"He had just about enough intelligence to open his mouth when he wanted to eat, but certainly no more." - P.G. Wodehouse

![]()

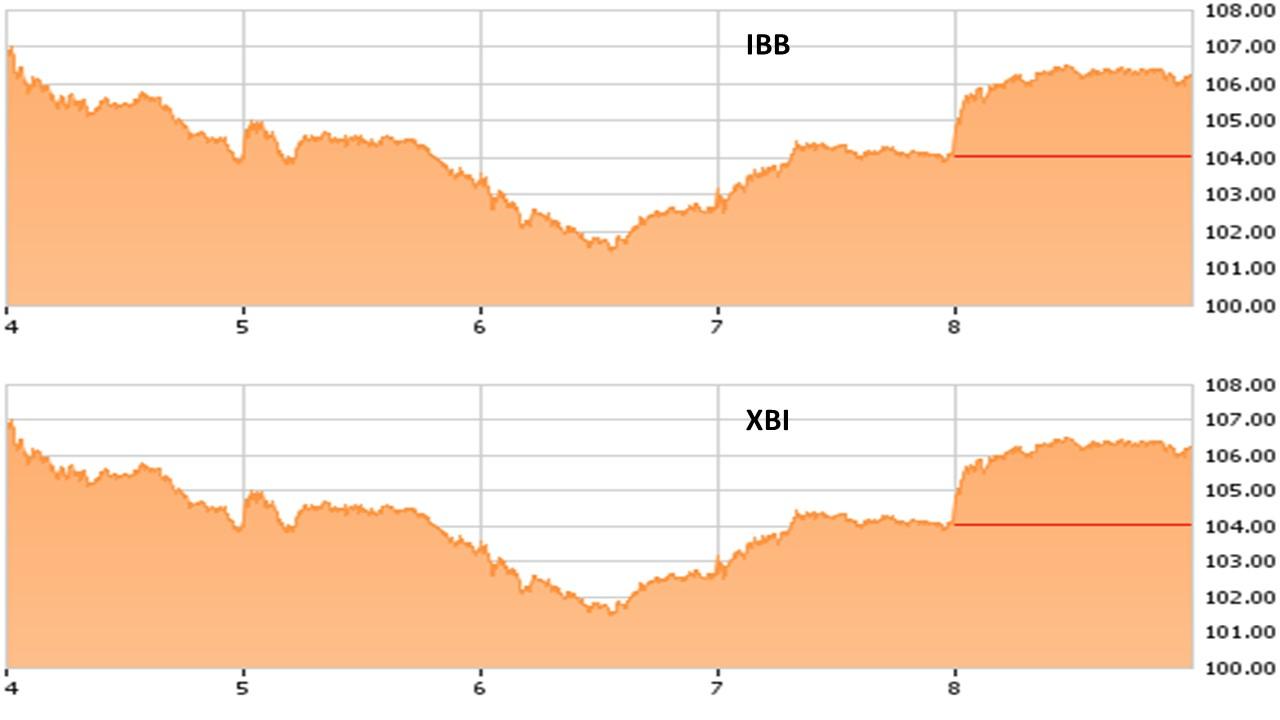

The main biotech indices rose some two percent on Friday to close the week relatively flat. Most of the early part of the week we saw weakness across the biotech sector, especially in many small caps. I think this is combination of tax loss selling, ho hum investment sentiment on the sector at the moment and a continued lack of M&A activity of note. That should change early in 2018, provided the tax reform package gets signed into law.

Author's note: To get these Biotech Forum Daily Digests as soon as they are published, just click here on my profile, hit the big orange "Follow" button, and choose the "real-time alerts" option.

![]()

A big notable winner of last week was Sage Therapeutics (SAGE). The stock more than doubled late in the week after positive results from a Phase II study around its compound SAGE-217 for the treatment of adult patients with moderate-to-severe major depressive disorder were released. The shares have now tripled from the level we first gave it a thumbs up almost exactly one year ago. We hope that many of our followers had that one in their portfolios in what was otherwise a ho-hum week for the sector.

The release positive top-line data from a Phase 2 clinical trial of MGL-3196 in patients with biopsy-proven non-alcoholic steatohepatitis or NASH powered a huge rise in the stock of Madrigal Pharmaceuticals (MDGL) on Wednesday. The mid-stage trial met is primary endpoint. MGL-3196 drove a 36.3% reduction in liver fat compared with 9.6% for patients taking the placebo in the study.

