Todd Krajniak is one of the fine people I have met here on Seeking Alpha. Todd is the founder of Krajniak Capital Management, LLC. On June 14, 2014 Todd published the following newsletter and with his permission I have posted it as an Instablog.

I recommend KNDI followers read this. As a KNDI follower you will be familiar with many of the events detailed by Todd. Like myself, what I think you will find most interesting is the insight and conclusion that Todd offers.

Kandi Technologies Group (KNDI) - What Are "They" Hiding?

6.15.2014

By Todd Krajniak

Why we were in the KNDI position originally

China needed a smog reducing solution for its new found love of the automobile.

Kandi's Quick Battery Exchange offered to bring a sensible solution to the shortcomings of EV.

I saw the two seat EV being sold without the battery similar to the original cell phone or toner fed printers; a disposable product which quickly and cheaply established dependence on a new technology. Instead of it being cell phone minutes or toner replacements, it was the battery exchange.

Why we are in KNDI now

China still has smog and the politics pushing the shift to EV are hardening like cement.

Depending on the region in China, KNDI's cars can cost less than the announced subsidies.

KNDI's Quick Battery Exchange patents have Kandi well positioned to own the patents of the industry standard EV "fuel pump".

We discovered KNDI for our investors over two years ago in the $3 price range, big name institutions are just now discovering KNDI.

What I got wrong in my initial analysis of KNDI

I did not understand the Chinese culture.

In the west, anyone with $1 is king of the minute. The world stops for that person until they pay for their hamburger. China is a patriarchal top down culture where giving people or entities ranking higher in the protocol pyramid their respect and ability to maintain 'Face' is more important than results.

China's patriarchal culture has slowed down the EV implementation significantly. Once the obvious was obvious which was Kandi had developed and tested a viable EV solution in Jinhua, before it could be rolled out, it had to be adopted and negotiated at every subsequent level up to Beijing. Then EV programs had to be announced as being implemented all the way back down from Beijing through Hangzhou and Jinhua. This process seemed to have to be repeated with subsidy adoption, approval, and now implementation.

What about the KNDI epic short seller drama?

KNDI has endured one of the most public and drama filled short battles I will see in my life time. Most of the hit pieces are available at Seeking Alpha, along with many bullish articles. Reading through the comment sections following the articles one can get a feel for all of the drama.

