TRVN-Trevena Inc. $5.74 close of 3/11/15

This is a research report by Stockreversals.com. You can opt in free at www.stockreversals.com or join our SRP Premium service at www.stockreversalspremium.com and get these reports as we send them out. Recent winners include QURE, BLUE, CHRS, CNCE, BLUE, KITE and the list continues. We delve deep into undiscovered plays and hang on and add on dips.

![]()

39 Million shares outstanding- 225 Million Market Cap

9.25 Million issued at $7 in February 2014 IPO; 11 Million issued at $4 in December 2014 raise;

Corporate Presentation (PDF February 2015)

Pre IPO insiders bought 2.1 Million of the 9 million shares in the $7 offering, something we always look for.

Shareholders: Actavis- 18% (ACT); RA Capital- 3 Million shares (Peter Kolchinsky, Harvard Grad with PH.D in Virology, one of the top Healthcare Hedge funds hands down since 2001); Several venture funds including Alta Partners, New Enterprise Associates, Polaris Ventures etc.

Pre-IPO Shareholders stock basis ahead of the $7 IPO was actually $7.27 per share for 16.5 million pre-IPO shares. This happened because at the time of the IPO last year, the Biotechs and the market were under pressure. The IPO was postponed in November 2013 and then finally went off a few months later. So you can actually buy into this stock well below what insiders basis is... a very rare situation. We look to find PRE-IPO shareholders who have a reasonable basis in the stock and not $1 or $2 for example.

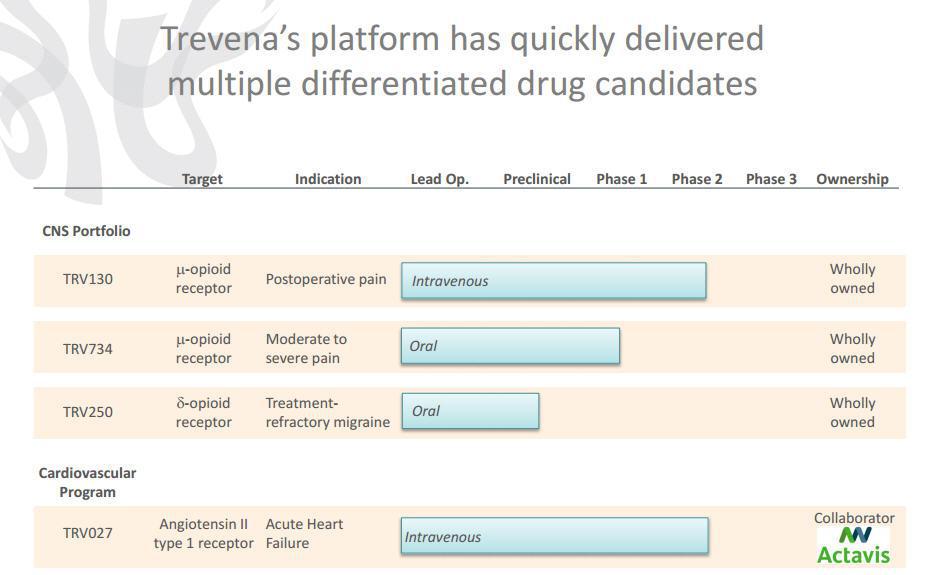

Using its proprietary product platform, Trevena is developing four biased ligand product candidates it has identified - TRV027 to treat acute heart failure (Phase 2b), TRV130 to treat moderate to severe acute pain intravenously (Phase 2b), TRV734 to treat moderate to severe acute and chronic pain orally (Phase 1), and TRV250 for treatment-refractory migraine and other CNS disorders (Preclinical). The patient population for these indications is well over 30 million in total. Compare this to CLDN which is 350,000-525,000 for example.

