This is an excerpt from a blog published earlier today:

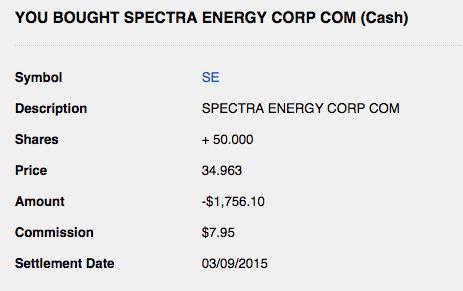

Stocks, Bonds & Politics: Sold 2 Linn Energy 2020 Senior Bonds at 90/Paired Trade: Bought 50 Spectra Energy (SE) at $34.96 and Sold 50 BMLPRJ at $21.14As part of my income investing strategy, I am constantly doing what I call paired trades. I am in effect substituting one income producing security for another. There could be a variety of reasons underlying that kind of switch.

I will be discussing the purchase of Spectra Energy, a large energy infrastructure company.

To finance this purchase in part, I sold 50 shares of the equity preferred floating rate stock BMLPRJ. That security pays qualified and non-cumulative dividends at the greater of 4% or .75% above the 3 month Libor rate on a $25 par value. Final Prospectus Supplement

I have discussed in two recent SA Instablogs the advantages and disadvantages of floating rate preferred stocks that pay the greater of a minimum guarantee or a spread to the 3 month Libor rate.

Equity Preferred Floating Rate Stocks: Added To MSPRA At $19.87 - South Gent | Seeking Alpha

Equity Preferred Floating Rate Stocks: Added 50 GSPRC At $19.63 - South Gent | Seeking Alpha

Since the Federal Reserve started its Jihad Against the Savings Class back in 2008, these floaters have been stuck at the minimum coupon rates and that is not likely to change for at least two more years and possibly longer.

In effect, an investor is paying an insurance premium in the floater's price representing the difference between its current yield and the yield of a fixed coupon preferred stock from the same issuer. The insurance is for the onset of unexpected and problematic inflation that would take the short term rates well above the trigger point for the activation of the float provision.

The problem is that problematic inflation does not appear to be in the cards anytime soon, so I only dabble in these equity preferred floaters and have resorted to trading them in small 50 to 100 share lots. Notwithstanding the small exposures, I have managed to generate $11,823.6 in net profits so far (snapshots at the end of the Gateway Post for this niche security: Stocks, Bonds & Politics: Advantages and Disadvantages of Equity Preferred Floating Rate Securities). However, most of those gains were generated by buying a few of these stocks when their prices were pulverized during the recent Near Depression.

Simply put, I view SE to be a better overall total return vehicle than BMLPRJ at the moment. I am focused on income generation. I recognize that income is produced by dividend and interest payments as well as harvesting capital appreciation. A realized capital gain is spendable income just like a dividend.

I executed a paired trade since I am maintaining my cash allocation near 25% based on my capital preservation objectives, views about the risks and opportunities of various asset classes, and the fact that I do not have to swing for the fences.

Bought 50 Spectra Energy (SE)(natural gas super cycle strategy)(see Disclaimer):

Snapshot of Trade:

Prior Trades: I have never owned the common shares prior to this purchase. I bought and sold several times a trust certificate that had as its underlying security a senior bond issued by Spectra Capital. That security, formerly traded under the symbol JBI, has been redeemed by the call warrant owner. Call Warrant Owner Redeems JZV and JBI A trust certificate is a category of exchange traded bonds. Most of the trust certificates have been redeemed by the call warrant owners.

Company Description:

Spectra Energy Corp. (SE) is one of the large pipeline and midstream infrastructure companies with operations in the U.S. and Canada. Those operations include 22,000 miles of natural gas, natural gas liquids, and crude oil pipelines; approximately 305 billion cubic feet of natural gas storage; 4.8 million barrels of crude oil storage; and natural gas processing, gathering and distribution operations.Spectra has a 50% interest in

DCP Midstream Partners L.P. (DPM), "the largest producer of natural gas liquids and the largest natural gas processor in the United States". The Annual Report has a map at page 21 showing the facilities operated by DPM. There is commodity exposure in this business since DCP is exposed to the spread in natural gas liquids and dry natural gas. The one year price chart shows significant price weakness in the DCP units: DPM Interactive Stock ChartSpectra is also the general partner of

Spectra Energy Partners L.P. (SEP) and owns a 82% equity interest in that MLP, page 5 10-K The last SEC filed Annual Report contains a number of maps that show the facilities, owned by SEP, that SE controls through its 82% equity interest in SEP. SE-2014.12.31 10K The market price for SEP units have held up much better than DPM: SEP Interactive Stock ChartSE also owns Union Gas Company that is engaged in natural gas storage and distribution, with approximately 1.4M customers in Canada's Ontario province, pages 17-18, SE-2014.12.31 10K.

