.03 | 22.54 | 2.75 | 12.68 |

| Northrup Grumman (NOC) | 1.96% | 14.88 | 26.48 | 2.55 | 11.4 |

| Raytheon (RTN) | 2.19% | 16.85 | 25.62 | 2.87 | 13.4 |

| Huntington Ingalls (HII) | 0.77% | 24.02 | 30.69 | 5.53 | 21.6 |

| Lockheed Martin (LMT) | 3.21% | 18.33 | 24.22 | 10.74 | 13.51 |

| United Technologies (UTX) | 2.01% | 18.93 | 26.1 | 3.38 | 13.33 |

Data by Reuters

Prospects for the Long Term

It's not just the short-term that poses significant risks to defense stocks. Long-term, these stocks face serious headwinds.

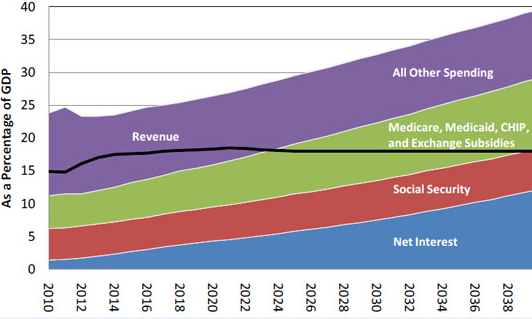

The CBO chart below illustrates this problem.

By 2024, the three largest budget items, Social Security, Healthcare, and debt service, will consume 100% of federal tax revenues.

And if we assume spending stays on its current trajectory, total federal spending will consume approximately 29% of GDP by 2024 - or roughly $5.8 trillion - a 38% increase over 2014 numbers!

Of course, this level of spending is completely unsustainable. And while fatuous politicians will do everything they can to recklessly spend - in the end, they will fail.

Using CBO numbers, defense spending will decrease to approximately 2.7% of GDP by 2024 - or approximately $540 billion in constant dollars.

This means that defense firms face a dwindling revenue source that will push their stocks deeper than an underground nuclear test site.

Protect your portfolio by avoiding these radioactive stocks.