Note: We are less than a month away from a critical FDA PDUFA date for this ~$4.50 a share biopharma stock. For a Free 10 page report on why I think this event could power significant capital appreciation through the rest of 2016 for this undervalued equity click here.

I have been investing since I was a teenager in the stock market and I am coming up on the Big 50 this September. I have lived through the go-go 80s and 90s where double digit annual equity returns seemed like a given most years. Thanks to pro-growth policies and some good fortune, the domestic economy churned out three, four or even five percent GDP increases like clockwork.

That does not mean there were not shocks to the market like the 1987 October crash, the Mexican Peso crisis of 1994, the Asian crisis of 1997/1998 or the Internet Bust of 2000. However, these seem mild to what has occurred over the past decade. The financial crisis was the worst economic shock since the Great Depression and we have been stuck in the weakest post war recovery on record since the recession "officially" ended in June 2009. The last time the economy grew at a three percent or better clip was 2005, which seems a lifetime ago.

No major economy seems to have a found a way fiscally to accelerate economic growth although the huge boost in regulation worldwide certainly has been one key factor why business formation and growth are so tepid. Key structural and labor reforms as well as large and overdue infrastructure programs have largely been ignored or have failed to be implemented both here, Japan and in Europe.

This has left the heavy lifting to try to boost economic growth to the major central banks. Despite their best efforts, these monetary efforts have largely failed to boost growth but have been a boon to asset values such as in real estate, art and of course global stock markets until recently. This has been a key factor in the acceleration of wealth inequality which has become a fashionable election year topic. These initiatives also have resulted in some numbers I never thought I would see in my lifetime.

The ten-year treasury currently yields 1.55%, within shouting distance of its all-time low of 1.39%. Those yields are generous compared to what is available overseas. The ten year German Bund actually went under zero percent last week. The Swiss yield curve is negative all the way out to the 30-year bond and the 10-year British Gilt hovers just over 1.1% despite the U.K. being on the brink of voting to leave the European Union which would bring about a large economic disruption. Over $8 trillion, yes trillion with a T, of European sovereign debt now carries a negative interest rate. Both the European and Japanese central banks are in uncharted territory with their current negative interest rate policies.

An investor who parachuted in from a decade ago would think he had landed in a Twilight Zone episode. This is the madness that has been brought about by well-intentioned but in my opinion, quite ineffective central bank policies across the globe.

So what is an investor to do in this environment? Given the state of Europe and the divergent policies of the Federal Reserve and the European Central Bank; it is most likely the dollar continues to rise against the Euro. This will continue to be a headwind for the earnings of large multi-nationals and it is a key reason earnings within the S&P 500 are about to post their five straight quarter of year-over-year profit declines when second quarter earnings start to come in early next month. I continue to be underweight large companies such as IBM Corporation (IBM) that get a good portion of their earnings from overseas especially from Europe.

Domestically focused small cap stocks are much less expose to overseas headwinds and that is a primary reason the Russell 2000 has outperformed the S&P 500 over the past three months. The small cap sector had been a laggard since late 2014 when the Federal Reserve ended its last quantitative easing program.

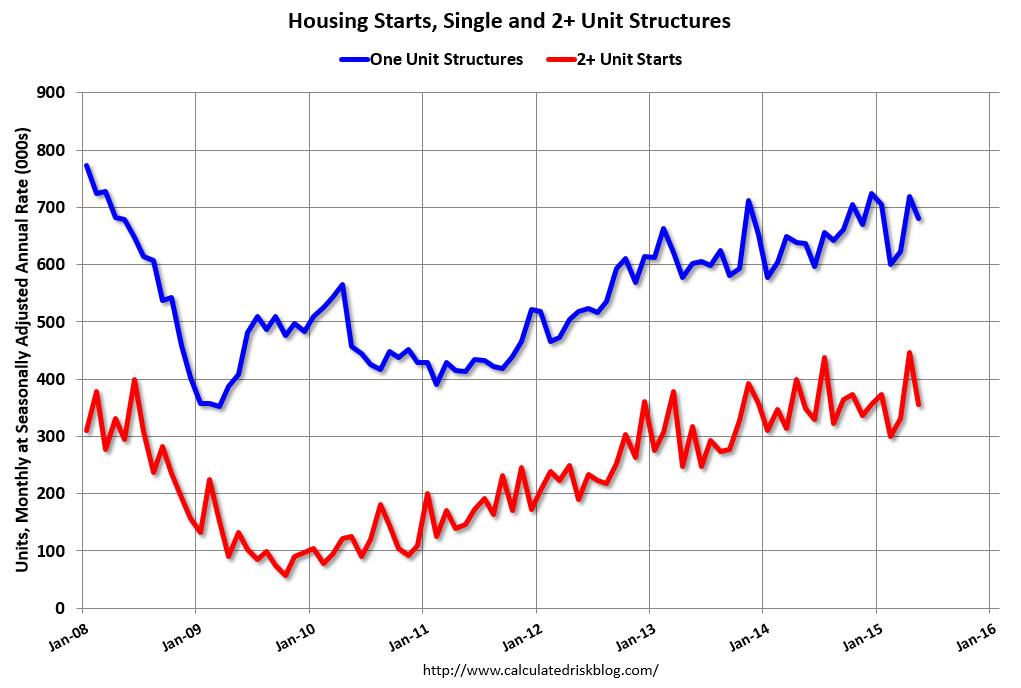

One also has to like the home building stocks as lower yields means rock bottom mortgage rates. Combined with decent job growth, loosening credit underwriting and pent up demand; the housing market should be solid for at least a couple of years outside a significant domestic recession. I continue to like LGI Homes (LGIH) and Taylor Morrison Home Corporation (TMHC), which I have profiled several times on these pages, as my two favorite home building stocks. Both companies are seeing impressive revenue and earnings growth and sell at large discounts to the overall market multiple.

Anything with a safe and solid dividend yield selling at reasonable valuations should also hold up well as investors scrounged for income in the low yield world we currently live in right now. Chatham Lodging Trust (CLDT) continues to be my top pick in the lodging real estate investment trust space. I have held this REIT for almost four years now and both the stock price and dividend payout have doubled over that time period. Chatham yields just over six and a quarter percent after raising its monthly dividend payout again earlier this year. Diamondrock Hospitality (DRH) and Hospitality Properties Trust (HPT) are two other holdings I have in this high yielding subsector of the REIT space.

It will be interesting how historians look back a decade from now on the monetary policies currently being engaged by the world's largest central banks. Somehow I don't think they will be viewed kindly at that point, but for the sake of the global economy and markets I do hope I am wrong in that assessment.

Thank You & Happy Hunting

Bret Jensen

Founder, Biotech Forum