SE also owns natural gas pipelines, gas gathering and processing facilities in Western Canada, page 18.

Spectra is close to a pure play on natural gas demand through its collection of economic rents for transporting, storing and distributing natural gas.

The stock consequently plays into my natural gas super cycle theme. A large part of that super cycle will be driven by the construction of combined cycle generating plants, using gas turbines, to provide both baseload and intermediate power requirements. A baseload generating station using gas fired turbines will be burning natural gas 24/7, rather than the historical use of those turbines to meet only temporary peak demand. The Natural Gas Super Cycle: Bought Back First Trust ISE-Revere Natural Gas Index Fund - South Gent | Seeking Alpha

SE currently has a 4 star rating by Morningstar with a fair value estimate of $44 and a consider to buy price of $35.2. So my first purchase is at least under that consider to buy price. S & P rates the stock at 3 stars with a $36 price target.

The 52 week high at the time of my purchase was $43.12. The 52 week closing high was $43 from 7/22/14. I suspect that the price has been pressured by the crash in crude oil prices as well as the decline in dry and liquid natural gas since hitting that high.

Chart: Crude Oil Prices: West Texas Intermediate (WTI) - Cushing, Oklahoma St. Louis FedChart: Henry Hub Natural Gas Spot Price-St. Louis Fed

Chart: Natural Gas Liquid Composite Price-St. Louis Fed

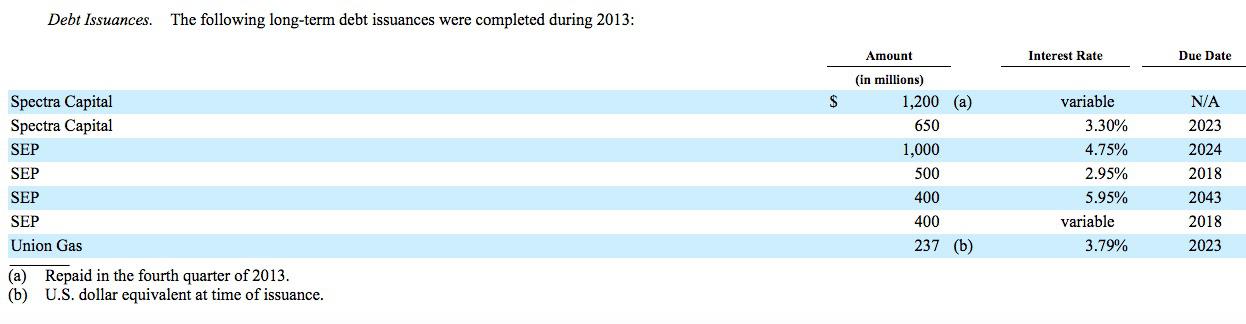

Spectra has been a beneficiary of the abnormally low interest rate cycle. In February 2013, Spectra Energy Capital sold $650M in senior unsecured notes, with a 3.3% coupon, maturing in 2023. Prospectus Spectra Energy Partner's (SEP) was also able to sell a lot of debt in 2013 at favorable rates:

Sourced Page 58 SE-2014.12.31 10K

Sourced Page 58 SE-2014.12.31 10K

Back in January, Moody's reaffirmed its Baa2 senior unsecured debt rating for Spectra Capital but changed the outlook to negative for the reasons given in the report. S & P currently has a BBB- rating on SE's senior unsecured debt, with Fitch at BBB. (Bonds Detail)

