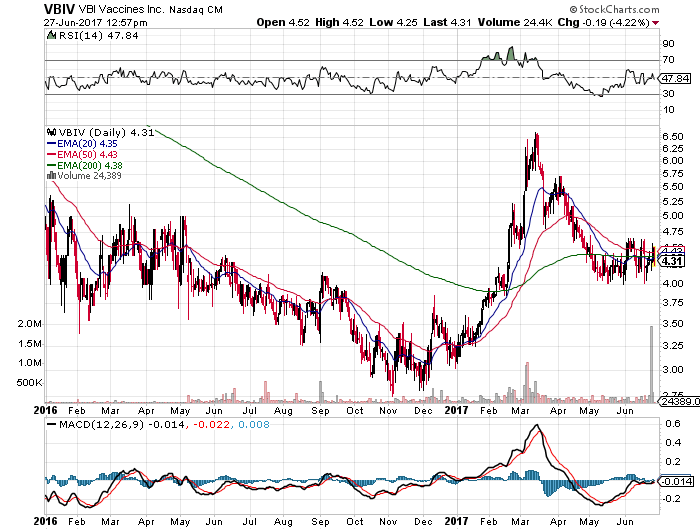

As with most small biotechs, VBI Vaccines (NASDAQ:VBIV) trades in a volatile manner. The stock now trades some 35% from the yearly highs of $6.60 despite some promising developments for the stock during June.

My last research at the end of February highlighted the hidden opportunity in the hepatitis B opportunity. The question now is whether an investor gets another opportunity to buy VBI Vaccines at $4.30?

My last research at the end of February highlighted the hidden opportunity in the hepatitis B opportunity. The question now is whether an investor gets another opportunity to buy VBI Vaccines at $4.30?

