Even if your interest in the Japanese economy is limited to sushi exports, video games and overpowered motorcycles, you would be well served to continue reading this entry, for the economic paralysis that Japan is presently enduring…and the extreme policy responses….is a case study for what may be awaiting other advanced economies, including the United States. It serves investors well to ignore the round…yet insignificant…numbers crossed by major indices and asset classes that the mainstream media sheepishly love to highlight. Recent meaningless examples include the Dow at 15,000, the S&P 500 at 1,600 and gold's 2011 assault on $2,000 per ounce, which has since petered out with a resounding thud. Yet last Friday's breach of 100 Japanese Yen (JPY) to the U.S. Dollar likely is significant for what it symbolizes about the state of advanced economies, their growth prospects, debt loads and the steps policy makers have attempted in order to right the ship.

Just in case there was any doubt that there is a beggar-thy-neighbor currency war occurring in the developed world, the USD has risen 27% against the JPY over the past year. In poker parlance, that would be akin to, "I'll see your QE3, Mr. Bernanke, and raise you the unlimited commitment to reflating the economy by the Bank of Japan (BOJ)." The odds-makers in financial markets have sided with the Japanese, betting that the Fed will eventually be forced to raise U.S. interest rates before the Bank of Japan takes its foot off the accelerator (for those not initiated into the cult of foreign exchange, expectations of interest rate differentials are a key driver in currency markets….hence the recent plunge in the value of the JPY). Ironically, much of Mr. Bernanke's fame came at the expense of the Japanese when during their lost decade….well decades now….he chastised them for not being aggressive enough in their policy responses. An accusation that clearly no longer applies.

Demographics As Destiny

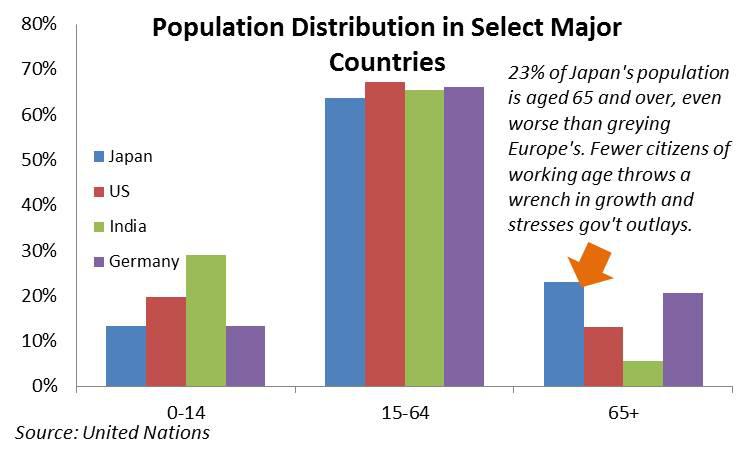

It hardly seems fathomable that Japan could have gone so wrong, so quickly. During the 1980s the country averaged over 4% annual GDP growth as it enjoyed the final stages of its post-war boom and accession to the top-tier of global manufacturers. Then things got frothy. Asset bubbles, a stock market crash, zombie banks. And on top of that, the lousiest demographics in the developed world. As seen in the chart below, 23% of Japan's population is age 65 and older. That means a smaller workforce will be responsible for covering the growing social outlays associated with a rapidly rising number of pensioners. Similar trends are occurring in other advanced economies (and in China, thanks to its one-child policy), but Japan takes the cake.

This confluence of forces kept economic growth stuck in low gear, averaging in the neighborhood of 1% annually over the ensuing decade-plus. By the mid-90's authorities instituted massive fiscal stimulus in hopes of spurring demand by undertaking large-scale projects. It did not work. Growth remained sluggish and only showed signs of life during the five years preceding the global financial crisis, a period in which global growth was largely built upon a house of cards. Since then Japanese GDP growth has been negative, leaving policy makers baffled regarding what to do next.