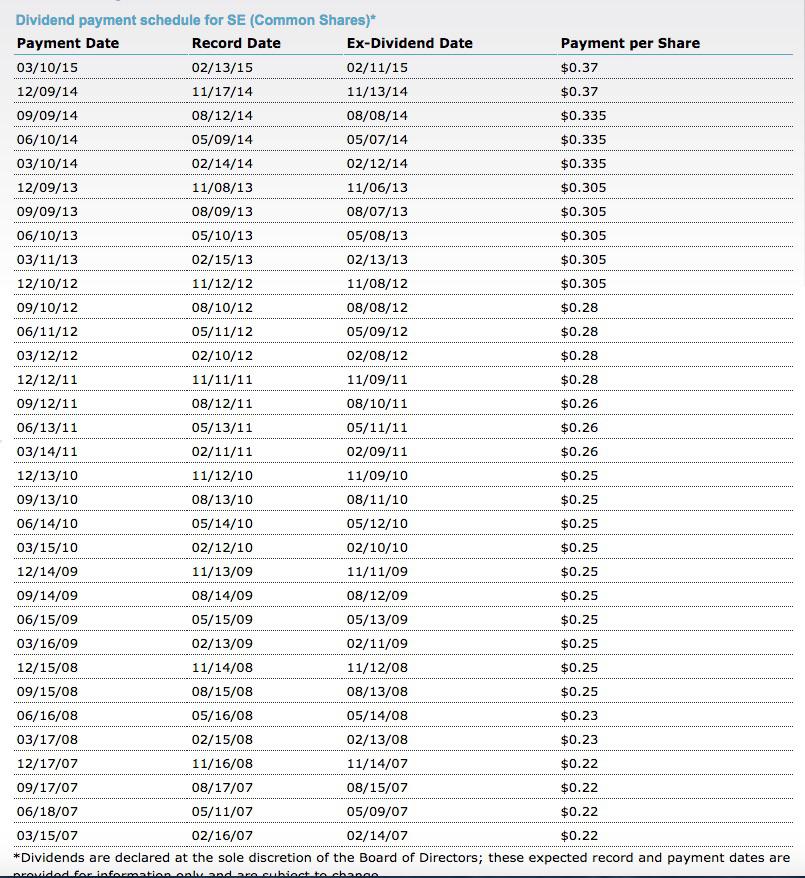

Dividends and Company Projected Dividend Increases: The quarterly dividend rate has increased from $.22 per share (2007) to $.37 now:

There is no dividend history prior to 2007. Spectra Energy did not exist as an independent company until it was spun out of Duke Energy (DUK), with that spin out completed in early January 2007.

Assuming a total cost per share of $35 and a $.37 quarterly rate ($1.48 annually), the current dividend yield would be about 4.23%.

Based on its current forecasts, SE anticipates that it will be able to increase its dividend by 9% per year through 2017. News Release (2/5/15)

SE has raised its dividend in the 4th quarter. The last raise took the rate up to $.37 from $.335 effective for the 2014 4th quarter payment.

I calculate that a compounded 9% annual increase will result in a $1.92 annualized rate by the 2017 4th quarter or about a 5.49% dividend yield at a total cost of $35 per share.

