John Petersen

After writing about investment opportunities in the energy storage sector for a couple of years, today marks an important transition because I've accepted Nadsaq's invitation to include my blog in the

Community section of their website. I'm grateful for the chance to reach a broader audience and hope that my weekly musings can help new readers separate hype from opportunity and avoid the intellectual short-circuits that are all too common in the energy storage sector.

By way of introduction, I'm a working lawyer and accountant who has spent 30 years guiding emerging energy and technology development companies through the corporate finance process. I earned my stripes in the battery industry during a four-year stint as general counsel for

Axion Power International that included 20 months as its board chairman. I'm an inveterate early adopter of new technologies, but my investment perspective is tempered by the knowledge that even extraordinary companies can take decades to achieve their potential and the future beyond a five-year time horizon is inherently unknowable.

During the 20th Century rechargeable batteries became a ubiquitous and largely invisible necessity of modern life. Lead-acid batteries started cars, provided back-up power and ran forklifts, golf carts and the occasional electric car, while compact lithium-ion and NiMH batteries powered portable electronics. None of these batteries performed as well as we wanted them to, but the only time we gave them any thought was when they needed to be charged or replaced. Maybe that's why the adjective most commonly used to modify the noun battery is "damned." The bottom line is batteries are and have always been a grudge purchase; devices that satisfied basic needs but fell short of expectations.

Over the last decade a curious dynamic has emerged in the energy storage sector as environmentalists, futurists and other dreamers latched onto the seductive idea that batteries could do everything from eliminating gas tanks to making wind and solar power stable. The eco-evangelical fervor rapidly spread to the media and government, and what started out as wishful thinking quickly morphed into ill-conceived policy. Faced with unreasonable expectations, battery developers found themselves between a rock and a hard place. They could either tell the government and the markets "your goals are unattainable" and reject piles of money, or they could say "we may be able to attain those goals," trusting that the money would flow, asking for forgiveness would be easier than asking for permission and there might even be an unexpected miracle.

The problem with the plan is that today's emerging energy storage demands are orders of magnitude larger than the applications the batteries were designed for. These emerging applications invariably demand extreme levels of battery reliability and performance, and are unbelievably cost sensitive. In other words, the plan itself is a classic example of the triumph of hope over experience.

Notwithstanding the flaws in the plan, the dynamic is now driving a global effort to improve all types of batteries. It's a long, difficult road, however, because battery technology is fundamentally different from information and communications technology, advances typically take seven to ten years to move from the laboratory bench to the factory floor, and the Moore's law gains we saw in IT and communications are not possible in electrochemistry. The innuendo inspired motto of my high school class was "better living through chemistry." In truth, however, chemistry hasn't seen many world-changing developments since 1969.

If you spend any significant time reading media stories and analysts’ reports on energy storage, you'll get the feeling that lithium-ion batteries are an amazing new technology that's arrived just in time to save us from the tyranny of imported oil. The reality is lithium-ion batteries have been around for over 20 years, fine companies like Sony, Panasonic, Sanyo and NEC have already optimized their manufacturing processes, the chemistry accounts for over $7 billion in annual sales and the principal economies of scale have already been realized. From this point forward, the gains will be incremental at best until something truly different comes along.

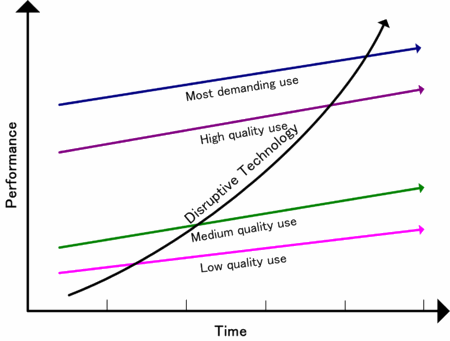

Most investors have heard of disruptive technologies, a term coined by Clayton Christensen to describe simple, low-cost innovations that eventually displace established technologies. According to Dr. Christensen, disruptive technologies usually lack refinement and have performance problems because they're new, appeal to a limited market, and may not even have a proven practical application; but their low cost creates new markets that induce technological and economic network effects and provide an incentive to enhance the disruptive technologies to equal or surpass established technologies. The following graph illustrates the phenomenon.

If you consider the graph for a minute, the problem with the disruptive technology myth becomes obvious. Lithium-ion batteries were developed for the most demanding applications and are already at the top of the graph. Moving down-market to low quality applications like electric cars and grid-based storage is the industrial equivalent of a salmon swimming upstream to spawn. It's a constant battle with the law of economic gravity, predatory competitors and customers and natural resource constraints. The lucky ones survive but many perish along the way. The key point to remember is that disruption flows from the bottom up, not from the top down.

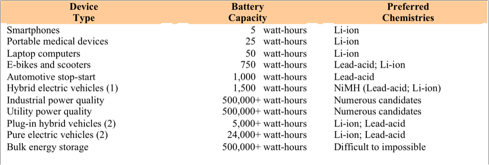

If we wanted to create a hierarchy of possible battery applications from the highest value per watt-hour to the lowest value per watt-hour, the list would look something like this:

(1) Current HEVs use NiMH batteries that are made from the rare earth metal Lanthanum. Since rare earth metal supplies are uncertain, lead-acid and lithium-ion battery developers are working to fill the void.

(2) In the US and Europe, plug-in vehicles will typically use lithium-ion batteries because they’re smaller and lighter. In Asia, more thrifty consumers are just as likely to prefer lead-acid. It is unclear whether either chemistry is truly suitable for the application.

I see a bright future for lithium-ion batteries in high value applications that only need a small amount of battery capacity, but think it's foolish to suggest that exotic batteries will become a cost effective technology for electric vehicles or play a critical in stationary applications where size and weight are meaningless but performance and cost are critical.

I consistently write about a short list of 18 pure play energy storage companies. My favorites in the established and profitable manufacturers class include Enersys (ENS), Exide Technologies (XIDE), Advanced Battery Technologies (ABAT) and China Ritar Power (CRTP). In the emerging technology class my favorites are Active Power (ACPW) and Axion Power (AXPW.OB). Unlike many writers, I don't expect leading lithium-ion battery developers like Valence Technology (VLNC), Ener1 (HEV) and A123 Systems (AONE) to thrive over the next couple of years.

In the weeks to come I'll drill down deeper into the myths and realities of the battery industry and the relative competitive positions of the manufacturers and developers I follow. Readers who would like to read my prior articles can find a complete archive at Seeking Alpha. Since I'm bullish on the battery business but bearish on many of today's market darlings, my articles tend to draw a lot of reader comment. I'd encourage investors who want to understand the industry to read my work, follow hyperlinks to source documents and pay attention to the numerous comments from others who disagree with me. If you make the effort, you'll find a depth and breadth of thought and opinion that I could never present if left to my own devices.

Disclosure: Author is a former director of Axion Power International (AXPW.OB) and holds a substantial long position in its common stock.