Today is the most important day in the life of the Model Portfolio. But first, a bit of history.

In the throws of the Brexit crisis (brief though it was), we took the opportunity to liquidate a number of very expensive positions in shares of consumer staples stocks, and put the proceeds into AMLP (an MLP ETF) and VGK, the Vanguard Group's total European stock index ETF. Since that day, VGK has rallied explosively, and is up by nearly 13% since the time we bought it just a couple of months ago. Since we put a large amount into that position, as you'll recall, the gains have been spectacular. Dumb luck, to be honest, but it's what we do with that luck that counts.

I never actually planned to keep that investment in VGK for long. It was designed as a place holder, a broad and cheap fund where I could park capital until I had some better idea with what to do with the money. The Model Portfolio is not designed to be an index fund, but an actively managed, hand selected batch of around 20 different securities. I look for well managed businesses with decades of healthy profits and proven business models. I look for steady and growing dividend payments. I look for competitive advantages that seem enduring. I look for reasonable debt levels. And above all, I look to buy businesses with those characteristics when they are cheap, and sell them when they get expensive. An index fund is actually the exact OPPOSITE of what the Model Portfolio is all about, and I am going to explain that more in just a couple of paragraphs. For now, please read on.

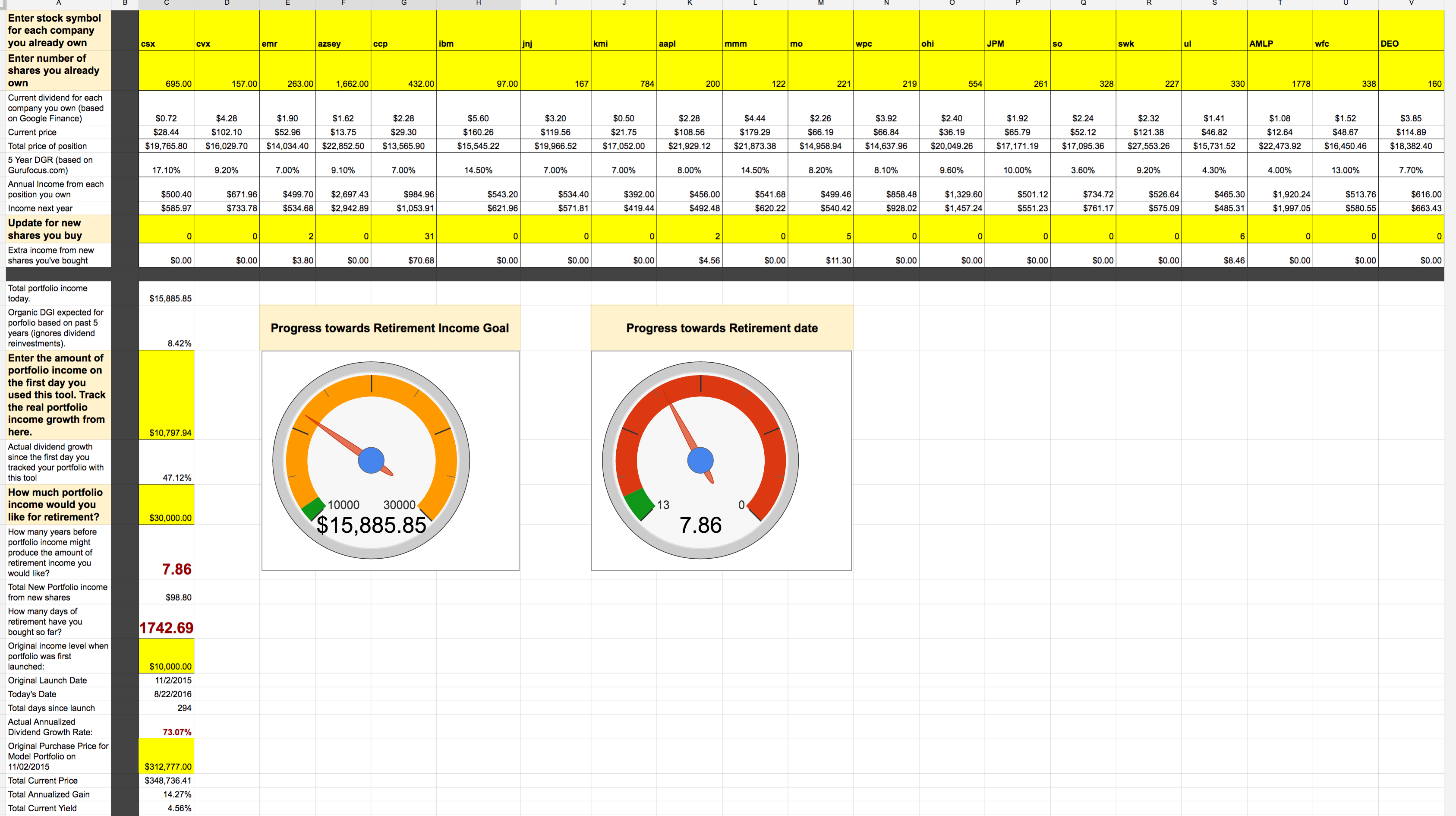

For those who follow the Model Portfolio, you already know that the purpose of the exercise is to create a portfolio that will churn out a steady and growing stream of income from reliable, top-shelf businesses. I started the Model Portfolio last November, with an allocation of shares designed to produce about $10,000 of dividend income a year. Since launching the project, my primary goal is always to maintain a portfolio of high quality businesses that trade at reasonable prices, and my secondary goal is to "trade up" when opportunity strikes, swapping expensive stocks with lower yields for cheaper stocks in equally good businesses that offer higher earnings per share (and, if available, higher dividend yields with lower dividend payout ratios). I set out to grow the Model Portfolio income from $10,000 a year to $30,000 a year, and have used my "retirement clock" spreadsheet to track the income progress, the income growth progress, and to project the probable number of years it will take before the Model Portfolio finally achieves it's $30,000 a year of dividend income.

And at long last, I have identified two strong European companies to replace VGK, and in the process, to deliver a very healthy raise. The first is Diagio PLC (ticker DEO) is a British company that produces beer, wine and spirits. I bought 160 shares of DEO. The company trades at a very reasonable PE ratio. The second is Allianz SE (ticker AZSEY) is an insurer based out of Germany, but with operations across Europe and the world. The company trades at a PE ratio of only 8, and offers a dividend yield of 6%. I bought 1,662 shares of AZSEY. Selling VGK and replacing it with DEO and AZSEY will lift the overall annual expected income of the Model Portfolio to $15,885 per year. This represents a gain of $5,886 per year of income above and beyond the $10,000 of annual dividend income expected when I launched the portfolio last November. The dividend growth of the portfolio comes out to an annualized 73% a year at this rate.

