Introduction

AVEO Pharmaceuticals (AVEO) is a small-cap biotechnology company focused on developing its lead product tivozanib (Fotivda®), an oral inhibitor of VEGF receptor 1, 2, and 3 tyrosine kinases for the treatment of metastatic renal cell carcinoma (mRCC). Tivozanib is approved for first-line RCC in the EU since August of 2017. This product is sub-licensed out to EUSA Pharma. Despite being approved in the EU, the FDA denied AVEO's application for approval in the United States. Now, in an attempt to prove the efficacy, AVEO is studying tivozanib in the third-line setting. Additionally, AVEO is studying tivozanib in combination with Bristol-Myers Squibb's (BMY) workhorse nivolumab (Opdivo®). With readouts from both trials scheduled in the coming weeks, here I will outline each trial and the fundamentals of AVEO, underscoring why these results could be a make or break situation for the company and investors.

Tivozanib plus Nivolumab - Background

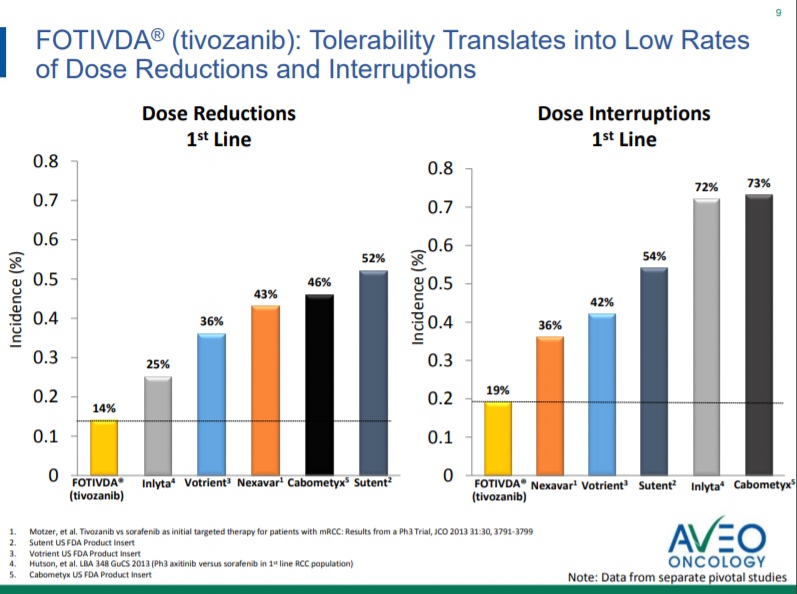

This trial, coined TiNivo by AVEO, is evaluating the combination of tivozanib and nivolumab in patients who are both treatment naïve and previously treated patients with mRCC. While this is not the only combination of PD-1 agents and VEGF agents being investigated, AVEO makes the case that tivozanib's superior selectivity allows for decreased side effects and the ability to use full doses of both tivozanib and nivolumab. From the TIVO-1 trial, tivozanib in the first-line setting, tivozanib treatment has a dose reductions and interruptions at a rate of 14% and 19% respectively. For comparison, dose reduction and interruption rates of other agents are presented in Figure 1. While this bodes well for the tolerability of, efficacy is still essential. Initial data from the TiNivo trial was presented earlier in 2018 at ASCO GU. Now, AVEO will present updated interim data from the TiNivo trial at ESMO Congress on October 22, 2018.

Figure 1. Tolerability (from October Corporate Presentation).

TiNivo Initial Data from ASCO GU and ESMO Update

From the ASCO GU poster presentation, we see the initial safety data on all 27 patients and efficacy data on 14 patients. The full dose of tivozanib (1.5 mg daily) was tolerated in combination with full dose nivolumab (240 mg q2 weeks). The patients recruited in TiNivo were split with patients previously treated and untreated. The rates of grade 3/4 adverse events were 52%, and the rate of grade 3/4 events related to study drug was 44%. Efficacy data was presented on 14 patients at the recommended phase 2 dose who had two or more treatment scans. The results were encouraging for these 14 patients, with 9 patients (64.3%) having a partial response. There were no complete responses, but there were also no patients with progressive disease. While the abstract for ESMO Congress has been released, there was no new data included, instead, "Final efficacy and safety data on all 28 patients will be available at the meeting."