Trevena's drug discovery and development approach is to identify and develop therapeutics targeting established GPCRs while offering a differentiated and superior therapeutic profile compared to currently available GPCR-targeted drugs. More simply, Trevena is going after alternatives to the standard of care pain killers Morphine and Oxycodone, and Fentanyl. So far they have had impressive early stage results. This is a highly lucrative "pain management" post surgical area of medicine. In addition a phase 2b trial for Acute Heart Failure is progressing very well in partnership with Actavis.

Their Founder, Robert Lefkowitz M.D., won the Nobel Prize in 2012 for Chemistry relating to his work in the GPCR field of science. The company has licensed the technology from Duke University where Dr. Lefkowitz is a professor in addition to his scientific exploits.

"We believe that we are the first company to progress a GPCR biased ligand into clinical trials. The members of our executive management team have held senior positions at leading pharmaceutical and biotechnology companies and possess substantial experience across the spectrum of drug discovery, development and commercialization."

Now you may need to read this passage a few times, but its worth your time:

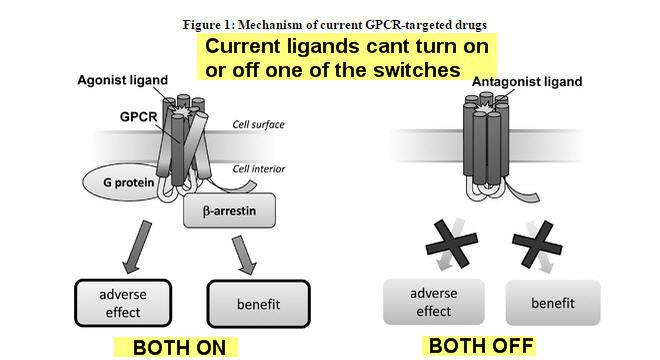

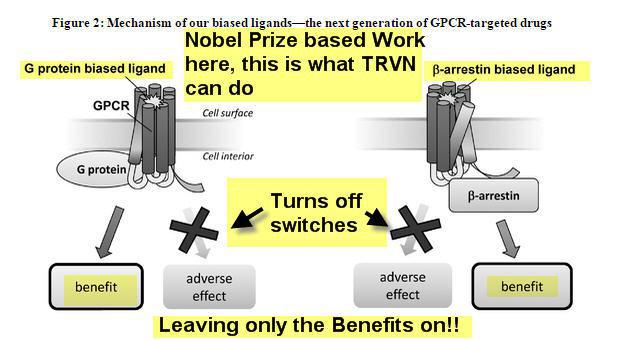

"Currently available therapeutics that target GPCRs, or GPCR ligands, are typically not signal specific, and therefore either inhibit both the G protein and b -arrestin pathways (an antagonist ligand) or activate both pathways (an agonist ligand). This lack of signal specificity often results in a suboptimal therapeutic profile for these drugs because in many cases one of the pathways is associated with a beneficial therapeutic effect and the other is associated with an undesirable side effect (see Figure 1). We use our proprietary Advanced Biased Ligand Explorer, or ABLE, product platform to identify "biased" ligands, which are compounds that activate one of the two signaling pathways of the GPCR and inhibit the other (see Figure 2). This signaling specificity is the basis for our drug discovery and development approach, which is to identify and develop therapeutics targeting established GPCRs while offering a differentiated and superior therapeutic profile compared to currently available GPCR-targeted drugs."

Essentially the science here is TRVN operates a traffic light as it were, so it can turn on and off signals whereas current standard of care products such as Morphine and Oxicodone can't. This means better and more efficient efficacy, less side effects, and lower dosage requirements, less costs for hospitals etc.

Lets look at some images to help out:

This is what current Ligands have a problem with:

Now this is what TRVN Nobel Prize Winning chemistry does that is different:

Pipeline: (Heart Failure, Post Op pain, Acute and Chronic Pain, Parkinsons, Migraines and more)

Trevena is taking this trade secret and proprietary technology and developing several initial targets in the clinical trials. Post Operative Pain (Intravenous), Acute and Chronic Pain (Oral), Parkinsons Disease, Depression, Pain (Oral), and Migraines (Oral). All of those are wholly owned by TRVN and as yet have not been licensed or partnered. They are also partnered with Forest Labs for Acute Heart Failure (Intravenous), and that is advancing rapidly with 620 patients currently enrolled in a phase 2b.