Phase 3 Catalyst

Phase 3 Catalyst

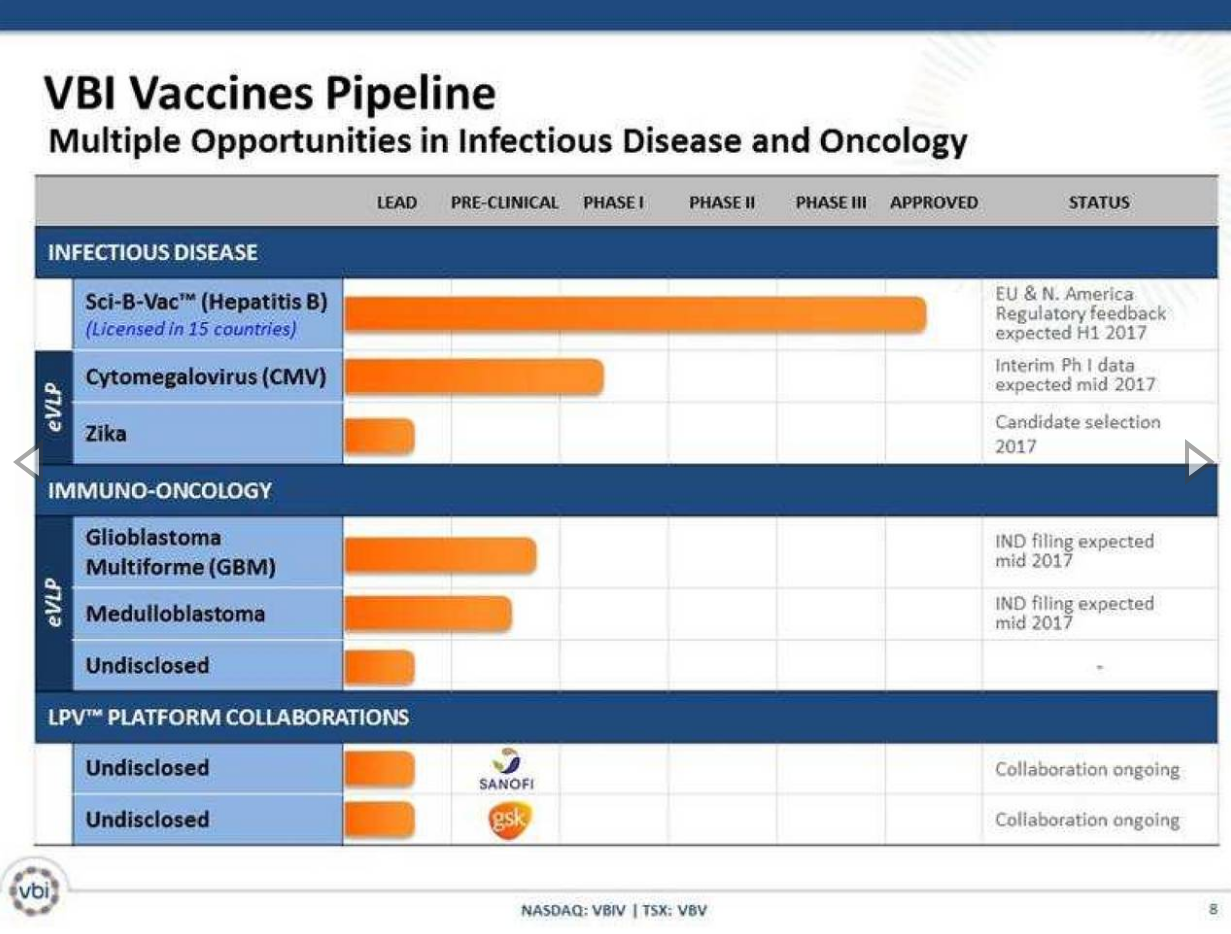

A big part of the merger with SciVac Therapeutics was to combine the management team of VBI Vaccines with the Sci-B-Vac vaccine already approved in 15 countries. The management team would utilize industry knowledge and experience to help advance the hepatitis B vaccine towards Phase 3 clinical trials in key markets like the U.S. and Europe while developing a pipeline of drug candidates for CMV, Zika and other immuno-oncology areas.

The investment theory has been that once the market realizes that VBI Vaccines has a legitimate Phase 3 vaccine candidate, the stock would see a boost. After all, similar vaccine stocks have much higher valuations.

The investment theory has been that once the market realizes that VBI Vaccines has a legitimate Phase 3 vaccine candidate, the stock would see a boost. After all, similar vaccine stocks have much higher valuations.

Last week, the small biotech got positive feedback from the FDA that Sci-B-Vac will not require additional clinical studies to support the Phase 3 study. The company now plans to kickoff the IND in the U.S. and CTAs in Europe and Canada in the 2H of the year.

The key to the story is that the third-generation hepatitis B vaccine has already demonstrated safety and efficacy in over 300,000 patients. The vaccine is approved in the home country Israel of SciVac and 14 other countries.

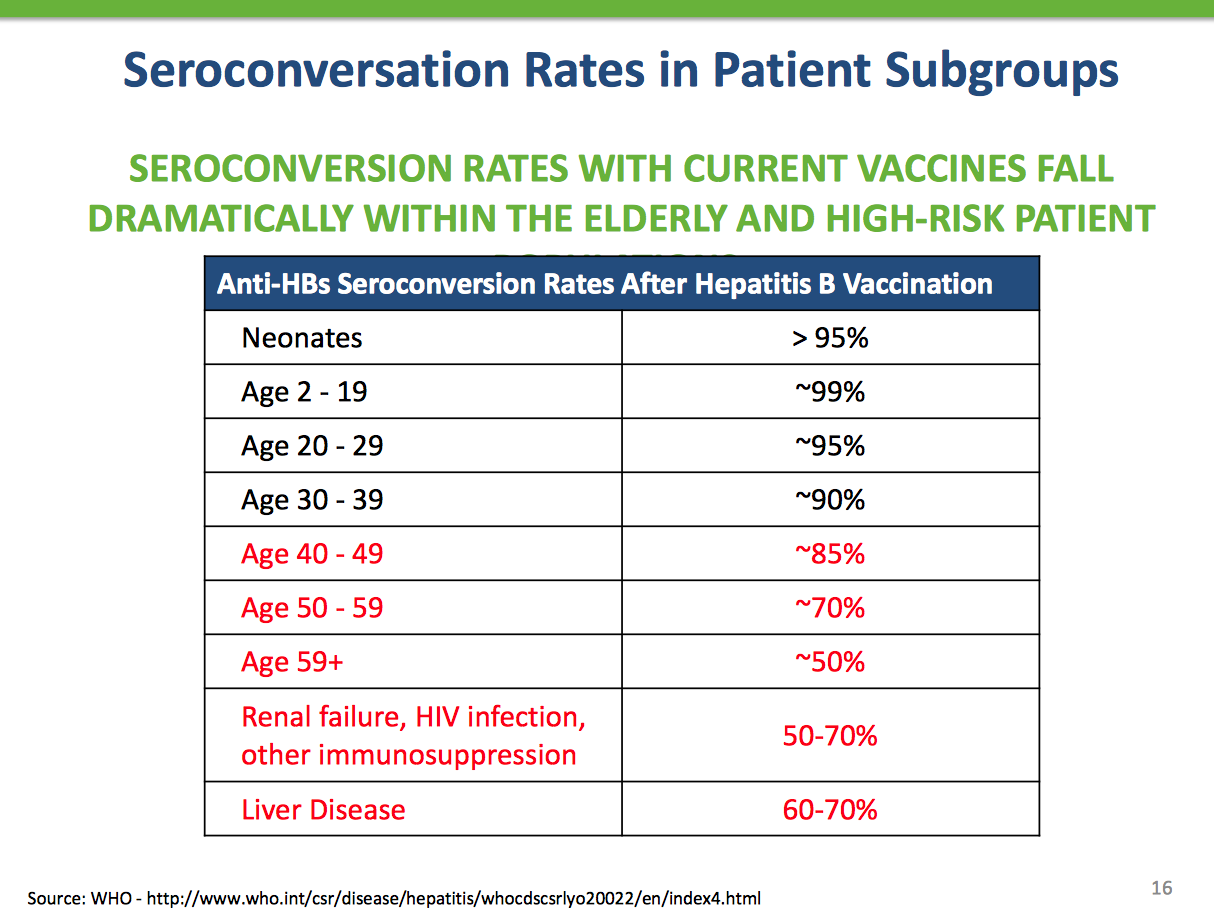

The vaccine provides earlier and higher rates of seroprotection in adult populations compared to the currently licensed hepatitis B vaccines. My previous article linked above further discussed the issues with current 2nd-generation hepatitis B vaccines.