Let's Try This Again

Let's Try This Again

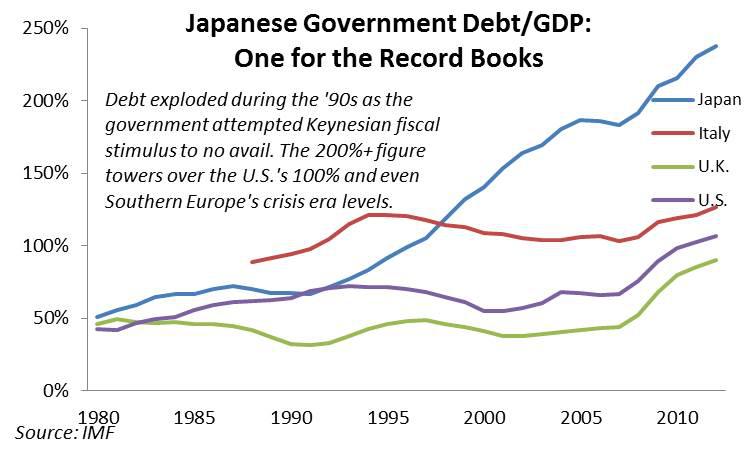

If the goal of the 1990's Keynesian fiscal stimulus was to jack government debt to GDP to the highest ratio in the world, then it was a resounding success. The U.S. has famously just crossed the ominous sounding threshold of 100% gross debt to GDP. Years ago Europe blew through its Maastricht Standard of 60% with some countries like Italy and Greece doubling that figure. In Japan, the ratio is broaching 250%. And this does not include private sector and banking debt, which only put the country more deeply into hock.

Knowing that the fiscal apparatus has already been red-lined, Japan's newly elected administration quickly made it known last autumn that it expected more…..much more….from the BOJ in combatting weak growth. The elbow twisting worked. The central bank announced unlimited purchases of financial assets, including Japanese government bonds (aiding the servicing ability of the aforementioned gargantuan debt load). It has also committed itself to achieving an inflation rate of 2%, a far cry from the current negative rate of -0.9%.

Rates and Deflation

Japan's version of quantitative easing is already on top of an interest rate regime that makes the current U.S. Fed seem hawkish. The Fed funds rate is presently in the range of 0% to 0.25%. To remove that subtle ambiguity, the BOJ has nailed its rate to 0.1%. Even with sluggish U.S. growth and distorted treasury markets, the U.S. 10-Year yield has drifted up towards 2% in recent days, leaving the 10YR-2YR spread at around 165 bps. In Japan, the spread is 69 bps. A flatter yield curve denotes weaker growth expectations. These rates are putatively set by markets…ignoring central bank distortions… which means that investors think that at some point in the future, prices may rise in the U.S.

Not so in Japan. Why? Because it is already experiencing a period prolonged deflation. This prospect has long kept advanced market policy makers awake at night. Yes inflation is lousy as it lowers the purchasing power of a nation's citizens, but in highly levered economies, deflation…or wide-spread falling prices…packs a one-two punch. First is lowers aggregate demand as consumers put off purchases, expecting prices to drop even further. Second, lower revenues put corporations at risk of default as they may not be able to cover fixed interest costs. That could lead to bankruptcies and layoffs on the corporate side and similarly, home foreclosures on the consumer side. A classic debt deflationary cycle. And you thought a hangover was tough to shake.

What has surprised experts about Japan is that deflation has not caused a sudden collapse, but instead a steady bleed of subpar economic performance. The table above illustrates the menace of deflation. At present the real rate of return (nominal minus inflation) on the Japanese 10-Year is 1.72%. Simply put, without the presence of inflation, consumers may as well keep their money invested...despite paltry rates….as it at least earns some interest. However, when inflation exceeds interest rates, real rates turn negative, enticing consumers to spend today vs. losing money in their savings accounts tomorrow. Case in point: if Japan was already at its 2% inflation target…..which it never will be….the real rate on the 10-year would be -1.18%. Time to go shopping.

Monkeying With The Market

The Bank of Japan's….as well as the Fed's and ECB's….commitment to low interest rates and asset purchases, by design, greatly impacts financial markets. On the obvious side, central bank purchases of safe assets like government bonds, force investors farther out along the risk spectrum into high-yield debt, equities and assets emanating from emerging markets. In addition to goosing demand for risky assets, lower interest rates…at least theoretically….positively impact asset prices in a couple of ways. First it enables firms to refinance debt at lower rates, and perhaps undertake debt-driven activities such as share buybacks, capital investment and acquisitions. All of which can be welcome developments for shareholders. Also there is the simple math that lower interest rates increase the present value of future cash flows from financial instruments, whether they be bond coupons or dividends. So it is no surprise that a commitment to asset purchases and low rates should spur an equities rally.