Acute Heart Failure-With Forest Laboratories, now owned by Actavis after 2/2014 acquisition covering much of the costs. AHF indications include portions of some 20 million patients living with heart failure in the US and Europe. Actavis option: potential $65M exercise after delivery of data Additional potential milestones of $365M and 10-20% royalties. Top line data due out 4th quarter 2015.

TRV027 as a first-line, intravenous, or IV, treatment in combination with standard diuretic therapy for AHF patients. We expect data from this trial to be available by the end of the fourth quarter of 2015. If subsequent Phase 3 development is successful and TRV027 is approved by regulatory authorities, TRVN believes TRV027 would be used as a first-line in-hospital AHF treatment. Also, TRV027 could improve AHF symptoms, shorten length of hospital stay in the short term, and potentially lower readmission rates and mortality rates in the long term.

A recent UPDATE on this phase2b Trial was just released this week. "Trevena and Actavis have agreed to weight future enrollment toward the most promising dose and to increase target enrollment in the study from 500 patients to 620 patients. Actavis, which holds an exclusive option to license TRV027, will fully fund this expansion of the study via a $10 million payment to Trevena."

Unlike current therapies, TRV027 has shown beneficial effects on the three key organ systems affected in heart failure, the blood vessels, heart and kidneys in our preclinical studies and Phase 1b and 2a clinical trials. In combination with standard diuretics, we believe these effects may translate into improvements in symptoms and outcomes such as hospital readmission rates, length of hospital stay and mortality rates if TRV027 successfully completes Phase 3 development and is approved by regulatory authorities. Safety studies have also been extremely impressive.

Its important to note that Actavis (Forest prior to acquisition) has been granted an exclusive option to license TRV027, which may be exercised at any time before TRVN delivers Phase 2b clinical trial results to Forest and during a specified period of time thereafter. If activated, Activis will have an exclusive worldwide license to develop and commercialize TRV027 and specified related compounds. They would be responsible for subsequent development, regulatory approval and commercialization of TRV027 at their expense. TRVN could potentially receive up to $430 million in the aggregate, including an upfront option exercise fee of $65 million and milestone payments depending upon the achievement of future development and commercial milestones. TRVN could also receive tiered royalties between 10% and 20% on net sales of licensed products worldwide, with the royalty rates on net sales of licensed products in the United States being somewhat higher than the royalty rates on net sales of licensed products outside the United States. A U.S. patent directed to TRV027 has issued and is expected to expire no earlier than 2031.

TRV130- Post Operative Pain indication:

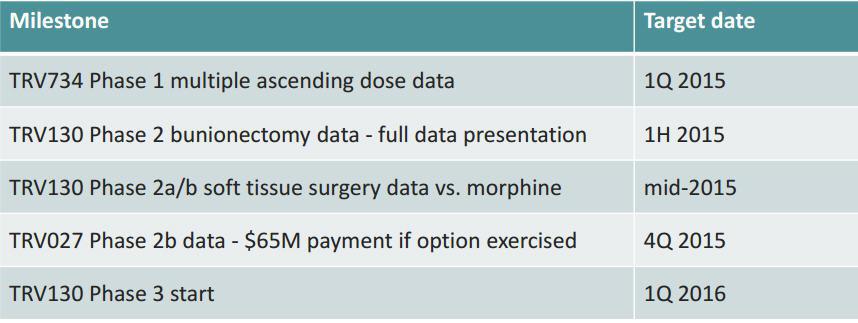

November 2014 phase 2a met endpoints and progressed to phase 2b (click to read PR)

January 2015 Phase 2b begins (click to read PR) with top line due mid 2015 then on to phase 3 which is also setting up parallel with phase 2b work...Phase 3 expected to start in January 2016

TRV130 is an intravenous G protein biased ligand that targets the mu opioid receptor. Trevena is developing TRV130 for the treatment of moderate to severe acute pain where intravenous therapy is preferred, with a clinical development focus in acute postoperative pain. 47 million scripts were written in 2013 for post op pain.

