Idea of the Week: A New Twist in Text Analysis

http://link.reuters.com/rud92t

Abstract: The risk of information overload has never been higher; failing to keep track of all the data companies generate increases the risk of falling into a value trap. StarMine's Text Mining Credit Risk Model helps in rapidly assessing that data to help identify companies like R.R. Donnelley that demonstrate characteristics associated with those value traps.

The stock market has been on the rise in recent weeks, but the same can't be said of the level of conviction on the part of investors. If you find yourself worried that you might be missing some crucial piece of data or insight into one or more of your portfolio companies, you are far from alone. It doesn't help, either, that these days simply keeping abreast of all the information about those portfolio holdings is far more demanding a task, much less winnowing through it all in quest of a piece of data that might not even be there - but that if it is, might warn you of otherwise hidden risks. Bulls and bears alike may be forgiven for feeling like another species altogether - a deer in the headlights.

R.R. Donnelley (RRD.O) may be a case in point. The company is best known in the business world for printing telephone books; on Wall Street, it's known as a favorite target of short-sellers, with 28% of its shares outstanding sold short. The shorts appear to have plenty of reason for concern. Historically, Donnelley has been a cash cow, but in recent quarters, its cash flow from operations has lagged compared to its net income.

Donnelley's debt to equity ratio skyrocketed to 328% at the end of 2011 from 153% the prior year. Another concern is the $1.22 billion underfunded pension obligation, which accounts for 115% of equity. Moreover, shareholder equity dropped due to acquisition-related write-offs. Donnelley's operating profit margins have fallen steadily from their recent highs of 10% in the fourth quarter of 2008, and while they now appear to be inching their way higher, currently at 7.7%, remain below the industry median.

But given that Donnelley trades around $11, 24% below where it started the year: the chart below clearly demonstrates why this is a stock that may well look "cheap" to bargain hunters. Long-only value managers may find the stock alluringly inexpensive. Could the shorts be wrong? Certainly, after its long slide (see Figure 1), the stock appears "cheap"; the StarMine Intrinsic Valuation model ranks the company in the top 5% of all North American companies. Of course, these investors are all well aware that there's a risk that a stock which appears attractive may prove to be a value trap, but trying to figure out which company documents might contain crucial information is, in many cases, a hit or miss proposition.

Figure 1: RR Donnelley's (RRD-O) decline may entice "value" buyers.

Part of the problem is that investors don't always have the right analytical tools to help them manage all the data that contains clues to whether companies like R.R. Donnelley are values - or value traps. Although designed as another way to assess the probability of default of a company more effectively than the Altman Z-score, the newly-released ((JOHNNY, PLS LINK NEWLY-RELEASED TO THE PRESS RELEASE THAT SOMEONE WILL SEND YOU))Text Mining Credit Risk (TMCR) Model may help point out which documents may warrant a more intensive and thoughtful scrutiny on the part of interested investors, as they may hold the clues as to whether the company is either a bargain or something that is cheap for a very good reason. While it is designed to alert investors of credit-related dangers and the prospect of future defaults, it also has utility value for analysts and portfolio managers trying to better grasp the risks associated with investing in the company's equity.

Fundamental analysts pride themselves in uncovering material information in text documents, whether these are news items, brokerage firm research reports, SEC filings or transcripts of quarterly earnings conference calls. The Text Mining model adds a quantitative element to this historically qualitative activity by identifying the most important documents out of the hundreds or even thousands that an investor may have to scour for clues. It does this by scoring each one from a bearish one to a bullish 10.

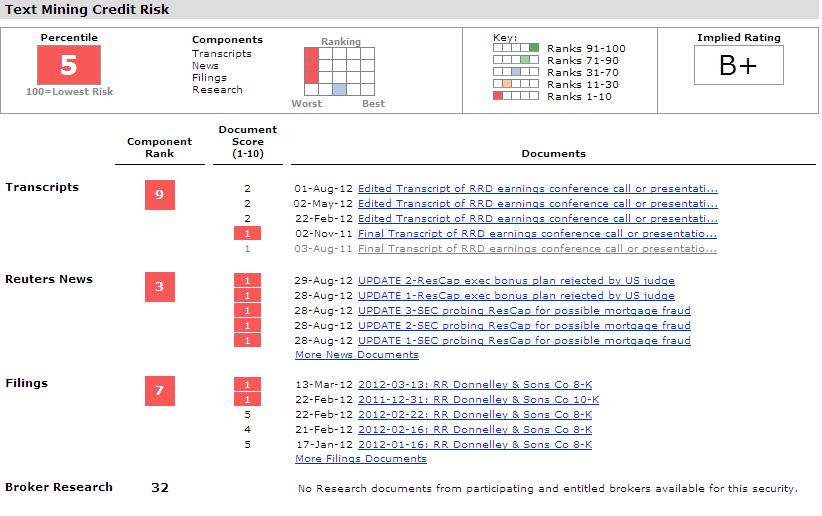

In the case of RR Donnelley, the company's overall TMCR score shows a low 5 on a 1-100 scale (See Figure 2, below). While the company scored 32 out of a 100 on the StarMine model's broker research component, it fared far worse on the model's three other components. It scored only 9 on earnings call transcripts, and merely 1 or 2 out of a possible 10 on the four most recent documents. (Those scores might well prompt a curious potential investor to click on the documents themselves, to get a better understanding of just what comments the model views as being so worrying.) The News component also scored poorly, only 3 out of 100, with all the documents in view scoring 1 out of 10. The same is the case for the company's recent filings: the overall score is a mere 7 out of 100, with the two most recent documents ranking 1 out of 10.

Figure 2. StarMine Text Mining Credit Risk Components for RR Donnelley (RRD-O)

One example of the kinds of wording that can generate a low score and alert investors to problems within the company comes in the form of an August 2, 2012 earnings call transcript. That includes a question from an analyst to management about debt reduction plans and potential bond buybacks of their high-yield debt. (See Figure 3, below.) The specific words used in that document meant that it scores a bearish 2 on a scale of 1-10.

Figure 3. StarMine Text Mining Credit Risk "Transcripts" component analysis ranks the August 2, 2012 release a low 2, on a scale of 1-10.

(see link above for text section)

Arguably, the steep declines in Donnelley's share price may mean that the bear case is already priced into the stock, while a rebound in the U.S. economy may help buoy the company's fundamentals and help rout the short sellers. But the fact that Donnelley's dividend yield stands at 9% today, at a time when those of more blue-chip "cash cow" companies are at half that level or even less, is another red flag. So the low score on the StarMine Text Mining Credit Risk Model may give investors a reason to pause and contemplate the possible consequences of an investment in what may turn out to be a value trap.

Long-only investors may use this kind of text-mining tool to identify avoid potential value traps; others may find it useful in identifying opportunities for short sales. Text mining has been a valued and valuable tool for quantitative hedge fund managers, in particular, for several years, and now it is demonstrating its utility for fundamental managers as well, whether used as a screen or to provide a "check" on a manager's instincts or impressions. Although the text mining credit risk model can't be seen as a "single decision" tool on whether to buy or short R.R. Donnelley's stock, it can provide a research shortcut, one that may help persuade risk-averse investors to pause on the sidelines - at least until that ranking improves.

-0-

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.