A couple of years ago (February 2015) we wrote about a tiny little internet security company called Intrusion (OTCQB:INTZ) and argued for patience. Well, considerably more patience was required but things finally seem to take a positive turn.

At the time we wrote our previous articles, they got a big client for Savant (one of the company's two main products), which looked like a break-through as they beat some impressive competition (Mandiant, which was taken over by FireEye).

Our reasoning was that if they could win one, they were likely to win more, but somehow that never really happened and the shares fell back a lot, as can happen with these small speculative plays:

However, things turned around quite a bit in Q4 last year, when the company had embarked on a strategy to focus on their other security product, TraceCop, which traditionally brought in most revenues. Revenues increased 50% in Q4 y/y on the back of several new orders, from the Q4 PR:

We booked $9.8 million of orders in 2017, which included $4.4 million of orders in the fourth quarter. This compares to $4.8 million of orders in 2016... Our orders pipeline as we entered 2018 included twenty-six customers, fifteen of which were existing customers and eleven new customers. Total bookings in the first quarter included five renewal orders from existing customers.

Their main products are:

- With TraceCop the company collects and analyzes open source data from the Internet and uses this data to locate and identify threats.

- Savant's approach is different from most other security products. It's an "inside-out" approach. Rather than looking at incoming traffic to try to weed out threats, it assumes that the system and/or network is already compromised. So it is looking at outbound traffic for identification of irregularities instead.

TraceCop is mostly a database of worldwide IP addresses, combined with other data. It goes back to the 1990s so it's hard to replicate. It's a tool for identification and location of cybercriminals.

Savant keeps 10 years of company network traffic logs (usual for companies is something in the order of 30 days) which enable companies using Savant to identify which host was infected first and which systems the hackers first established a beachhead on long after it happened. Together with TraceCop its easier to establish rogue traffic.

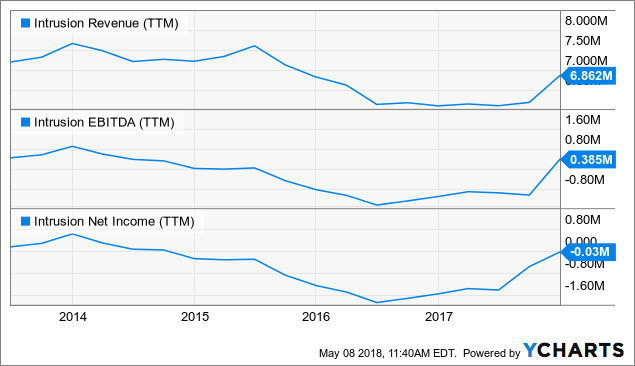

Focusing on TraceCop has paid off considerably, as you can see in the chart above. Such fourfold of the share price from the lows comes on the back of improved financials, and indeed Q4 last year was their first profitable quarter for quite some time (although it has to be said that they were always fairly close to break-even in the past).

The chart doesn't yet include the Q1 figures which continued the improvement, but the Q4 trend change is clear. What we can say after the presentation of Q1 figures is that the turn-around is getting legs:

- Revenues accelerated dramatically and increased by a whopping 43.8% y/y.

- Net income was 78% higher sequentially to $346K.

- Gross profit margin was 62%, down a point from last year's quarter.

- Operating expenses actually declined, from $1.3M in to $1M now, as a result of shifting R&D expenses to cost of sales.

Perhaps the best news is that management argued that there are two large orders at the point of signing, after months of what seems to be bureaucratic procedures involving a Federal agency (Department of Defense) opting for a procurement bureau. Here is what management said on the Q1CC:

We've been watching too large orders work their way through procurement for months and have indications that these will soon turn to purchase orders. The most important one I'm tracking is over twice the size of our previous largest order and represents a new class of opportunities for us...

As it happens, the company gets most of their business from Government, from the 2017 10-K:

Sales to U.S. government customers accounted for 81.6% of our revenues for the year ended December 31, 2017, compared to 69.3% of our revenue in 2016. We expect to continue to derive a substantial portion of our revenues from sales to governmental entities in the future as we continue to market our entity identification products and data mining products to the government.

It seems as otherwise things are also looking up as the company (Q1CC):

Our orders pipeline as we entered 2018 included 26 customers, 15 of which were existing customers and 11 were new customers.

However, bookings were only $850K and that includes renewals from existing customers, so it seems that Q2 will depend on closing at least one of these big deals for maintaining the momentum from Q4 last year and this Q1. At least one of these deals, luckily the biggest one, seems a done deal (Q1CC):

as I understand the funds have been transferred to a procurement group and all the paperwork will be done at the end of this week so they can start the procurement with us so historically that's about a three week cycle from the end of this week so that's my best guess at this point but it's been months of waiting.

Although bookings were low this quarter, the pipeline might not be all that empty (Q1CC):

There are a few new opportunities which has surfaced this quarter, this last quarter with potential new customers solely based on relationships that have grown out of our two newest contracts we still have some business development work to do for turning these opportunities in orders in late 2018 and early 2019.

Management is also hoping to turn some of their new TraceCop customers into buying Savant. If they can do that, it will be a home-run.

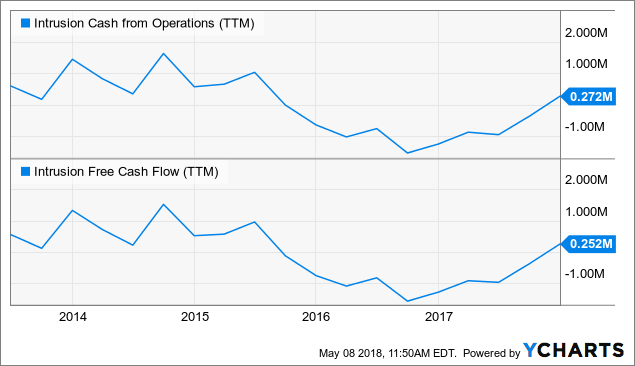

Cash

Again, the latest quarter isn't included and there isn't yet a quarterly filing to gauge cash flow. But given the improvement in revenue and especially earnings in Q1, the positive trend has, in all likelihood, continued.