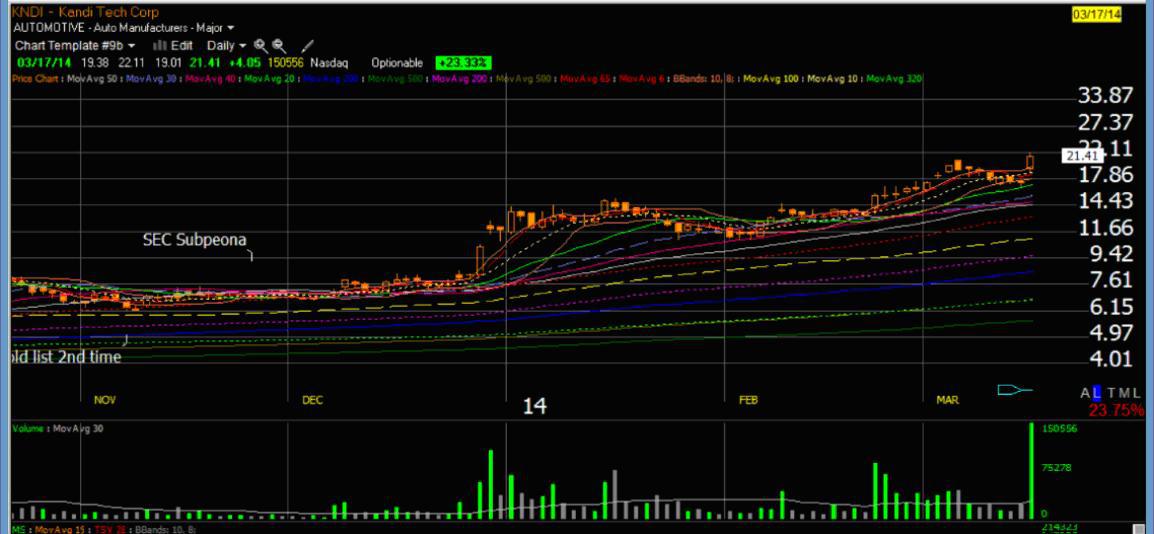

To get a grip on the story line of how a 300,000 share short position turned into a 6,400,000 share short position and what it means going forward it's best to look though the chart by periods of history and offer a little commentary to illustrate the evolution.

On September 21, 2012, Arthur Porcari sourced a PRC policy paper which stated that the Chinese government would act to support a few EV initiatives, one being the KNDI EV program, a couple months after the city of Hangzhou's letter of intent to support Kandi's 20,000 EV leasing program.

As you can see by the following chart, three days later Geo investing published their first major hit piece against KNDI, complete with tales of innuendo and photos of Chairman Hu Xiaoming's house as provided by their in investigator on the ground in China. This crashed the stock to $3.08 before recovering much of the losses by the end of the session.

Through the remainder of 2012 and into 2013, there were a multitude of follow on negative articles from Geo and Sharesleuth.

The real news out of China covered the announcement of a new factory in Huzhou, and the upcoming JV with Geely. It was a very promising news trail that was being assaulted by short sellers. During this period KNDI shares shorted increased to 700,000 shares.

Most of the squiggly lines on the chart are moving averages. I keep them there for reference as many computer trading programs will buy and sell along those lines in a pre-programmed fashion. As you can see by the selloffs in the above chart, buyers were waiting along the longer term moving averages.

Then on June 5 2013, the nightmare began.

Well... it's been a nightmare for the fund that had been shorting the stock.

Going into June 5, the stock traded roughly 70,000 shares per day, had a 700,000 share short interest, and roughly 19 million shares floating. Much of the float was believed to be held by savvy individual investors who were for the most part self-made men. I met many in Atlanta in 2007 at the first Kandi investor conference. Due to the high conviction of this base of successful individual shareholders, I believe the float available for trading was significantly smaller than 19 million shares. On June 5, the stock traded 18 million shares in volume. It took 60 million shares in volume to contain the momentum run. With a fraction of 19 million available for trading, from where did all of that volume come? If 1% of the 19,000,000 share float trades in a day that's only 190,000 shares. It's my contention that the shares of the float available for trading were significantly lower than 19,000,000. This barrage of volume was well beyond a statistical anomaly - well beyond.

By the middle of July KNDI was on the Reg SHO Threshold list. This means someone counterfeited a significant amount of stock in order to drive the price down.

Jerry Klein, another KNDI shareholder, authors an Open Letter to the SEC, FINRA, and NASDAQ and files the first shareholder complaint to the SEC regarding the counterfeiting at the August 2013 lows.

Into early November, the short sellers had counterfeited enough stock to drive it onto the Reg SHO Threshold list again. KNDI in its 2013 annual report disclosed receiving a subpoena from the SEC regarding an investigation into a matter involving KNDI around Thanksgiving of 2013. No details about the investigation were revealed.

There is still some residual ballyhoo about the unknown nature of the inquiry, but we do know the stock came off the Reg SHO Threshold list and the stock price tripled shortly following the receipt of the SEC subpoena.

After filing the Annual Report on Form 10-K on March 14, 2014, the short fund preyed on the fears of investors by leveraging the SEC subpoena disclosure. They tried breaking the stock yet again driving the short interest up to 6,000,000 shares, approximately 23% of the float. The price was pushed down into the moving average band which I illustrate on this chart template.

The moving averages bring automated trading both long and short. By pressing the stock down into those bands this brings a new class of short sellers providing selling into which the longer term manipulative short seller was able to find supply.

