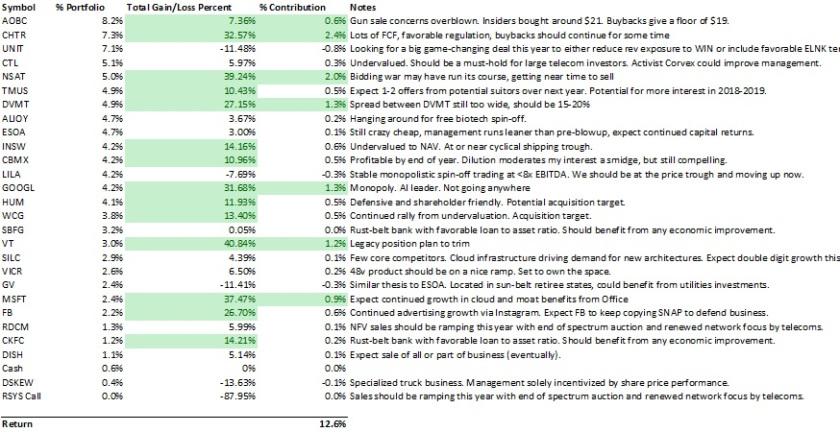

All of my holdings have reported with the exception of American Outdoor Brands Corporation (AOBC), which should report in mid-June. Everything did OK. CombiMatrix Corporation (CBMX), Vicor Corporation (VICR), WellCare Health Plans, Inc. (WCG) and Silicom Ltd (SILC) all legged higher on results. My tech picks are all steadily grinding up. Everything else except my cable/infrastructure picks, Charter Communications, Inc. (CHTR), Uniti Group Inc. (UNIT), and Liberty Global, Inc. (LILA) moved in the right direction. Expectations around CHTR were so high that the stock actually sold off despite reporting decent results. I continue to hold and still consider it a solid long-term position. Overall, the quarter was a good one. I haven't opened any new positions, and plan to look internationally when I do. I have highlighted the top 25% of performers in green.

I'm currently up 12.6% vs. the S&P 500 being up 9% over the past 6 months. It's not bad by any means, but if I can't get a 15-30% return per annum, then I should probably consider simply rolling into a broad market tracking ETF and leaving everything on auto-pilot. I still care more about minimizing losses rather than shooting for the moon, but I also value my time and researching stocks can be time-intensive. My preference is also changing from passively owning parts of companies to full ownership, where I can control the outcomes rather than depending on others to do it for me.

Closed Positions

Time Warner Inc. (TWX) - I closed out my TWX position to fund other opportunities. The spread had narrowed sufficiently to give me a ~10% gain since November, and I have no desire to hold AT&T (T) after the deal closure.

Globalstar, Inc. (GSAT) - My GSAT call options expired worthless. The stock rallied like 2 days after the expiration and would have been exercisable had I rolled the position over. They still haven't nailed down a deal and I'm skeptical that they are top of mind for any potential buyer. If I could find cheap LEAPs for GSAT, I might buy again, but my broker doesn't appear to them.

Twilio (TWLO) - I had a nice 21% gain in TWLO heading into earnings, then watched it turn into a -15.7% loss as the stock cratered on revelations that Uber (UBER) might reduce spending. So I closed out the position. Management sounded really down on the business, and then made some open market purchases. I'm torn about where the stock goes from here, so I'm back on the sidelines. It sounds like Vonage (VG)/Nexmo is getting extremely aggressive on price and that's never good for competitors.

SBA Communications Corporation (SBAC) - I bought and sold SBAC after a 6% gain. At 7x leverage, when the stock does well, it does really well. But you have to watch out when it turns or flattens, and I'm not sure how much room it has to go up from here. It also sounds like they plan to make some additional overseas acquisitions. It's a good time to do so (I think), and I generally want to be more exposed globally rather than solely to the U.S., but I worry about property rights in emerging markets and the high debt. I like the more mature markets where LILA is focused and I added to my position there.

New Positions

CBMX - There is a good write-up here on CBMX. I really like the demographics set-up and I feel the stock is underappreciated for two reasons.

- Investors are discounting the improvements the new management team has made and their commitment to year-end profitability.

- Healthcare stocks in general are still pretty beat-up.

VICR - This Seeking Alpha post has convinced me that 48 volt is going to be the future of hardware, and Vicor owns the space. The author has clearly researched this company intensively and is excited about the prospects. The opportunity in front of VICR is due to an intriguing controlling owner who chose to forego easier research and development avenues for years, which punished the stock. I love finding companies with committed founders who have substantial stakes and plan for the long term.

I've been both a bit too concentrated and a bit too spread out in smaller names for comfort, so I'm working to reduce my portfolio size to something more manageable, under 20 symbols. I don't regard the U.S. market as particularly attractive, but I also wouldn't pretend to understand international or emerging company dynamics as well as I know the U.S. It's something of a conundrum. If domestic valuations stay this high, then at some point we are headed for pain, so I am saving excess cash and waiting for a nice fat pitch.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.