Other ESMO Updates and the Competition

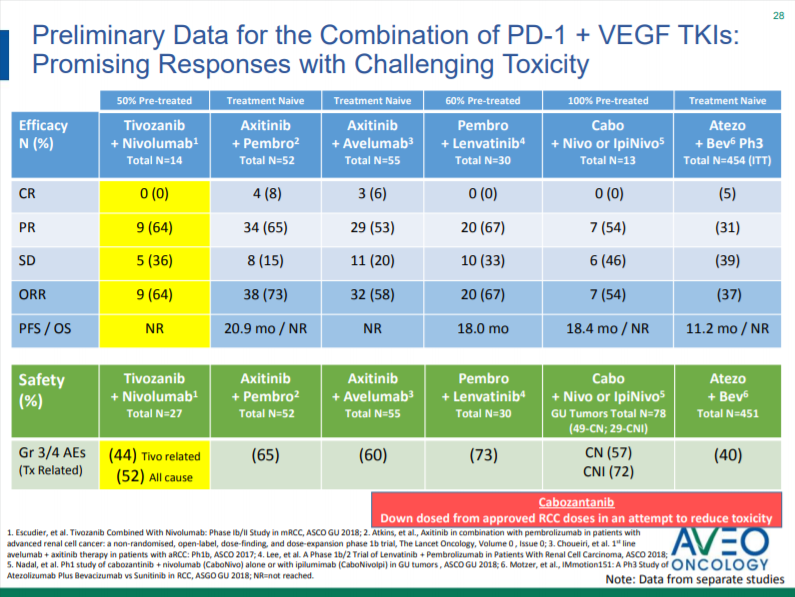

As AVEO has presented, the initial data from TiNivo has shown similar efficacy relative to its competitors (Figure 2). From the data presented, TiNivo had the lowest rate of grade 3/4 events apart from atezolizumab and bevacizumab (52% versus 40% respectively). While atezolizumab and bevacizumab may have a lower rate of grade 3/4 adverse events, this was at the expense of efficacy in the phase 3 trial in treatment naïve patients, with only a 37% ORR. So far, the best ORR have been from axitinib with pembrolizumab and levantinib with pembrolizumab: ORRs of 73% and 67% respectively. While the lead in data from TiNivo did not show any complete responses, CRs were noted in the axitinib with pembrolizumab and axitinib with avelumab group, however, one must consider these studied treatment naïve patients, and there has only been a limited amount of data on treatment naïve patients presented yet from the TiNivo study. If TiNivo can elicit similar safety and efficacy data in both treatment naïve and previously treated patients, that will bode well for the combination. It is important to note that Bristol-Myers Squibb is running a Phase 3 trial of cabozantinib in combination with nivolumab in the first line setting of mRCC (CHECKMATE-9ER), however, this still leaves the door open for previously treated patients.

Figure 2. Combination of PD-1 agents and VEGF Agents (from October Corporate Presentation).

While the TiNivo update on the additional 14 patients will be important for AVEO, ESMO congress is also the venue for Exelixis (EXEL) to reveal initial ORR data on their COSMIC-021 trial of cabozantinib in combination with atezolizumab for treatment naïve patients with mRCC. Cabozantinib is approved for mRCC at a maximum dose of 60mg daily (an approved lower monotherapy dose to help manage AEs), lower than the maximum approved monotherapy dose. Now whether this lower dose makes a large difference is a matter of opinion, but AVEO seems to think that the fact they can use a full dose of tivozanib in TiNivo is an advantage. Exelixis included data in their abstract, and from what is revealed in this treatment naïve cohort is and ORR of 50% with a single CR and 4 PR. Of note, two additional patients had unconfirmed PRs. This is new data not included in Figure 2, and competition is always something to keep an eye on, as it is hard to make comparisons until we see the updated TiNivo numbers on October 22nd, which is the first catalyst for this company. What is clear, however, is that this is an extremely crowded and competitive environment that AVEO is playing in.