In studies so far a patient can take a lower dosage of TRV130 vs Morphine and get equal or better effect with less side effects. At a slightly lower dosage, peak patient pain relief was dramatically better than Morphine. (Source: Page 14 Slide Investor presentation). Higher magnitude, faster onset, and better response rate vs. standard of care so far.

"We believe that the management of moderate to severe, acute postoperative pain represents the largest opportunity for an intravenously administered µ-opioid therapy like TRV130. Accordingly, we plan to focus our clinical trials on the treatment of surgical patients. We believe avoiding the side effects typically associated with the activation of the µ-opioid receptor will position TRV130, if approved, to more effectively treat postoperative pain than currently available µ-opioid therapies, thereby expediting postoperative recovery and hospital discharge." (From IPO prospectus)

Despite the development and adoption of guidelines for the management of postoperative pain and the extensive use of current treatments, significant unmet need remains. In a survey of 250 surgical patients in the United States, over 70% of the patients undergoing in-hospital procedures reported pain in the postoperative period before hospital discharge, of which almost 50% experienced severe or extreme pain. The dosing of the most effective class of analgesics currently available, m -opioid agonists, is limited by severe side effects such as respiratory depression, nausea and vomiting, constipation and postoperative ileus, which is a condition that most commonly occurs after surgery involving interruption of movement of the intestines in which the bowel enters spasm and stops passing food and waste. TRV130 showed superior analgesia compared to a high dose of morphine, while causing less respiratory depression, nausea and vomiting in a phase 1 trial.

TRV734: orally administered follow on to TRV130 compound for the treatment of moderate to severe acute and chronic pain

Opioid drug sales across the United States, Europe and Japan were almost $11 billion in 2012. Opioids are used to treat moderate to severe acute and chronic pain. However, these drugs are limited in their safety and tolerability by constipation, nausea and vomiting, and respiratory depression.

TRV 734 is a small molecule G protein biased ligand targeting the µ-opioid receptor. "TRV734 takes advantage of a well-established mechanism of pain relief by targeting the µ-opioid receptor, but does so with enhanced selectivity for the G protein signaling pathway, which we believe, based on preclinical studies and clinical trials, is linked to analgesia as opposed to the b -arrestin signaling pathway associated with side effects. Subject to successful non-clinical and clinical development and regulatory approval, we believe TRV734 may have an improved efficacy and side effect profile as compared to current commonly prescribed oral analgesics, such as oxycodone." From IPO prospectus 2014

We have completed full preclinical safety pharmacology, toxicology, genotoxicology and pharmaceutical development studies and have an active investigational new drug application, or IND, with the U.S. Food and Drug Administration, or FDA. We have completed enrollment in a second Phase 1 multiple ascending dose clinical trial and expect to report data from this trial early in the first quarter of 2015. We have retained all worldwide development and commercialization rights to TRV734. We intend to seek a collaborator with experience in developing and commercializing controlled-substance therapeutics in chronic care pain markets, thereby leveraging their expertise while retaining rights to commercialize TRV734 in hospital and specialist markets in the United States.

d -opioid receptor program

We are pursuing a research program to identify an orally bioavailable small molecule G protein biased ligand targeting the d -opioid receptor for the treatment of CNS disorders, of which we intend to initially focus on Parkinson's disease, pain or depression. We expect to complete IND-enabling preclinical studies in 2015. We intend to maintain flexibility on whether to develop and commercialize this product candidate in collaboration with a pharmaceutical company licensee depending on the clinical indications we ultimately decide to pursue, but we intend to retain meaningful commercial rights in any event.