It's my opinion that the short fund which has been working this large short position is trying to cover by holding the price within the moving average bands for the purpose of covering into the automated short selling algorithms. Since the release of the Form 10-K, the number of open out of the money call contracts has increased to be large enough to cover the total short position.

Sooo…, what are "THEY" hiding?

The volume since June 5, 2013 has been uh…. putting it mildly, statistically questionable. After all the private placements and warrant issues and exercises, 1% of the float changing hands in a day would be maybe 260,000 shares, 2% would be around 520,000 shares per day. Since June 4, 2013 (336 days through August 20, 2014) KNDI has traded on average 2,723,000 shares a day, roughly 10% of the float using the averages float during that period.

With all the volume (eighty to ninety percent phantom volume), two tours on the Reg SHO Threshold list, increasing the short percentage to about 25% of the float, and all the hit pieces, why does KNDI continue to print higher lows?

The character of shareholder in this company is different than any I've ever seen. The long term holders are not finance guys. They skew heavily toward self-made business men. The people I met at the 2007 investor/analyst conference in Atlanta were people who made their fortunes having a vision and bringing that vision to reality, despite the mass disbelief in their visions, or having to fend off nuisance law suits, or having to maintain composure while being slandered. They, and including myself, thus 'we', empathize with Chairman Hu's plight. We see the vision through the China smog too.

Since KNDI is extremely conservative about its public and investor relations, the shareholders have had to do their research by translating Chinese media and pooling their efforts through a private yahoo chat group. This group has meticulously sourced and posted hundreds of articles, photos, and feedback from multiple investor trips to visit the company.

This mix of entrepreneurial empathy, hard sought information, and needing to dig for information ten times harder than normal to refute the barrage of short pieces attempting to break the bid so HFT's could run rough shod through the chart has created an insanely strong shareholder culture in KNDI.

The problem the short has is not the 6,400,000 shares short which has likely expanded yet again this week. The conundrum is much more complex. The short has taken a stock which has roughly 26 million shares floating. The actual amount of those share held by people who say "over my dead body will they come out of my cash account" leaves the percentage of float available for trading to likely be significantly smaller than 25.5 million.

With the short interest added to the float, there are roughly 32 million shares available for ownership. What if, due to the commitment it has taken to get ones arms around KNDI the number of shares held in the hands of people who say "over my dead body will they come out of my cash account" is actually greater than say 29 million shares, while institutions are just now beginning to add the stock? And 29 million was picked out of thin air for the sake of the example.

Conceptually, the number of shares of float actually willing to trade is an integer just like interest rates apparently are according to the ECB.

If you take the 25.5 million shares and place them all in the hands of people who put them in a cash account for their great grandchildren, the number of shares available for trading is 0. If 22.5 million of them are in a cash account held for their grandchildren, then the shares available for trading are 3 million. Now what happens if say someone borrows those 3 million shares and through shorting and re-hypothecation sells 6.4 million shares short? For the sake of this example suppose 4 million of those shorted 6.4 million get bought by people who tuck them away into a cash account for their grandchildren? Hmm… negative availability.

It's unusual, but possible that a short fund could hypothecate and re-hypothecate themselves into a position where the amount of shares owned by longs holding long term is greater than the float; hence shares of the float available for trading is a negative number, thus an integer.

If you think that's a statistical stretch, let's discuss the volume in KNDI. The shorts got buggered on June 5, 2013. It took 60+ million shares in volume across two weeks to squelch a short squeeze of 700,000 shares in a stock which did 70,000 shares a day in volume.

Repeat… 700,000 shares short … And it took 60 million shares of volume to defend.

Why did volume never return to its long term resting volume? The float hasn't increased that dramatically. The company's visibility hasn't increased that dramatically. The media driven prejudice hasn't subsided.