TiNivo Funding and Financials

From AVEO's most recent quarterly filing, AVEO estimated the cost of the TiNivo trial being $4.0 to $4.5 million. Bristol-Myers Squibb is supplying nivolumab for the trial, and EUSA has opted-in for the co-development of TiNivo, but has already paid its cap of $2.0 million for the shared trial costs. Regarding remaining costs, AVEO estimates there are around $1.0 to $1.2 million in expenses left for the TiNivo trial through 2019, which appear to the sole responsibility of AVEO. The research and development reimbursement and cost sharing from EUSA was not subject to the sublicense fee to Kyowa Hakko Kirin (KHK), while any royalties and milestones generated from the future marketing of the TiNivo combination in EUSA's regions would be subject to the 30% sublicense revenue obligation to KHK.

TIVO-3 Trial Background

The trial evaluating tivozanib in the mRCC third-line setting has been coined TIVO-3. The TIVO-3 trial has recruited 351 patients to compare tivozanib to sorafenib. The primary endpoint is progression-free survival, which the company plans to use to support a marketing application for the third line setting in the EU and then for an application for the First and Third line setting in the United States in combination with TIVO-1 data.

After several delays in releasing the data, on October 1st, AVEO announced the TIVO-3 Steering Committee recommended that the topline analysis be initiated. The cutoff for progression-free survival was October 4th. The company expects this analysis to take approximately six weeks. These timelines suggest the results could be expected around or during the week of November 12th.

Doing the primary analysis early results in the analysis of fewer events. The company noted that if the event total was 242, as it was as of September 26th, instead of the planned 255 events, then the power of the study would be reduced from 90% to 88%. While the "industry standard" power is 80%, TIVO-3 is still powered greater than this value. Under the new calculation of 88% power, if no difference in progression-free survival is found, there is a 12% chance this is a false-negative due to chance, as opposed to the original calculation that would be 10%. This change places a slightly increased risk that if no difference is found, that it is due to chance, however only 2% is not particularly worrisome. Furthermore, this is under the assumption of 242, if any additional events have happened between September 26th and October 4th, then that will only help AVEO in this situation.

TIVO-3 Funding and Financials

From AVEO's most recent quarterly filing, AVEO estimated the overall cost of the TIVO-3 trial to be roughly $45.0 to $48.0 million. They are estimating that the remaining costs of the TIVO-3 trial are in the $6.0 to $9.0 million range through 2019. As tivozanib is sub-licensed to EUSA in Europe, Latin America, Africa, and Australasia, EUSA may opt-in to the TIVO-3 trial in the form of a $20 million reimbursement payment representative of half the cost of the trial. This research and development reimbursement from EUSA is not subject to the sublicense fee to KHK, while any royalties and milestones generated from the expanded indication in EUSA's regions would be subject to the 30% sublicense revenue obligation to KHK.

Fundamentals

AVEO reported ending the second quarter of 2018 with $18.1 million in cash, cash equivalents, and marketable securities. Revenue for the second quarter was approximately $400,000. Of this value, $97,000 was from tivozanib royalties, which represents a growth from the $46,000 in royalties reported in the first quarter. One must not forget, however, that tivozanib royalties are subject to a 30% sublicense fee payable to KHK. The net income for the second quarter was $4.0 million, however, approximately $11.1 million of the second quarter net income was due to a non-cash gain attributable to the decrease in the fair value of the 2016 private placement warrant liability that principally resulted from the decrease in the stock price that occurred within the quarter. Expenses during the second quarter included $4.9 million in research and development expenses and $2.8 million in general and administrative expenses. The company guidance at the end of quarter included enough cash to fund operations into the first quarter of 2019. That being said, this estimate assumes no reception of milestones, no new partnerships, or no additional equity or debt financing.