The life-threatening liver infection can be currently prevented by approved vaccines, but an increasing amount of high-risk patients are encountering vaccine failure. Patients that fall into the elderly, obese and high-risk categories amongst others are seeing suboptimal responses to the vaccine.

As Benzinga mentions, the market opportunity for the vaccine is roughly $560 million. The company states that an opportunity of up to $800 million exists in corporate presentations, but investors would be happy with either outcome with the stock valuation currently sitting around $175 million.

As Benzinga mentions, the market opportunity for the vaccine is roughly $560 million. The company states that an opportunity of up to $800 million exists in corporate presentations, but investors would be happy with either outcome with the stock valuation currently sitting around $175 million.

Russell 2000 Addition

As of the market close on June 23, VBI Vaccines was added to the influential Russell 2000 index. The inclusion of this key index and the Russell 3000 further legitimizes the small biotech to the financial community.

The Russell 2000 index is commonly used as benchmark for mutual funds that fall into the small-cap category. While inclusion in the index is a positive signal for the financial community, the stock is not guaranteed success once in the index.

Other small vaccine stocks like Dynavax Tech (DVAX) joined the Russell 2000 back in 2010. Whether or not the addition to the major index propelled the stock higher or not, Dynavax did soar from around $20 to over $50 by early 2012. The small biotech has famously survived failing to obtain FDA approval for Hepsilav-B to only rally back to a market cap over $500 million on promising data from another drug in the pipeline.

Another vaccine focused stock in Novavax (NVAX) joined the Russell 2000 all the way back in 2008 during the financial crisis. The small biotech is worth over $330 million now despite a failed Phase 3 trial last year. The biotech didn't see similar gains after joining the key small-cap index though the market was in crash mode at the time and might not provide the best indication of a normal outcome.

All in all, the inclusion in this large index is a positive for VBI Vaccines and the valuation is intriguing at these levels. These comparative Russell 2000 stocks have valuations double those of VBI Vaccines despite recent high profile failures in Phase 3 trials.

Updated Balance Sheet

One crucial aspect of any small biotech is the capital availability to fund clinical trials. VBI Vaccines is well connected in this aspect reducing the fear of future funding.

The small biotech ended Q1 with $23.5 million in cash on the balance sheet. The company burned about $8.2 million in cash from operations during the quarter.

VBI Vaccines is clear that completing clinical trials including the above mentioned Phase 3 trial will require substantially more funds via equity issuance and possibly more debt added to the existing $12 million outstanding. The company raised over $23.6 million back in December via a funding from Perceptive Advisors. Perceptive is a leading biotech investment firm with over $2 billion under management.

Other key investors include Clarus Ventures, OPKO Health (OPK) and ARCH Venture Partners led by Chairman Steve Gillis. These investments are led by board members with the assumption that VBI Vaccines will easily attract additional funding when appropriate.

Regardless, high risks still remain in any small biotech dependent on rapidly developing technologies and drug therapies. The small biotech remains susceptible to development of competing drugs and the amount of money that larger biotechs can commit to funding advanced clinical trials. Despite all of the big venture funds and key executives at VBI Vaccines, the cash committed is still minor in the big picture.

The failure to obtain FDA approval similar to Dynavax is always a primary risk and even so much more for a small biotech without cash and a large balance sheet to survive a drug failure and move forward on other drug candidates.

Even with positive progress on the drugs, no assurance exists that the market will prefer vaccines from VBI Vaccines. The Hepatitis B Foundation lists a rather lengthy amount of drugs in the testing phase. The list includes some of the biggest biotechs with deep pockets that the company will possibly have to compete against for market share.

Takeaway

The key investor takeaway is that VBI Vaccines continues making progress as promised during the merger with SciVac. The previous approvals of the hepatitis B drug candidate in 15 countries and the solid investment funds involved in this small biotech increase the odds of a positive outcome for shareholders in this highly risky sector.

As with any small biotech, an investment is only recommended for a small portion of a diversified portfolio.

Additional disclosure: VBI Vaccines pays Seeking Alpha a fee to participate in its Corporate Visibility program. This article was submitted independently by Stone Fox Capital and selected by Seeking Alpha's editors for publication. No fee was paid for its publication.