There are no PDUFA dates on the calendar next week. Notable events will be dominated by companies presenting at the 59th ASH Annual Meeting and Exposition in Atlanta that runs from Dec. 9th through the 12th. We covered many of these companies in last weekend's update. However, here are a few additional names to watch that will be presenting at this well-attended event.

Kura Oncology (KURA) presented preliminary Phase II data from its compound Tipifarnib Sunday. It is in trials as a possible treatment for chronic myelomonocytic leukemia.

Alexion Pharmaceuticals (ALXN) will be presenting new Phase I/II data for its compound ALXN1210 to treat Paroxysmal nocturnal hemoglobinuria today. Phase 3 data from another study is due sometime in the second quarter of next year. After the bell Thursday, it was reported that noted activist investor Elliott Management had taken a stake in this mid-cap concern.

GlycoMimetics (GLYC) will also be presenting today. The company is expected to release Phase I/II results for its compound GMI - 1271 for a potential treatment of Acute myeloid leukemia, both newly diagnosed and refractory.

Global Blood Therapeutics (GBT) will release updated data around Phase 2a study for its compound GBT440 to treat Sickle cell disease - children age 6-17 as well.

Spark Therapeutics (ONCE) is presenting additional data from a Phase I/II study for its drug candidate SPK - 8011 to treat Hemophilia A today as well. For a full list of companies presenting at this conference, click here.

![]()

After very little analyst activity throughout 2017, Aquinox Pharmaceuticals (AQXP) is starting to see some positive analyst commentary over the past month. In early October, Cantor Fitzgerald ($28 price target) reissued its Buy rating on the stock. Roughly two weeks later Canaccord Genuity ($22 price target) did the same. Friday, Needham became the third analyst firm to chime in with a Buy ($25 price target) on the stock. The stock currently trades for approximately $10.50 a share.

Oppenheimer reiterated its Outperform rating and $10 price target on Mediwound (MDWD) Friday after recently meeting with management. Oppenheimer's analyst had this to say about the company's prospects:

We met with MDWD management and came away incrementally more positive. We consider MDWD to be relatively de-risked with two validated drugs in development for areas of high unmet medical need. Both NexoBrid and EscharEx are in late stages of development in the US, with the same active ingredient that is already approved in Europe. Both development programs are fully funded to completion. Both NexoBrid and EscharEx offer significant advantages vs. surgical wound debridement in terms of clinical and economic outcomes. Based on demographics and epidemiology, we believe EscharEx may be the larger of the two commercial opportunities relative to NexoBrid.

After a recent pullback, Repligen (RGEN) see some love from Citigroup on Friday. Citi's analyst in this space initiated RGEN as a Buy with a $45 price target. Earlier in the week, JPMorgan also started the name as a Buy with a $42 price target. It was the first analyst activity Repligen has seen in some five months.

Note: New analyst ratings are a great place to begin your due diligence, but nothing substitutes for deeper individual research in this very volatile sector of the market. Many of the small-cap names highlighted in "Analyst Insight" will eventually appear in the "Spotlight" section, where we do deeper dives on this type of promising but speculative small-cap concerns.

![]()

