Traditionally when one thinks of tobacco stocks one thinks of high yield and slow growth. The decline of smoking in the US seems to limit the future growth of the industry. Yet, I have discovered in Lorillard, a company with a bright future and one of the shareholder friendliest managements I have ever seen.

Background

Lorillard (LO) was founded in 1760 and is the third largest tobacco company behind Altria (MO) and Reynolds American (RAI). Its most popular brands are Newport, Kent, True, Maverick and Old Gold. It recently broke into the electronic cigarette space with its $135 million 2012 acquisition of blu. In October of 2013 it acquired SKYCIG an UK electronic cigarette company.

Thanks to Newport, Lorillard has recorded 11 straight years of market share gain. It now owns 14.9% of the cigarette market in the US. On the electronic cigarette front it holds 47% of market share.

- 2013 sales increased 5%.

- 2013 earnings were up 11%, the best in the industry.

- Tobacco market share rose 50 basis points to 14.9%.

- Electronic cigarette market share is an industry leading 47%.

- 4th quarter cigarette volumes declined by 1%.

- This compares favorably to industry wide 6.2%.

- Management is guiding for annual 3-4% declines in cigarette volumes.

- Electronic cigarette sales account for about 1% of this decline.

- Electronic cigarette division net sales up 300% to $230 million.

- Management has decided to merge SKYCIG into blu and expand blu into European markets that SKYCIG services.

- Management's eventual goal is to turn blu into a dominant global brand.

Risks

Continued decline in US smoking rates:

Regulatory risk against Menthol: On November 22, 2013 the FDA closed a public inquiry on a proposition for it to regulate or even ban menthol cigarettes. 90% of Lorillard's sales are from menthol cigarettes and though it is attempting to diversify its product line, any regulations targeting menthol cigarettes could have a devastating affect on sales.

Regulatory risk against electronic cigarettes: The FDA is deciding whether or not to regulate or even ban electronic cigarettes. Like the issue with Menthol, the FDA is concerned about any manner of nicotine delivery that is more appealing than regular flavored tobacco. The concern is that electronic cigarettes, with their lack of carcinogenic chemicals, bad smell and lower cost, may act as a gateway drug to individuals who wouldn't consider using regular tobacco. Once a non smoker tries and likes electronic cigarettes they might be willing to switch to regular tobacco, with all of the negative health implications.

Potential For Future Growth

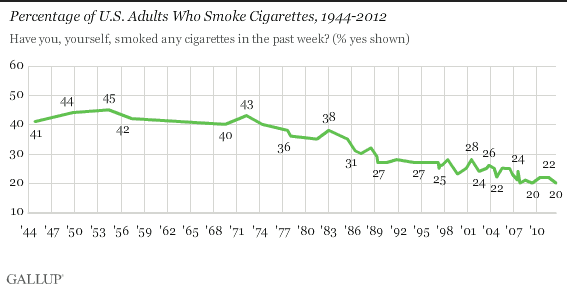

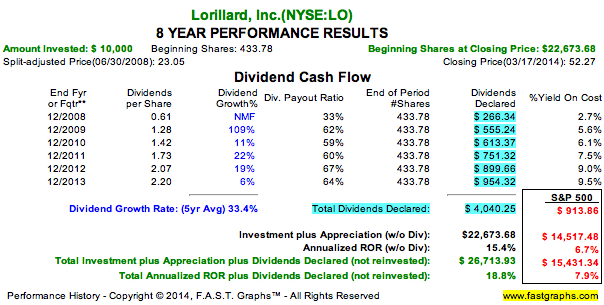

Larger market share of a larger (but shrinking) pie: The US smoking rate has recently hit a new low of 18.1%. By 2050 the US Census Bureau estimates the US population will increase by 100 million. If the US smoking rate stabilizes at some point, say 15%, that would represent a 17% decline. However, a 30% increase in population would actually increase the number of smokers in America. In addition, if Lorillard is able to continue to increase its market share than its sales of traditional tobacco would increase moderately over the coming decades. The growth wouldn't be fast, but it would continue providing the company with the consistent cash flow with which it has could finance stock buybacks and dividends. The company has an excellent track record of returning cash to shareholders. Over the last 5 years Lorillard has returned $8.224 billion to investors through these two methods.

Electronic Cigarettes: Regular tobacco is a $500 billion global business. Currently electronic cigarettes represent only $1.5 billion in sales but by 2023 Bloomberg Finance projects electronic cigarettes may overtake regular tobacco sales. That would mean electronic cigarettes could grow into a $250+ billion industry within a decade. Given that Lorillard owns 47% of this promising market the potential for profit growth is staggering.

Share Buybacks:

Over the last 5 years Lorillard has bought back $4.6 billion in stock. Over the last 6 years its decreased its share count by an astounding 29.8%. This represents a 5.73% CAGR decrease in the share count. Such aggressive share repurchases are helping drive Lorillard's impressive EPS growth rates.