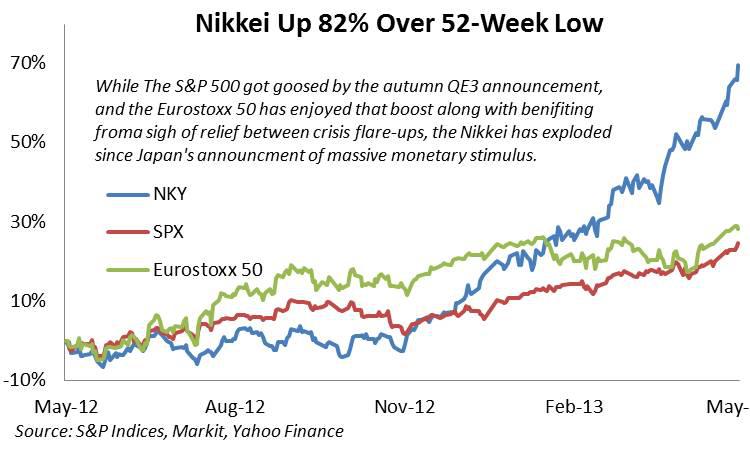

That said, any index that climbs 70% over the course of 52 weeks…especially in a low growth environment…should cause investors' eyebrows to furl. Yet this is exactly what has occurred with the Nikkei Index, which has put the rallies in the S&P 500 and European shares over the same period to shame.

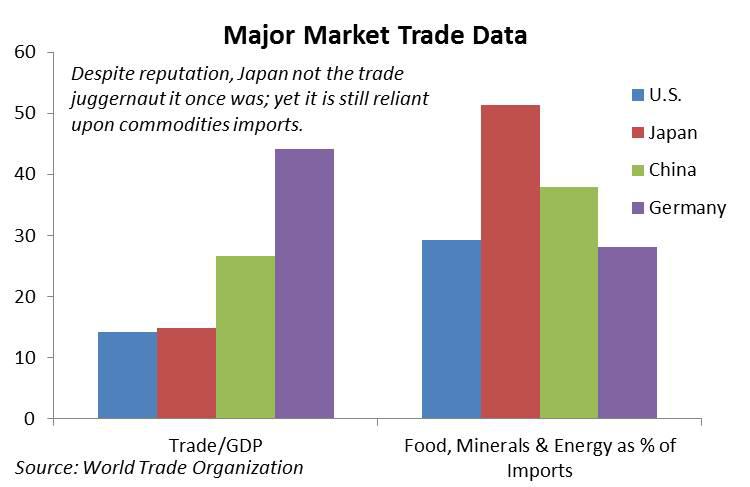

Another catalyst for the Nikkei's rally is the aforementioned weakening of the Yen. This, at least on paper, makes sense too, but with a large caveat. A cheaper currency not only makes a country's products cheaper vis-à-vis foreign competitors, but it also boosts domestically-denominated corporate earnings when foreign profits are translated back to the local currency. So a weaker Yen should boost corporate performance…but at the cost of imported inflation. Japan is a resource poor country, at least with regard to energy and mining products and to a lesser extent, foodstuffs, which together comprise 50% of the country's imports compared to 29% for the U.S. and 28% for Germany. As these commodities are traded internationally in dollars, the weaker Yen would cause prices for the key building blocks of the economy to rise. Yes, the BOJ's goal is to drive up inflation, but the imported variety is notoriously difficult to control.

A Savers Revolt?

It seems to defy logic that Japan has been able to get away with its astronomic debt/GDP ratio for as long as it has. One reason for this has been the fact much of it is held by local creditors, often domestic savers. Local creditors don't have to worry about a real or de-facto JPY devaluation hammering the value of their investments. Italy has been able to bear its chronically high debt load for similar reasons.

The Japanese propensity to save has been one of the reasons why its currency has long been considered a safe-haven in times of economic tumult. Falling currencies and rising inflation tend to punish savers. The long-standing assumption has been that, for political reasons, Japan won't garrote its thrifty citizens by doing anything too egregiously stupid on the policy front. This latest salvo by the BOJ may have finally thrown this idea out the window. It now appears that authorities have sided with the corporate sector by preferring a weaker JPY and rising profitability over the predictability of real returns in Japanese savings instruments.