Since that filing, however, the company has bolstered their balance sheet with a small amount of cash. This includes a $2.0 million milestone payment from CANbridge for the IND approval of CAN017 (formerly AV-203). Additionally, in August company raised $5.7 million through a public offering. Outside of this known $7.7 million cash infusion, there is the low double-digit to mid-twenties royalties on tivozanib that will be due to AVEO, less the 30% fee to KHK. Additional milestones include $8 million for EU reimbursement approvals in France, Germany, Italy, and Spain, less the 30% fee to KHK and the $20 million research and development reimbursement from EUSA for TIVO-3 which will not be subject to the 30% KHK fee.

Interpretation and Thoughts

While every investor may interpret these developments differently, I find the next couple weeks to be essential for AVEO's future. The fact that the company completed only a small secondary offering in August seems to signal management's confidence in both the TiNivo program, but more importantly, the results of TIVO-3, and here is why. Normally, if a company raises capital before a major inflection point, I would expect it to be a significant amount, enough for them to continue operations for a significant amount of time in the case of negative results. A capital raise after poor results at a lower share price would significantly destroy share value. The August capital raise of $5.7 million is roughly a quarter worth of cash, not as sizeable as I would expect. Management also knows that positive results can result in a $20 million payment from EUSA, a payment that is not subject to the 30% KHK fee, which would substantially bolster the balance sheet.

The company has also disclosed that they are actively seeking partnerships for their AV-353 pulmonary hypertension candidate, which would also help the balance sheet. These are a few of the potential avenues that AVEO could use to bolster its balance sheet. With that being said, there are a lot of things that need to go right for AVEO. I would imagine that positive TIVO-3 data would result in the share price increasing and subsequently another offering at a higher share price, likely a more sizable raise than the August secondary.

What is most important to AVEO, its success in TIVO-3. A positive readout from TIVO-3, combined with TIVO-1 data will support an application to the FDA for use of tivozanib in the first and third line setting. This is the region that AVEO retains the rights to tivozanib and would be able to enjoy the revenue from, less the required low to mid-teen tiered royalties on sales to KHK. This is much more substantial than receiving only royalties from EUSA and paying a portion of the royalties to KHK. AVEO would also have to pay an $18 million milestone if tivozanib is approved in the United States.

From the current viewpoint, it is clear to see without sales in the United States, AVEO will be unable to sustain itself on the EUSA royalties alone. Should TIVO-3 not report positive data, I would see a painful secondary offering in the future of AVEO, negatively impacting the share price. This would leave AVEO dependent upon EUSA to commercialize and promote tivozanib for some source of royalty revenue. AVEO would also then likely become dependent on the rest of its pipeline for potential future revenues outside of the highly competitive MRCC VEGF plus checkpoint inhibitor market which its TiNivo trial is in.

Figure 3. Tivozanib Timeline (from October Corporate Presentation).

Conclusion

It is clear to see that AVEO is entering a very important inflection point for the company, first with the TiNivo data and more importantly, with the release of TIVO-3 data. The dates to watch for AVEO include October 22nd, when the updated Phase2 TiNivo data is presented. The second catalyst to watch for is the TIVO-3 results, which can be estimated to be released around the second week of November (week of November 12th). A complete list of proposed tivozanib catalysts are presented in figure 3 above. While Exelixis is already in a Phase 3 trial with cabozantinib plus nivolumab, this is in treatment naïve patients. If TiNivo reports good data in previously treated patients, this would be an advantage for AVEO. AVEO desperately needs positive TIVO-3 data if they have any hopes of removing their dependence from EUSA royalties and getting tivozanib approved in the United States. In general, this appears to be the making of a high risk, high reward situation, and investors should treat it as such.