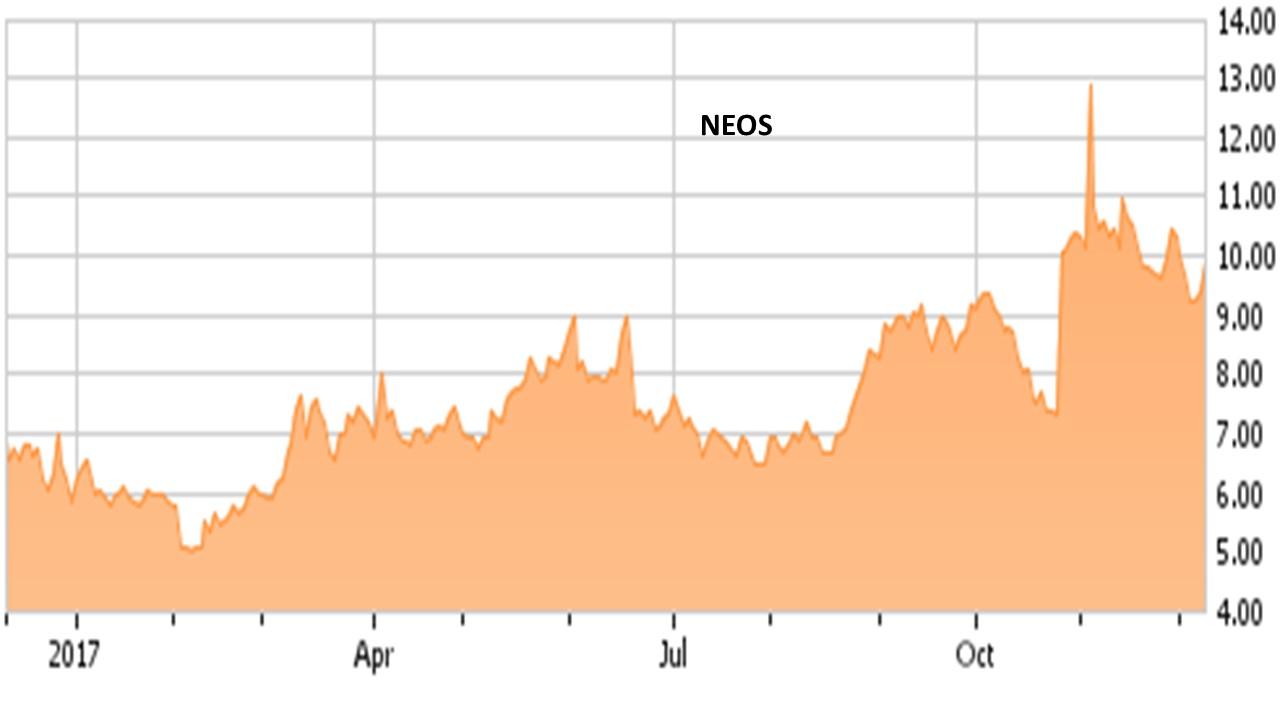

The stock of Neos Therapeutics (NEOS) gained more than five percent on Friday following solid third quarter earnings results. Neos is one of my favorite small biopharma names at the moment. The stock is up some 50% since we called it a must-have small cap stock in March of this year. Let's revisit this name after earnings results and highlight some of the key items within it just released quarterly results in today's Spotlight Feature.

Earnings Highlights

Earnings Highlights

The company posted a loss of 58 cents a share, nearly two dimes a share above the consensus. Revenues came in at $6.7 million for the quarter, slightly above the consensus. Sales increased by over 300% from the same period a year ago.

Adzenys XR-ODT saw scripts grow over 20% sequentially from the second quarter to over 50,000 in the quarter just reported. Almost three quarters of new scripts are coming from individuals on other ADHD drugs.

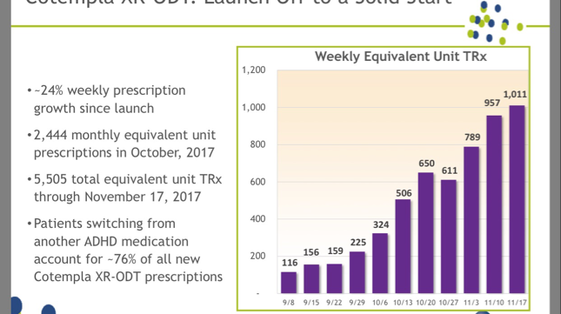

Recently launched Cotempla is also off to a strong start, as can be seen in the chart above. Neos held $66.5 million in cash and cash equivalents and short-term investments at the end of the third quarter.

Outlook

There is a lot to be excited about right now about Neos Therapeutics. The company recently rejected a $10.25 a share buyout bid from PDL Biopharma (PDLI) as the board thought considerably undervalued the company. A highly ranked analyst (TipRanks) at JMP Securities reissued a Buy rating and whopping $30 price target on NEOS one month ago. He noted that "PDL BioPharma's $10.25 per share takeover offer undervalues Neos Therapeutics."

In addition, the company's third approved drug Adzenys ER will hit the market early in 2018, adding another revenue stream. I don't think PDL BioPharma is likely to make a bid in the mid-teens which is the level I think it would take the board to seriously consider an offer. However, I think other suitors like Pfizer (PFE) or Supernus Pharmaceuticals (SUPN) might be enticed to 'kick the tires' if M&A picks up in 2018. The company's three approved products should have peak sales in the $300 million to $400 million which is a small portion of ~$10 billion annual ADHD market.

The only caveat on the stock is there is the possibility the company may need to do a capital raise if it remains a stand alone entity. It has four quarters of cash at its current burn rate, which should come down as sales ramp up. If a secondary offering causes a notable decline in the stock, I will add to my core holdings as I like the longer term risk/reward on this name even at current levels.

"There is more stupidity than hydrogen in the universe, and it has a longer shelf life." - Frank Zappa