Cronos Group (NASDAQ:CRON) is set to release their earnings on Tuesday, November 13th - along with three other major players in the industry. Because of the newness of the cannabis industry, valuations of the various companies are misaligned from fundamentals and differentiate wildly. Some stocks are perceived as grossly undervalued to their peers whereas valuations for other's harken the call of irrational exuberance. Cronos Group fits somewhere in that category. Because of the disparity in belief, this presents an opportunity when it comes to earnings releases; the news tends to induce a heavy dose of volatility. With Cronos' earnings on Tuesday, the potential for their stock to move substantially exists. However, with pot stocks you can never be too sure if the market will swing upward or drop like a rock, regardless of results. I am going to bring some sensibility to the valuation of Cronos and then try and determine what their earnings release will do with the stock. And, I am going to line up a trade based upon this analysis while encompassing the possible volatility.

Here is a look at Cronos' daily stock chart:

If you look at the chart for August 14th, you will see the date of the last earnings release for the company. On that date,

Cronos reported earnings of $0.05 (TTM) on revenue of $6.4 million. The stock was printing $5.69 pre-release and doubled in less than two weeks; the stock had a short-term peak of $12.87 after 17 days before finally easing back.My thinking on Tuesday's release is that there is going to be some balance between this earnings release and the future guidance. Over the past few weeks, Canada has been fully legalized for adult-use cannabis. No sales from this will appear in the earnings we are about to see. However, the company may likely provide guidance based upon what sales have been like. The quarter finalized at the end of September. Canada legalized cannabis nationwide in mid October. If there is good news to be said from the initial sales from this, the future guidance is an opportunity to mention that.

The company and what they are working towards

Cronos has a valuation of $1.53 billion. It is difficult to get a steady read on the company's earnings because they have a few one-offs that have made the company profitable in some of the past few quarters. However, this quarter the expectation is that the company takes a loss on earnings despite higher revenue:

| Revenue | 6/30/2018 | 3/31/2018 | 12/31/2017 | 9/30/2017 |

| Total Revenue | 3,394 | 2,945 | -1,156.931 | 2,388.543 |

| Cost of Revenue | -2,952 | 1,017 | -1,458.698 | -690.213 |

| Gross Profit | 6,346 | 1,928 | 301.767 | 3,078.756 |

The company reported in their latest earnings conference call that the revenue increased from $3 million versus $0.6 million the previous year, same quarter; an increase of 428%. The company also sold more kilograms than expected for the quarter resulting in a decline in cost of revenue.

Here are the longterm numbers I am focused on for Cronos: In the quarter ending in June of this year, Cronos had some $577,000 profits on $3,394,000 revenue for 17% profit margin (CAD$765,000 profits on CAD$3.9 million revenue). The company sold 1,145 kilograms at a cost of $1.24 per gram ($1.64 CAD).

These are important numbers for determining the company's value. The company is expected to be able to produce some 110,500 kg. per year based upon there building projects and supplier contracts. At a price of $7.21 USD per gram, that would amount to revenue of $796.7 million per year. On that revenue, with 17% profit margin, the company can expect to earn $135.5 million. With 177 million shares outstanding, EPS would be $0.76. If we valued the company along the lines of the general market at 20-times these earnings, that puts each share worth $15.00. Currently, the stock is trading at about $8.35, about half of its possibility.

To be sure about the valuation, going back to the Cronos earnings transcript, the company states that they "have enough demand for the capacity that we're currently building". That build would be the 110k kg. per annum. So, these valuations should hold and the company should achieve those levels of sales. When? The company does not give any kind of sense. But, my expectation is within a few years' time.

As mentioned, most see earnings for this quarter coming in negative. But, can the company increase revenue as they have been doing, establishing their brand? And, can they contain their earnings loss despite it being negative? Increasing revenue would be a major plus for this release, and this would be on trend for the past few quarters. Declining negative earnings would also be a plus. This is what I, and the market, are going to be digging through on Tuesday morning (8:30 New York Time).

Or, does the company fall flat? This is a consideration that needs to take place. Cronos is still developing their brand. Cannabis is just newly legalized and so individuals have not developed their "favorite" brand just yet. Cronos does state in their previous earnings release that they are continuing to establish their brand in the medical arena. But, all eyes are now turning to rec use.

And, then there are the supply issues: Canada keeps running out of supply. I can't recount how many company articles I have read over the past several months where companies have provided guidance of their gearing-up for the adult-use legalization. And, yet the country is undersupplied. Cronos shipped some 100 kg. in September. But, the product is sold out in Ontario, although some is still available in British Colombia.