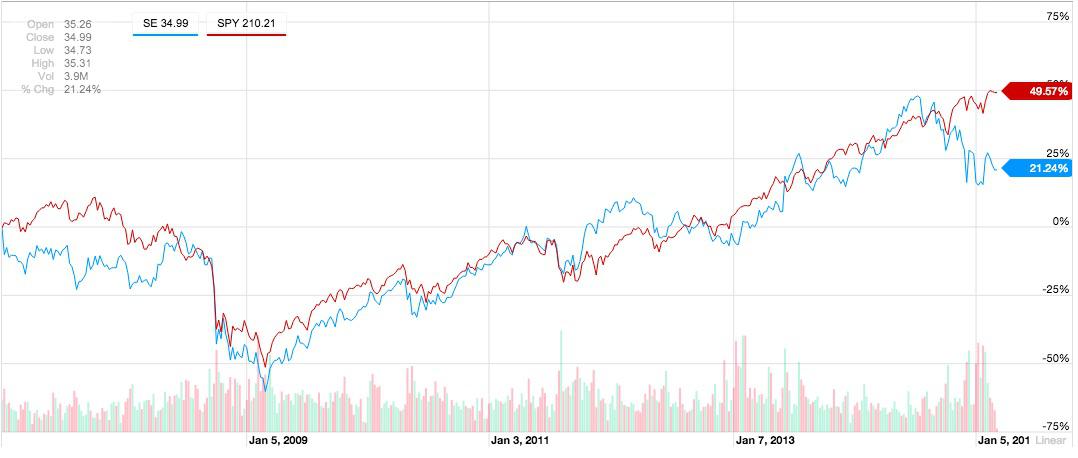

Chart: I drew a chart from 1/3/2007 through 3/3/2015 comparing the prices of the ETF for the S & P 500 (SPY) and SE. I am not surprised that SPY has outperformed on a price basis, but the gains in both securities are subdued when using that starting point rather than focusing on SPY's robust move since March 9, 2009:

SPY vs. SE: 1/3/2007 through 3/3/15

When dividends are reinvested, the total annualized return for SE during that period was 7.02% compared to SPY's 7.2%. That just highlights the importance of total return that includes dividend reinvestments. Calculator On a price basis, SE was about 28.33% below SPY's price appreciation, but both securities had similar total return numbers.

Recent Earnings Report: SE reported 4th quarter EBITDA of $810M, up from $798M in the 20134th quarter. Distributable cash flow was reported at $316M for the quarter and $1.46B for 2014 (up from $1.29B in 2013). The cash flow coverage for the dividend was at 1.6x, exceeding SE's forecast of 1.4x coverage. The company also discusses in its earnings release the current status of its growth projects which I will not summarize here. E.P.S. was reported at $.47 for the quarter and $1.61 for the year.

Here at some links to articles discussing this report: MarketWatch and Market Realist

SE's forecasts for 2014 are contained in this 2015 Business Outlook and Financial Plan.

Most investors, which is just my best guess, value companies like SE and Kinder Morgan based on distributable cash flow rather than GAAP E.P.S.

Morningstar has the price to cash flow at 11.4.

Rationale: SE was bought as a potential total return vehicle. I simply have a rational hope that a combination of the dividend and share price appreciation will produce a 10% annualized total return. My prospects for achieving that goal have improved some due to the recent price correction. SE seems to be in a prime position to capture economic rents from the increased use of natural gas.

A recent article published at SA and titled "Spectra Energy: Delivering Record Gas Throughputs To Northeastern Markets" highlights that positioning in one market.

Morningstar estimates that SE moves about 12% of the natural gas consumed in North America.

I am trying now to keep this section simple and to focus on the core reasons.

Risks: The company summarizes risks incident to its operations starting at page 27 of its last SEC filed Annual Report: SE-2014.12.31 10K

When I look at Spectra, what sticks into my brain is the huge debt load that will need to be refinanced and refinanced, over and over again, and will likely increase significantly over the years.

Spectra calculates its total debt exposure at $14.7B as of 12/31/14 in its earnings press release (page 7) The maturity schedules of the fixed coupon debt obligations can be found at pages 96-97. Those debt obligations are presented on a consolidated basis and consequently include SEP, Union and DCP debt.

Trying to avoid hyperbole and hyperventilation, I would just note that there is a lot of interest rate and refinancing risks embodied in that debt load. And, SE's debt is borderline investment grade now. One reason for nibbling now is the sheer size of that debt and the potential dangers that load poses to common shareholders at the bottom of a top heavy capital structure. (see also page 61 and note 16 starting at page 96, SE-2014.12.31 10K)

Another potential problem is that the natural gas super cycle, which I envision, will be short-circuited by a rise in solar distributed power generation, a subject that I recently discussed in comments to my article about electric utilities: A Word Of Caution About New Purchases In The Utility Sector | Seeking Alpha I probably would not want to own SE twenty years from now for that reason on top of the debt load. Whenever an investor starts predicting the future, perhaps it is best to predict often which will improve one's chances of success. This vision thing can lead to big bucks or sometimes it is more of a delusion than a vision which proves prescient.

Future Buys/Sells: This 50 share purchase is a starter position. I will probably not go over a $5,000 exposure given my perceptions about the risks particularly those involving the debt. I will most likely average down when and if the share price falls below $33, buying another 50 share lot and possibly another 50 shares at $30 or below. I would then consider selling the highest lot on a push toward $40 and then look for an opportunity to buy back that lot at below my then existing average cost per share. That is what I call small ball.