If the regulatory risks prove overblown than Lorillard may end up being one of the greatest investments of the next 10-20 years. This is because the potential for electronic cigarette growth, combined with the company's passion for buying back shares, could result in EPS growth of 20+%.

Consider this: Lorillard's 2013 sales were $7 billion. If Bloomberg is even 10% accurate the electronic cigarette market would grow to $25 billion within a decade. Lorillard has 47% market share, which would represent revenue growth of $12.5 billion, tripling current sales. The growth in revenue would allow an acceleration of the stock buyback and the dividend growth rate, both of which have been superb. Though this potential hyper growth is a more speculative best case scenario, it shows that boring old Lorillard may have an amazing future ahead of it.

Future Projections and Current Valuation

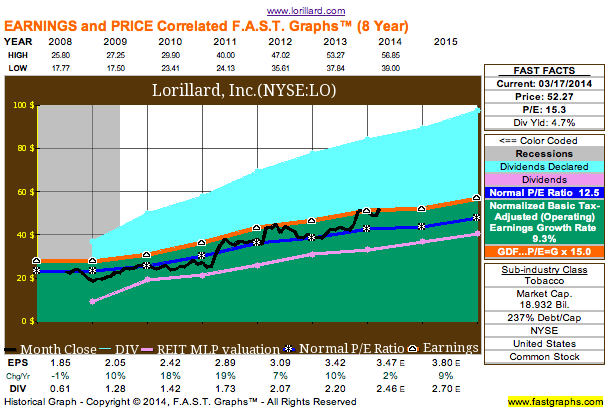

As seen in this fast graph, the average PE for Lorillard over the last 8 years is 12.5. Thus the current PE of 15.3 seems to indicate that the price is overvalued. This may be true based on a trailing earnings basis, but on a 10 year projected growth basis the opposite is true.

As seen here, the 10 year projected return of Lorillard is 10.9% CAGR. This does not include dividend reinvestment. If we compare this rate to the stock market's 1871-2013 9% CAGR total return, we see that Lorillard is likely to outperform the general market by about 21% over the next decade. Thus I determine that Lorillard is 21% undervalued at its current price. Investors can probably expect to beat the stock market over the next decade but is it enough to be compensated for the risk of owning the stock?

Risk Adjusted Cost Of Equity Calculation

This calculation tells us how much a stock must return for investors to be compensated for investing in the stock vs a risk free return, aka ten year treasury bonds. The formula for this calculation is:

risk free return+beta(market return-risk free return)

- 10 Year Treasury Bond: 2.76%

- Lorillard Beta: .33 (this means that Lorillard is only ⅓ as volatile as the stock market over the long-term)

- Market return: 9%

The cost of equity is just 4.82%. This low hurdle rate is due to Lorillard's incredibly low beta. Historically, lower beta investments have outpeformed the market. This calculation helps us to see why.

4.82% is the rate of return Lorillard would have to deliver to be worth the risk of investing. As we can see from the fast graph 10 year projections, the expected rate of return is projected to be over twice this. Thus Lorillard is a terrific investment at today's prices on a risk adjusted 10 year basis.

Dividend Analysis

Recently the dividend was raised 12% to $2.46/year. Note that the 2008 dividend is only for 2 quarters so it must be annualized to $1.22 to get a true comparison. We can see that in the last 7 years the dividend has grown 10.54% CAGR.

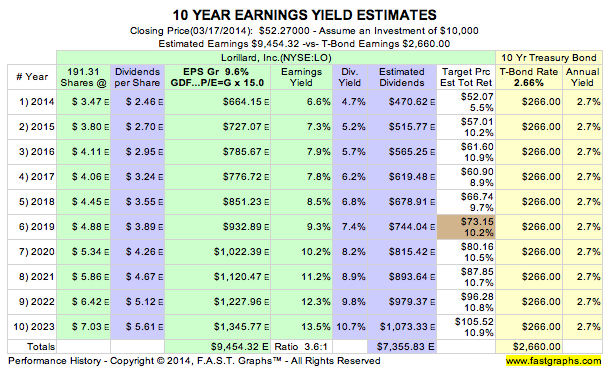

Looking ahead 10 years, using the earlier fast graph, we see a projected dividend of $5.61 in 2023. This represents an expected dividend growth rate of 9.59% CAGR.

DGI Score

A good rule of thumb is that total return equal: Yield+dividend growth rate. Keeping this number at 12+ is a great way to maximize the chances of outperforming the market in the long term.

If we look at Lorillard we see 5.1% yield+9.59% expected CAGR dividend growth for a total DGI (dividend growth investor) score of 14.69. This indicates that Lorillard is an excellent dividend growth stock.

Bottom Line

When it comes to great dividend growth stocks Lorillard is a prime example. It possesses a stable, repeat business and has a dominant position in the fast growing electronic cigarette industry. Its shareholder friendly buybacks and fast dividend growth make this stock a likely long-term market beater. At the current valuation the stock is massively undervalued in terms of its likely 10 year future performance.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.