Demand for commodities has become a leading indicator for the future growth of the global economy. One way to look at this is through shipping rates. As shipping of raw commodities picks up, it is evident demand has risen, and in turn, shipping rates will rise. This is all fine and dandy, except this is not what we are seeing here. So how does one play the almost stagnant shipping market? Well hopefully this article will shed some light on a few different plays.

We will begin by looking at the Baltic Dry Index, which is the Baltic Exchange's freight index that tracks shipping rates for commodities across 26 different shipping lanes. Various raw materials are shipped via ocean vessel, including but not limited to iron, grain, coal, and others. After declining for 35 straight days and over 37% year to date, the Baltic Dry Index has finally showed some signs of life. The index has risen for 13 of the past 15 days, a 16.3% increase from a recent bottom in mid July. This is a positive sign given the talk of a double dip and a global economic slowdown. The chart below shows the movement of the index dating back to 2009.

The index reached its peak in May of 2008, which was followed by an unprecedented 94% drop in shipping prices through December 2008. Since then, the index has bounced around, as global demand remains sluggish. This recent push forward in prices is only a small step, providing an indication that demand for these raw materials has remained subdued.

The Baltic Dry Index serves as a leading indicator in that it provides an estimate of demand for raw material inputs, which are used in the production of other goods. However, the recent decline in prices may not fully reflect a drop off in demand. It should be noted that when the index was rising back in 2007, production of additional vessels was put into motion. Now that these vessels have been completed, the increased supply of ships could also bring downward pressure on prices. Both of these theories will be examined in an attempt to shed some light on a few different plays.

We will first take a peak at demand for the leading cargo, iron ore, and one of the largest importers of this commodity, China. Chinese importing of this particular raw commodity, which is used in the production of steel, has stalled as of late. As China attempts to cool it's economy, demand will remain low. As the graph shows, imports have dropped as of late, and this is certainly taking its toll on the BDI. If demand continues to slip, expect to see the BDI remain at standstill, at best.

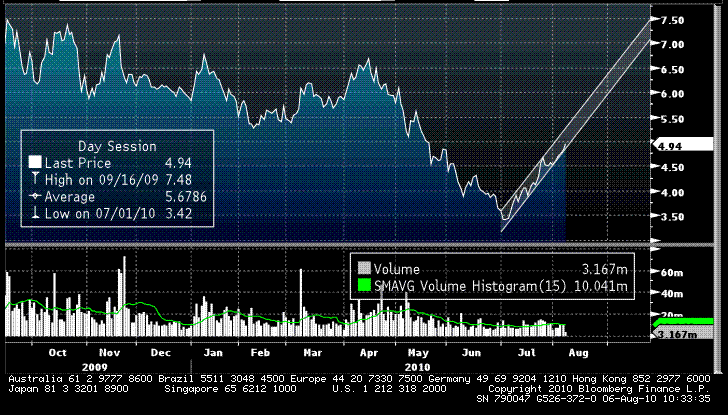

So if there is supposed to be a large amount of capesize ships coming to fruition, why not get in on DRYS? DryShips Inc “owns and operates dry bulk carriers,” as the name implies. The company moves major bulks and also owns Ultra Deep Water Rigs, which gives some nice exposure to the recovering offshore drilling sector. But I digress. DRYS has solid fundamentals with consistent revenue dating back to Q4:08. The company is also in a better financial position, with a 54% gross profit margin compared to 36% average of its peers. The company as has much less debt than the average of the companies I surveyed.

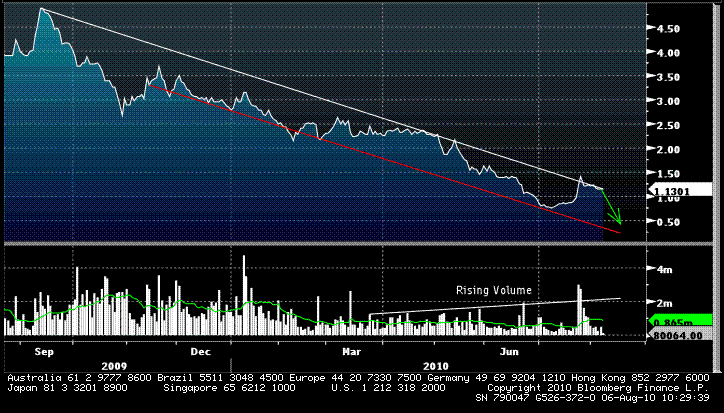

Looking at another small cap stock, ONCF, is one I think would be a solid short. "The Company is engaged in transporting drybulk cargoes, including such commodities as iron ore, coal, grain and other materials and crude oil cargoes through the ownership and operation of nine drybulk carriers and four tanker vessels." The company has negative EPS, at -4.86, and mountains of debt compared to its competitors. For example, long-term debt to assets sits at 84.07%, while its net profit margin is -133.84. A recent splitting of shares has diluted earnings nicely as well. Clearly, the drowning shipping market is taking ONCF down with it. It appears that this ship is sinking with the shipping market, multiple puns intended.

The final play I will suggest would be SEA. The Claymore shipping ETF, which "seeks investment results that correspond generally to the performance, before the Fund’s fees and expenses, of an equity index called Delta Global Shipping Index (the “Index”). The Index is designed to measure the performance of companies listed on global developed market exchanges and currently consists of companies within the maritime shipping industry." If one thinks that the shipping index is going recover quickly, this maybe a solid place to park some cash. I personally would not advise it since the fund actually stopped trading in April and has since exploded. I think a correction is due, and once investors realize that sea freight is a slowing industry, this fund will get hit.

All in all, it is important to look at the global macro factors that are influencing this particular industry. As demand for raw materials slows, it will lead a chain reaction that may leave many companies and fund devastated.

Disclosure: No positions