If one wants to do something interesting, pull up 1minute charts for the past 2 months. You will find periods where the algorithms are stopped. The stock is mausoleum dead quiet when the algorithms aren't running. That's what they are hiding. Someone has put out 6 million shares in a stock which is illiquid without algorithms running.

Since KNDI isn't ramping and short interest is still growing, do you want to take a guess at who owns those algorithms inflating volume?

Uh, now what boss???

Trading over the past couple weeks feels as though the short interest has increased again, maybe to 6.6 million shares. It's just a feeling.

In calculating days to cover, if one adjusts the float to shares of float willing to trade, the days to cover by implication of fewer shares being available to trade would seem to need to be adjusted higher. Take away the statistically questionable trading volume which has kept average daily volume elevated… let the stock trade without the enhancement of the algorithms and the days to cover goes crazy high. I mean crazy high.

Yes, it is my opinion that someone is running an algorithm base trading scheme for the sole purpose of inflating volume for the purpose of masking the real average daily volume and a days to cover number which accurately reflects the dire situation. Keep in mind, volume went nuts on the breakout where someone sold the stock onto the Reg SHO Threshold list, and volume has not yet come back to a percent of float traded daily level which we see throughout the market.

Getting to a guesstimate on the "Crazy High" days to cover number?

Cross multiply the 'way back' 70,000 shares a day volume on 19 million shares floating with today's 25.5 million share float. Average daily volume proportionately would be roughly 94,000 shares.

Covering 6.4 million shares on 94,000 shares per day would take 68 days. Now that's a crazy high days to cover number. And, that's what I think they are hiding by pushing the statistically questionable volume through the tape.

Obviously, the estimated adjusted days to cover is a loose extrapolation based on my opinion.

In my opinion the short seller has gotten the price to trade down to the algorithms in the moving average bands where he is able to find new sellers into which he can start covering. The number of open out of the money calls has increased dramatically over the past couple months as well. The options specialist is taking on the risk. Even though the responsibility for repurchasing those 6.4 million shares seems to be shifting to a broader group of short sellers, they have to cover at some point - from whom though?

Then again?

Maybe this entire short battle has been a rouse. It's possible that someone large has sold short on shore 6 million shares to other entities in their control which are off shore thus manufacturing an "in" and then they could have started to buy a boat load (official finance 301 term) of out of the money calls stopping them out of their short. It may be labor intensive, but at the end they'll have made a 25% position.

Why I think the game is over for the shorts?

Unit count, institutional awareness, and popular awareness.

We have been sourcing EV production count articles in China which lead us to believe the projects are moving forward.

KNDI's EV dominance is even forcing Jim Cramer's The Street.com who now sources Stocktwits for its content to admit what we've known for our investors for years. KNDI can develop pop culture ticker name recognition as the pied piper effect kicks in.

Major institutions have been starting and / or adding KNDI.

EV subsidies in Hangzhou are expected to begin soon. Subsidies would dramatically accelerate unit count, but the policies of removing old cars from the road and reducing ICE license plates seem to be driving adoption for car share and bulk leasing.

End Game for KNDI?

The rollout of EV programs has not been fluid, but is progressing. Subsidies are in the process of being implemented. This is China we are talking about, so "soon" may have many different meanings spanning from "retroactively to a long time".

"Supportive Policies" have begun. In the west, when we see letters of intent promising supportive policies for a 20,000 vehicle program, we think 'Oh the government is going to buy them'. Not so.

In China, "Supportive Policy" apparently loosely translates to "We will shoot your competitor." http://news.ifeng.com/a/20140619/40808369_0.shtml

Hangzhou has capped internal combustion engine license plates to approximately 6,600 new plates per month while leaving EV plates unlimited. May 2014 there were 280,000 applications for the 6,600 license plates. KNDI's Micro-Bus cars also known as the car share program cars, are allowed to use the bus lanes circumventing traffic jams, and China is red-lining older cars taking 5 million off the road with mandates pending to take 13 million off the road.