On the one hand, selling out of your product is a good thing for revenues. On the other hand, I can't believe any company ran out of supply anywhere. This is a perfect opportunity for a company to put their stock on shelves and get consumers to commit to their brand.

At the current moment, my focus for Cronos is this earnings release and the subsequent earnings conference call. I expect there to be continued growth in their medical use area of business. And, I want to see the company making strides to reign in negative earnings. But, the real meat-and-potatoes for me is the volatility that will happen because of this earnings release. Since cannabis is so new, my real expectation is the volatility; I am putting a trade together based upon this. In the very near future, once we get a better grasp of the company's developing fundamentals, I will switch my thinking towards owning this company outright; I like the idea that the company's stock should be double the price.

The Trade & Downside Risks

Things are going to be interesting this week. But, I cannot be certain which direction the stocks are likely to move. Given that, I am putting on a trade that allows for either direction to happen.

I am an options trader at my core. And, an options trade is the way to go with this earnings release. I am going to put on a delta-neutral trade buying the stock and buying puts with a 1:2 ratio, respectively. This way, if the market moves up sharply, my long stock stock will be profitable, however, I lose on my options. I need a move of $1.60 in either direction.

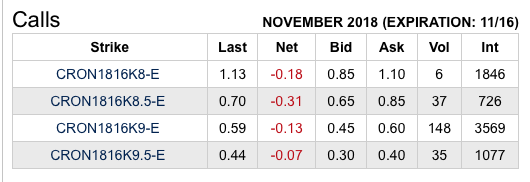

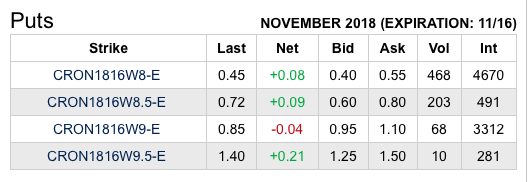

Here is a look at CBOE prices for both call and put options on (CRON):

I am long the 8.50 puts at a cost of $0.80; my breakeven is a move of $1.60 either up or down from the current price within 3 days' time.

I am long the 8.50 puts at a cost of $0.80; my breakeven is a move of $1.60 either up or down from the current price within 3 days' time.

The only way the trade does not work out is if the stocks do not move at all. Considering that all four of the biggest participants in the industry are releasing their earnings on both Monday and Tuesday, I find a move of <$1.60 in the allotted time as being a low probability event, but it certainly could happen. If it does, I lose out on the cost of my puts.

Important disclosures

As my readers know, I have homes in both Colorado and California - and have seen the legalization process occur in these states. However, I am currently living in Mexico. Because of my viewpoint, I have been an active participant in the cannabis scene with investing and trading. I own some cannabis stocks and expect to own them for many years to come. I have shorted other companies but will be looking to purchase some of those companies in the near future. This week is going to be huge for the industry, I believe, and I expect I will be very active.

There are several cannabis companies releasing earnings on Monday and Tuesday, including Canopy Growth (CGC), Tilray (TLRY) and Aurora Cannabis (ACB). Along with Cronos, these are some of the biggest cannabis companies in Canada. I expect a great deal of volatility from the respective earnings releases. I expect differentiation between the various companies and their results this quarter. That will make things interesting.

I am expecting a tremendous amount of volatility from Tilray and their earnings release. I have shorted the stock several times and have done well, but this time I am trading the stock with an abundance of caution. I have a very similar trade on with Tilray as I do with Cronos; you can read about that stock here: Tilray: Should You Buy Or Sell Before The Earnings Report

I am looking to go long Canopy Growth after having been short from $55 all the way down to $34. I felt Canopy Growth's stock was substantially overvalued and the short postintion worked out well. Now, however, I want to own the stock at these lower levels and am hopeful that some price swings this will will afford me that opportunity; you can read about that here: Canopy Growth: After The Pot Stock Sell-Off, A Better Price To Buy

I am long Aurora and hope to hold this stock for many years to come. I have buy orders below current market prices; you may read about that idea here: Aurora Cannabis Poised For Long-Term Growth With Acquisitions

Conclusion

This week will see lots of volatility. Cronos' stock is likely to move significantly. However, I am not about to say I know what direction, although I am leaning towards a price move upwards. The fundamentals of Cronos are that the company will make their niche within the industry. For right now, this week is likely to see a significant amount of volatility with stock prices in the industry. I am gearing up for that.

Since I cannot be certain about which direction of the stock I am putting on a delta-neutral position with leanings towards the stock heading higher. But, I do expect a significant amount of volatility. I feel this is the most sane way of taking advantage of potential insane price swings.

Afterwards, I am going to take a serious look at owning this company for the long haul.