TRV250

"We have identified a new product candidate, TRV250, a small molecule G protein biased ligand targeting the delta-opioid receptor. Based on the initial profile of TRV250, we anticipate focusing our initial development efforts on the treatment of treatment-refractory migraine headaches. According to Decision Resources, a healthcare consulting company, the acute episodic migraine market encompassed approximately 12 million drug-treated patients in 2013 in the United States, representing approximately $2.2 billion of sales. We estimate that approximately 20% to 30% of these patients either do not respond to or cannot tolerate the market-leading triptan drug class, and an additional 30% would benefit from improved efficacy compared to these drugs."

So there is the pipeline, much of the info we took directly from the IPO prospectus filing from February 2014. What we can see our numerous indications getting deeper into the pipeline. The fact that the target populations are so large is what makes TRVN attractive for long term investors. 20 Million heart failure patients in the US and Canada, 30 million scripts per year for Post Op pain, and the list goes on. Migraines effect 10's of millions of people around the world. The fact the founder has won the Nobel Prize for this science and the early safety and tolerability and now efficacy studies are going well is very promising.

We like to find undiscovered Biotech/Biomedical small to mid caps before they are being written about. We wrote up QURE, CNCE, CHRS, BLUE and others way before they took off, some just recently in fact. Sometimes our research reports are met with no movement in share price for awhile, but in almost all cases we see huge percentage moves within weeks to months of our reports as the "A-Ha" moment finally kicks in with the masses. In the case of Trevena (TRVN) we think there is little to no coverage in terms of people writing or talking about them. We also don't think anyone is really adding up all the math and the potential of the huge target populations they are going after with this chemistry.

The market cap for Trevena is still only 225 million. If we were to take 30 million POST Op pain management scripts per year and assign only 20% of those to TRVN future drug (If approved), that alone makes for a 100 million revenue potential on the very low end. 20 Million heart failure patients many of whom receive intravenous drugs via 2.1 million hospitalizations per year, could easily result in hundreds of millions of annual revenue to TRVN down the road. As it stands, an up front payment of 63 million would be payable to TRVN from Actavis as soon as 4th quarter of this year or earlier if they opt to fully license the heart failure indication. That would be reported as earnings and would result in about $1.50 per share in profits alone just on the payment potential.

The company is cashed up with a recent 45 million raise in December along with the 50 million they raised in the IPO 13 months ago. This is enough to take them deep into 2016 and cover the costs of all their trials and more.

Analysts current targets range from $13 to $21 for what its worth.

The chart is building some momentum for a potential breakout in the weeks and months ahead. Consider that many of our research reports do not always result in immediate upside moves CHRS sat from 13-15 for many weeks then ran to 32. CLDN sat from 16-18 for 7 weeks than ran to 26 just recently and so forth. We like to buy while there is some resistance from sellers who have lost patience with the stock. Then we like to keep adding on dips if we continue to like the potential and the science. We have had multiple big winners lately at our SRP service like QURE, ZIOP, CNCE, CMVLF and the list goes on by being patient. We buy stock while people are not paying attention, and then we add and wait patiently for the valuation to move up.

The market cap here as we said is only 225 million and they have enough cash to take them deep into 2016 with multiple catalysts in 2015 as it stands. We estimate they have about 110 million in cash currently. We also would not be shocked to see Actavis consider a buyout of the entire company assuming the Heart Failure indication is doing well in phase 2b. This would make more sense than ACT paying them 65 million up front fee plus royalties, funding requirements, and milestones... but that is just our take.

We see plenty of sellers from 6-6.50, so our thinking is we can accumulate the stock for awhile and then look to the catalysts to likely move this market cap much higher going forward. We have 3 catalysts between now and mid 2015 and another in the 4th quarter of 2015. This market cap could easily double, even to reach the analysts mean target of $14.33 there is a fair amount of upside potential from 6.50 and below.