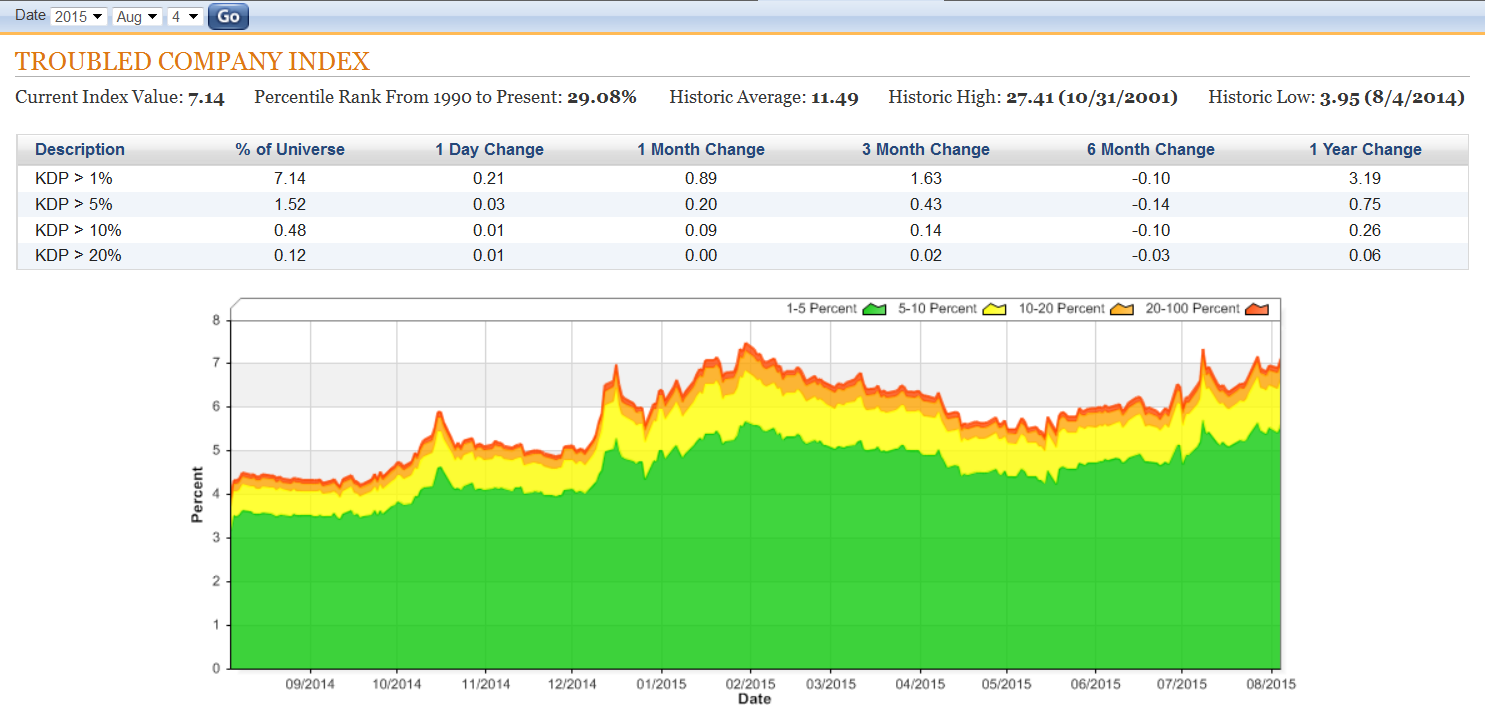

Kamakura Corporation reported today that its troubled company index was up 0.21% to 7.14%. At this level, the index is at the 71st percentile of corporate credit conditions over the period from 1990 to the present. The record low in the index, the 100th percentile, was 3.95% set on August 4, 2014. The all-time high in the index was 27.41%, recorded on October 31, 2001.

For the most recent ranking of the best bond trades in the U.S. market, ranked by the ratio of credit spread to default probability, see this premium post. The best value ranking measures the bond risk and return for all heavily traded bonds, including the firms at the top of the troubled company ranking.

The Kamakura troubled company index measures the percentage of more than 36,000 public firms in 61 countries that have annualized 1 month default risk over one percent. The average index value since January, 1990 is 11.50%. Since November, 2010, the Kamakura index has used the annualized one month default probability produced by the KRIS version 5.0 Jarrow-Chava reduced form default probability model, a formula that bases default predictions on a sophisticated combination of financial ratios, stock price history, and macro-economic factors. The version 5.0 model was estimated over the period from 1990 to 2008, and includes the insights of the worst part of the recent credit crisis. The countries currently covered by the index are Argentina, Australia, Austria, Bahrain, Bangladesh, Belgium, Brazil, Canada, Chile, China, Colombia, Cyprus, Denmark, Egypt, Estonia, Finland, France, Germany, Greece, Hong Kong, Iceland, India, Indonesia, Ireland, Israel, Italy, Japan, Jordan, Kuwait, Luxembourg, Malaysia, Malta, Mexico, the Netherlands, New Zealand, Norway, Oman, Pakistan, Peru, the Philippines, Poland, Portugal, Qatar, Russia, Saudi Arabia, Singapore, Slovakia, Slovenia, South Africa, South Korea, Spain, Sri Lanka, Sweden, Switzerland, Taiwan, Thailand, Turkey, the United Arab Emirates, the United Kingdom, the United States, and Viet Nam.