But what happens if the savers revolt? They were notorious practitioners of the Yen-denominated carry trade during the last decade, borrowing in their low domestic rates and investing in higher-yielding emerging markets and Australia. Anecdotally this is happening again, this time with juicy-yielding southern European bonds as the destination. A nightmare….but plausible…scenario is domestic savers…tired of low rates and messy government finances… dumping sovereign debt en masse akin to rats fleeing the proverbial sinking ship. Should a tipping point in local demand be reached, liquidity would dry up, foreign investors would be second out the door, and interest rates would sky rocket, driving a wooden stake through the heart of an already comatose economy. Although the need to reflate the economy is obvious, the risks associated with these policy tools are perilous. Let's wish them luck.

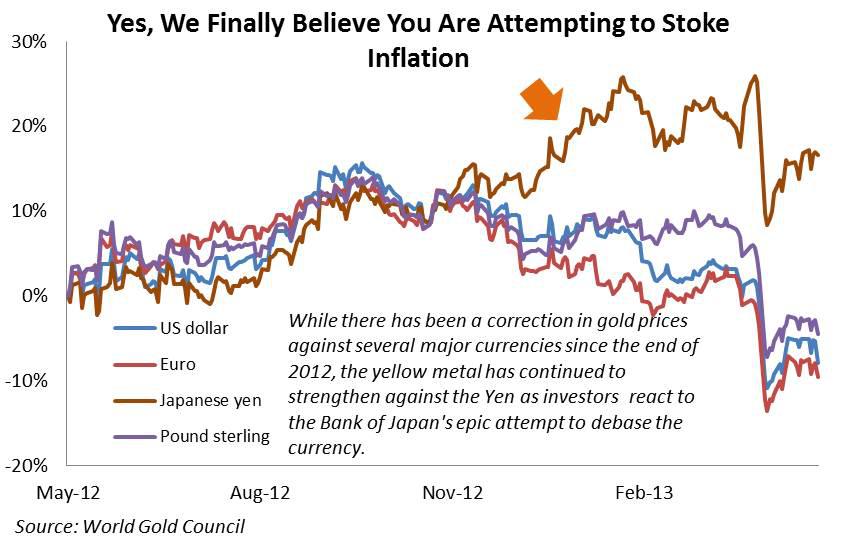

Gold As the Barometer

Although not a gold bug, the market for the yellow metal at times does provide prescient insight into the minds of investors and their expectation of price stability and currency prospects. This is especially true when there is such a divergence in gold prices in various advanced economy currencies. Although Europe, the U.S. and Japan have all implemented dovish policies and show no fear in debasing their currency, it is only the JPY that has continued to lose value against gold over the past several months.

This means that investors may have a stronger belief that BOJ officials will keep its foot on the gas long after the ECB and Fed begin to ease up on asset purchases and low rates. The fact that gold is hitting record highs in JPY perhaps represents the possibility that the party is over scenario described above is upon us and Japan may face a future of no growth, illiquid credit markets and a debased currency. Gold and other real assets make good investments in times of crisis.

Don't Look Away Now

With regard to these subjects, there are many similarities between Japan and the United States. Both have high government debt to GDP ratios, are stuck in a post-crisis, low growth funk, have interest rates at historic lows and have instituted unprecedented stimulative policy responses. Much of what has been described here can be placed in the financial repression bucket, meaning policy aimed at transferring wealth from creditors to debtors to pay for past fiscal sins. Yet equity markets in both countries are surging. Toss Germany in there as well, given that the DAX has just touched a record high. Yes, markets should be forward looking, but record highs in low growth environments give hint that something is amiss. Should these rallies be fueled largely by central banks crowding investors out of less risky assets, then there will be a price to pay once the bubble…..and that is what it would be….finally pops. Even more daunting is the plight of sovereign debt markets once central banks dial back their purchases and it is left to market to determine the credit-worthiness of over-leveraged entities. Recent ambiguous statements about the how and when of the Fed's eventual exit strategy don't carry much weight being that policy makers are in unchartered territory and the textbook was tossed out long ago.

On a brighter note, the U.S. is not Japan. Is it greying, yes? But it is also a nation of net-positive immigration and is alone among advanced economies with regard to favorable demographics. It is also resource rich and is on the cusp of becoming even more so if it figures out a way to take full advantage of newly accessible shale-based energy reserves. It also holds the world's reserve currency, meaning that it can get away with backdoor devaluations than other countries (but on the flipside, it has a much large external debt position than does Japan). All this said, as Chairman Bernanke did years ago, it would be wise for U.S. and European investors to study Japanese developments in real time to determine how its policy successes and misfires impact economic growth and investment portfolios in the months and years to come.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.