Here is the picture for last year, from the 10-K:

Net cash provided by operations for the twelve months ended December 31, 2017, was $272 thousand due to the following sources of cash and non-cash items: a $291 thousand increase in accounts payable and accrued expenses, a $30 thousand decrease in inventories, an $11 thousand increase in deferred revenue, $69 thousand in depreciation expense, $137 thousand in amortization expense of capital leases and other assets, $18 thousand in stockbased compensation, and $33 thousand in waived penalties on dividends. This was partially offset by a net operating loss of $30 thousand (The net loss in 2017 included other income of 928,000, of which $872,000 came from the sale of certain unused IP addresses and $56,000 from the sale of an investment.), a $217 thousand increase in accounts receivable, $56 thousand gain on sale of investment, and a $14 thousand increase in prepaid expenses and other assets

So keep in mind that the positive cash flow last year was mostly due to an increase in accounts payable and accrued expenses.

Debt

Investors should also note this, from the 10-K filing:

On March 25, 2004, we completed a $5,000,000 private placement pursuant to which we issued 1,000,000 shares of our 5% Convertible Preferred Stock (the “Series 1 Preferred Stock”) and warrants to acquire 556,619 shares of our common stock. The conversion price for the Series 1 Preferred Stock is $3.144 per share. As of February 28, 2018, there were 200,000 shares of the Series 1 Preferred Stock outstanding, representing approximately 318,065 shares of common stock upon conversion.

On March 28, 2005, we completed a $2,663,000 private placement pursuant to which we issued 1,065,200 shares of our Series 2 5% Convertible Preferred Stock (the “Series 2 Preferred Stock”) and warrants to acquire 532,600 shares of our common stock. The conversion price for the Series 2 Preferred Stock is $2.50 per share. As of February 28, 2018, there were 460,000 shares of the Series 2 Preferred Stock outstanding, representing 460,000 shares of common stock upon conversion.

On December 2, 2005, we completed a $1,230,843 private placement pursuant to which we issued 564,607 shares of our Series 3 5% preferred stock (the “Series 3 Preferred Stock”) and warrants to acquire 282,306 shares of our common stock. The conversion price for the Series 3 Preferred Stock is $2.18 per share. As of February 28, 2018, there were 289,377 shares of Series 3 Preferred Stock outstanding, representing 289,377 shares of common stock upon conversion.

The interest cost (dividends on the preferred stock) and dilution aren't severe, the dividend on the preferred stock amounted to $210K or 3% of revenues last year. However, in relation to earnings this is still rather substantial.

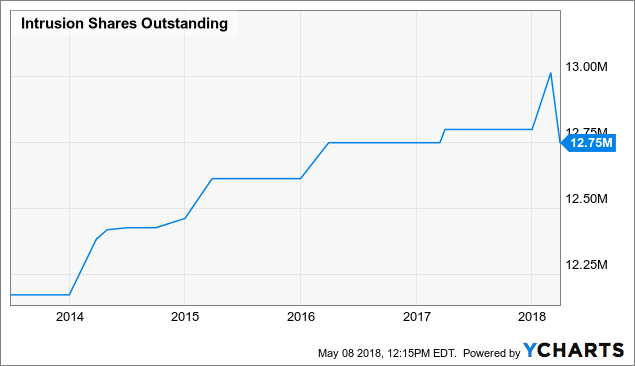

Dilution has been rather moderate the last 5 years.

One off benefit

Another thing we found in the 2017 10-K is a rather substantial one-off benefit:

On July 7, 2017, the Company entered into a sale of certain IP addresses that were not currently being used in the Company's business operations and were not required for the Company's future business plans. The net proceeds from the sale of these intellectual property assets were in the amount of $872,000 which the Company received on August 9, 2017. In addition, $56,000 was received on August 3, 2017, from the sale of an investment.

Valuation

The market cap is $13M and the company has $3M in debt so the enterprise value is $16M. Sales last year were $6.9M although the company booked considerably more orders ($9.7M).

So based on this, the EV/S multiple is a little over 2 but if the booked orders materialize that could come down quite a bit.

Q1 produced a nice profit at $346K, which suggests they could do over $1M in profits this year, perhaps even towards $1.5M.

This means the shares aren't all that expensive, but nevertheless they are only for those who can tolerate the risk as it's still very uncertain what kind of numbers they will hit this year.

Conclusion

This is still a small speculative play but focusing on TraceCop has paid off as the company has gained orders and momentum, and there are some serious deals apparently at the point of completion and the company has moved to profitability.

If you can tolerate the risk, we think a small position is warranted. The company is clearly gaining traction, and by doing that future orders will be easier, not harder.

We think that the small scale of the company would scare a lot of potential customers, so the more and the bigger orders they score, the less this will be a problem for prospective customers.

Then there is the opportunity with Savant, selling to existing customers which requires little effort.

But one has to keep in mind there are no guarantees here, the orders could dry up and Savant might never really gain significant traction. For less risk tolerant investors we would advise to wait out at least a couple of quarters to see whether the present is a fortunate blip or really a new trend.

Given that the company is already profitable, if it is the latter the upside in the shares is also considerable.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.