After Sonic Foundry's (OTCPK:SOFO) fiscal 2009 report last November, our post was "To Believe or Not to Believe (in the Mediasite Franchise)?" (link here). Readers probably know by now that our research provides ample evidence to believe in the franchise. We included more support for the franchise thesis earlier this week (here). Still, ultimately the financial results must confirm the presence and durability of a franchise.

We think fiscal 1Q 2010 results released Thursday are another step in the right direction and -- importantly -- forward guidance for a "tipping point" (as coined by author Malcolm Gladwell) this year remains intact. In fact, management said we'll begin to see "large deal impact" during the March quarter (fiscal 2Q 2010). This is ahead of prior guidance calling for large deals to hit late spring and summer (June/September quarters). We recommend watching the half hour presentation - link here.

We think fiscal 1Q 2010 results released Thursday are another step in the right direction and -- importantly -- forward guidance for a "tipping point" (as coined by author Malcolm Gladwell) this year remains intact. In fact, management said we'll begin to see "large deal impact" during the March quarter (fiscal 2Q 2010). This is ahead of prior guidance calling for large deals to hit late spring and summer (June/September quarters). We recommend watching the half hour presentation - link here.

An interesting sidebar (pointed out by someone on the Yahoo! Finance Message Board here) is to watch Sonic Foundry's earnings Webcast and compare the Mediasite delivery to that of video conferencing giant Polycom's recent earnings Webcast (PLCM) - link here. Polycom uses a pop-up window with video playback via user selected Windows Media or Real Player that has a slide window to the right. Yet, the slides didn't move for us. Instead, to share/show each new slide, a new browser window is launched each time (!!!), which -- to put frankly -- we find cumbersome and suboptimal. We suspect Polycom management would not only agree but likely prefer to use Mediasite to deliver their quarterly message (and other corporate events). Thus, as discussed in our "Get the Memo" post on 1/03/09, Polycom provides us with yet another example of an organization that needs Mediasite, albeit one sitting squarely in the video arena. Other video-related companies that could benefit include Thomson Reuters (TRI), Nasdaq OMX's (NDAQ) Shareholder.com unit, and even Cisco Systems (CSCO).

Back to results. For the quarter, revenue of $4.5 million (+12% Y/Y) was better than implied guidance for only $4.0 million and the company's GAAP net loss was only $320 thousand compared to $1.3 million (revised) in the year ago period.

Sonic's trailing twelve month income statement is as follows:

- Billings of $19.5 million were up 1% Y/Y (expect acceleration in coming quarters)

- Revenue of $19.1 was up 12% (catching up to TTM billings)

- Gross profit of $14.6 million was up 16% (margin expansion)

- GAAP operating expenses of $16.1 million were down 10% (expense reduction)

- Cash operating income of approximately negative $150 thousand (a $900 thousand Y/Y improvement)

A few slide highlights - new customers:

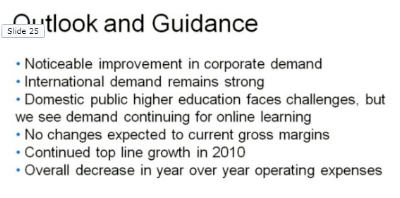

Guidance:

Guidance: More on the outlook and market position:

More on the outlook and market position: In Crossing the Chasm: Marketing and Selling Disruptive Products to Mainstream Customers by Geoffrey Moore (included in our reading list here), Mr. Moore shares his view of the technology adoption life cycle and strategies for making the jump -- i.e. "crossing the chasm" -- from "Early Adopters" to "Early Majority" and then to the "Late Majority". Mr. Moore's advisory firm, TCG Advisors, includes several related presentations on its Web site (link here).

In Crossing the Chasm: Marketing and Selling Disruptive Products to Mainstream Customers by Geoffrey Moore (included in our reading list here), Mr. Moore shares his view of the technology adoption life cycle and strategies for making the jump -- i.e. "crossing the chasm" -- from "Early Adopters" to "Early Majority" and then to the "Late Majority". Mr. Moore's advisory firm, TCG Advisors, includes several related presentations on its Web site (link here).In one deck, Dealing With Darwin - Innovation Vectors TCG Advisors Deck, he illustrates the life cycle with a "bowling alley" and "tornado" in the "Early Majority" phase as adoption accelerates on the way to "Main Street" adoption. Given Sonic Foundry's guidance and apparent confidence that the large deals are in process (i.e. a reality), we think Mediasite is currently making the leap to mainstream adoption. Of course, execution is critical during this stage and, along with IT budget pressures, represents a primary risk factor.

Let's briefly consider two scenarios:

- (1) The best case scenario for investors: earnings power finally becomes material in calendar 2010, although the Market (today) may not believe the future promise until micro-cap Sonic truly shows it the money (within next six months). At that point, interest in "the story" suddenly perks up and valuation expands along with investor/media interest. We've seen it before with other companies. If quarterly revenue can scale to the mid-$6 million range, we estimate quarterly earnings of around $0.25, or approximately one dollar annualized. At that level, even a conservative P/E multiple puts shares meaningfully higher.

- (2) The worst case scenario: large deals fail to materialize and the business trends flat and/or erodes and funding is a problem in a still fragile economy. The stock languishes and declines.

However, we find comfort through our extensive technology industry experience and Mediasite franchise analysis. Notably, we see and hear increasing, consistent, and favorable feedback from customers -- for the latest, please see the Big Bend Webinar this week:

Getting the Buy-In and Budget to Launch Hybrid Courses Right Now Russell Beard of Big Bend Community College shows you how one of the smallest community colleges in the state of Washington with one of the largest service districts – 4,000 students across 4,500 square miles – found the money, time and political will to launch a webcasting program.

While acknowledging risk factors, we can now feel even better with our November conclusion on the back of reiterated guidance -- given the company's expanding customer roster and forthcoming campus-wide adoptions, we continue to believe our initial thesis: competitive advantages point to a powerful, sustainable franchise -- Sonic Foundry is (1) far along the learning curve with (2) intellectual property protection, and (3) very satisfied, captive customers that face high switching and search costs. Points (1) – (3) are both related to and strengthened by (4) economies of scale and (5) leading market share.

Furthermore, our intrinsic value estimate of $20-27 is supported by an estimate of reproduction cost as well as the probable private market value that would be awarded by an informed strategic buyer based on trailing financial results (without the benefit of insights into Sonic's pipeline that might support a higher "PMV", 2009 M&A comps provide support).

We will follow-up in February with a bit more on how to interpret forward guidance.

Disclosure: Long SOFO.