Now, why is today the most important day in the life of the Model Portfolio? The answer is because the dividend growth of the Model Portfolio is roughly 1000% higher than the average earnings growth rate for the S&P500 (which for the past century has stood at 7% per year on average). 1000% in under a year is a big, round number. Big enough that it doesn't look like statistical noise. Here is why I am telling you this.

The Nobel Prize for economics was shared by one of my favorite authors and thinkers, the father of modern portfolio theory, Eugene Fama. Professor Fama has "proven" that the stock market is perfectly efficient and rational, and therefore, it is not possible for a person to reliably outperform the stock market through security selection. Most people who try to grow the price of their portfolio faster than the stock market's price increase will end up dramatically underperforming the broader stock market. In fact, ALMOST EVERYONE who tries fails, and for this reason, the efficient market theory is more or less the gospel of the financial world.

I'm here to tell you today that everyone missed the boat. The fact that nobody can reliably outguess the market when it comes to stock prices says NOTHING about whether the market is efficient or rational when it comes to valuing corporate EARNINGS. It only proves that stock prices are unpredictable, but stock prices and corporate earnings are not necessarily the same things at all.

If you look at corporate earnings, you will quickly see that the stock market places vastly different prices on the earnings of one company (say, 8 times earnings in the case of Allianz) than on the earnings of a similar company (for example, 20 times earnings in the case of Chubb). Does that really make very much sense in a world where the stock market is perfectly efficient and rational? If so, then it shouldn't make a difference to a portfolio's earnings to swap shares of Chubb for Allianz. In the end, the portfolio's earnings ought to end up growing more or less in line with the overall market (which should come out to around 7% a year on average, assuming the portfolio is appropriately diversified).

On the other hand, if the only reason why Chubb's earnings are priced more richly than the earnings of Allianze is because the stock market is inefficient and irrational at valuign corporate earnings, then it should be possible to grow a portfolio's share of corporate earnings far faster than the rate of corporate earnings growth for the overall stock market, simply by selling "expensive" earnings and replacing them with "cheap" earnings. And all things being equal, the more irrational and inefficient the market is when it comes to pricing earnings, the faster the portfolio's earnings growth ought to be relative to the earnings growth of the overall market.