In the near term, I think the Chinese government is sensing that they can shift demand without actually writing the subsidy checks. These policy shifts seem to have thawed the EV market place just enough for Kandi to get their QBEx cars out into the market place. QBEx being the industry standard seems to be the end goal.

The cars we are seeing going out into the market place are both plug-in and battery exchange. Thus the battery exchange model is getting pulled into existence.

There are and have been concerns that Kandi does not have an M1 license and thus is just a parts supplier. In actuality this mandates that they are an integrator of industry players while implementing an industry standard. They have been positioned to be a supporter to all and competitor to none. Geely through the JV is on board with QBEx. Zyote has recently introduced a QBEx model for Hangzhou's leasing program. That makes two "competitors" who are in the QBEx camp.

KNDI through its Jinhua factory should sell many EV's into the Jinhua and Hangzhou markets along with supplying parts to the Geely JV. While Kandi, through the Geely JV, should sell many, many more EV's. Those numbers are becoming quantifiable for investors who want to do the analysis.

The blue sky yet to be recognized is the marketplace of Chinese auto manufacturers who will have to find a way to partner with KNDI or license the QBEx technology from KNDI. Any way you slice it, plug-in is awful and QBEx offers a recurring taxable revenue stream.

The further out blue sky yet to be recognized is the relationships which follow behind China's purchasing of electric utilities globally. QBEx is a turnkey solution which can be implemented by every electric utility globally allowing them to go head to head with the petroleum industry.

Disclosures:

This is an opinion piece. To find supportive research behind the opinion, please join the KNDI private group at Yahoo.com. There is extensive research available to all members who are interested. Also it's imperative that one reads d1ev.com regularly for current info on the Chinese EV landscape.

KCM is long for our investors, and principle's household accounts. This is not a recommendation. Do your own due diligence. By the time you read this, our position may have changed. You will not have notice of these changes.

As KCM seeks companies undergoing enterprise change which hasn't yet permeated the financial statements, the purpose for publishing this piece is to continue a public dialogue illustrating our thought process in selecting and managing individual positions which are progressing towards being ownable by more conservative strategies. KNDI is 1 stock. It is not our entire portfolio nor should anyone take it as being indicative of our returns for investors. We will be happy to fully disclose our positions current and historical to interested investors.

Krajniak Capital Management, LLC (KCM) does not guarantee the accuracy or completeness of this report, nor does Krajniak Capital Management LLC assume any liability for any loss that may result from reliance by any person upon such information.

The information and opinions contained herein are subject to change without notice and are for general information only. Past performance is not a guide or guarantee of future performance. Consult your financial professional before taking action on any of the information contained within this report.

Some links take you to other sites. KCM is not responsible for the information contained within those sites. Charts provided by worden.com

Past results are no guarantee of future results and no representation is made that an investor will or is likely to achieve results similar to those shown. All investments involve risk including the loss of principle. This document does not constitute an offer to sell or the solicitation of an offer to purchase any security or investment product.

Krajniak Capital Management, LLC ("KCM") is a Registered Investment Advisory Firm regulated by the State of Michigan. The purpose of this newsletter is not to provide investment advice to the general public. KCM does not render personalized investment advice through this medium. This medium is limited to dissemination of general information on KCM services and the KCM mindset. The information provided herein is for informational purposes only and does not constitute financial, investment or legal advice. Investment advice can only be rendered after delivery of the KCM disclosure statement (Form ADV Part 2) by KCM and the proper execution of an investment advisory agreement between the client and KCM. None of the content herein should be construed as individual investment advice. Investment Management is long-term oriented. Any strategies that you consider implementing or changes in your financial situation should be brought to the attention of your professional Investment Adviser. KCM may only engage in providing advisory services in Michigan or states where it has completed a notice filing or is exempted from notice filing. General investment, financial planning or other information shown on this site are for illustration purposes. Nothing herein shall constitute advice, recommendations or personalized consultation.