And that is precisely what I've done with the Model Portfolio (and for the last 20 years, with my own portfolio as well). I've seen many examples of "expensive" earnings and "cheap" earnings over the past months, and used those opportunities to buy and sell stocks and grow the Model Portfolio's income by over 10 times the average earnings growth rate for the S&P500. If the market was rational and efficient, I couldn't have done it with the Model Portfolio over the last year, or my own portfolio over the last twenty years. If Eugene Fama is correct, then technically speaking, I cannot exist. And I do very much beg to differ, as far as THAT is concerned.

So let's sum it up. As an investor, my approach is to say "I don't know or care what the stock market will do in the future." The only thing I focus on is growing my share of corporate earnings, not growing the composite price of my portfolio (in the real world, I literally have no idea what the price of my portfolio is on any given day or even any given year). I use the actual dividends I get in my hand each year as the basis for how I calculate my portfolio earnings, because corporate income statements can be very misleading, whereas cash money is unambiguous and hard to argue with. If I see a way to buy a stream of high quality earnings at a good price, I buy it, and if the stock stays cheap for a day, a year, a decade, I don't care. I am happy to buy MORE shares that will entitle me to a greater percentage of the company's high quality earnings. And if those shares become expensive, then I'll sell them so long as I can find a cheaper alternative place to park my capital. And the more wacky and insane the stock market is when it comes to pricing corporate earnings, the faster I am going to grow my share of corporate earnings. I'm focused squarely on what the efficient market theorist types ignore (earnings) and almost entirely ignore what the efficient market theorists focus on (stock prices).

The composition of the Model Portfolio is now thus:

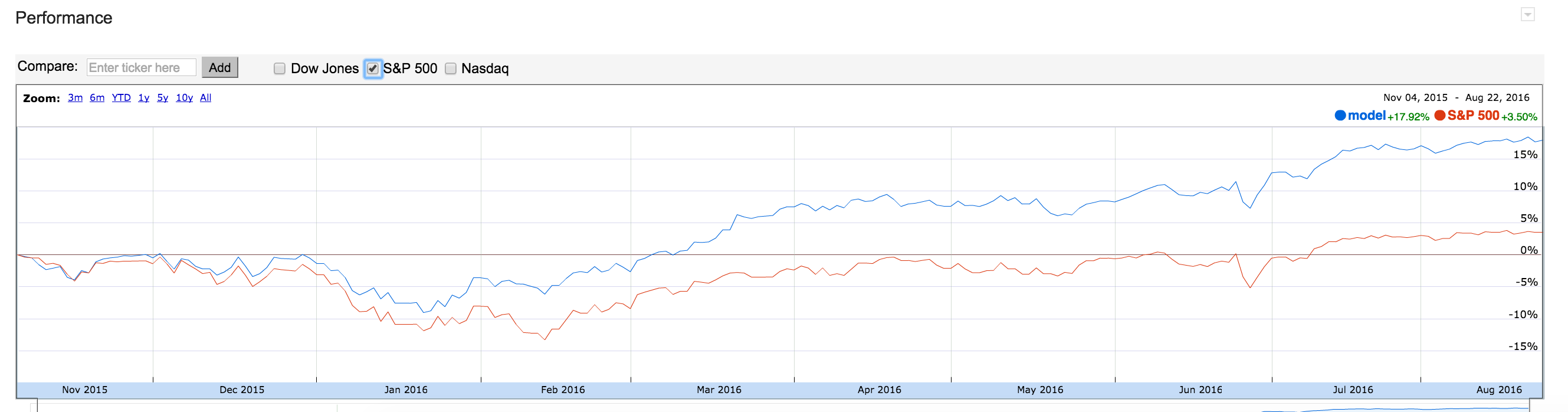

I've just gotten through lambasting price performance as an entirely meaningless goal, but I realize that we have total return investors out there. Some would say dividend growth is not an appropriate metric to measure portfolio growth, but I will tell you that over time, there's a chance that the price growth of a portfolio might fall somewhat roughly into line with the underlying earnings growth of the portfolio. I have no clue about what those chances are, by the way, or how long it would take for all that to shake out. Regardless, for those who care about such things, here is the relative performance of the Model Portfolio compared to the S&P500 since I launched the Model Portfolio project last November: