Marathon Petroleum Corporation (NYSE:MPC) owns 21%, or one million barrels per day (BPD), of Mid-Continent and Rockies refining capacity. While its operations remain steady as it integrates Andeavor, it's experiencing both seasonal winter product decline and the pressure of lower stock market momentum. So although the company benefits more than ever from discounted crudes, it also offers a heightened dividend yield of 3.2% at its current stock price.

Brief Company Summary

Marathon Petroleum is based in Findlay, Ohio, and employs about 44,000 people full time.

With a Dec. 26, 2018, closing stock price of $58.35/share, its market capitalization is $40.3 billion. The company has a total of 3 million BPD of refining capacity in sixteen U.S. refineries.

The company divides into three segments: Refining, midstream, and retail marketing. Much of its midstream is contained in two separately-traded limited partnerships. It sells petroleum products to wholesale customers, to the Speedway business segment, and to independent retailers operating 11,000 outlets, including Marathon, Arco, and several other brands.

With the acquisition of Andeavor, Marathon Petroleum now has controlling interest in two midstream partnerships: MPLX LP (MPLX) plus Andeavor Logistics (ANDX). Both limited partnerships continue to trade separately from MPC stock.

Oil Prices and Differentials

West Texas Intermediate-Cushing Oil Price, $/barrel

Left axis: $/bbl, credit: market.businessinsider.com

The Dec. 26 closing oil price was $46.94 per barrel for West Texas Intermediate (WTI) crude oil at Cushing. While this is an increase of 10% in one day, as the chart shows the level is dramatically lower than early October prices that reached more than $75/barrel. Lower oil prices are a boon for MPC.

Since not all oil is the same, and Marathon benefits from localized factors, a description of differentials is useful:

*The Brent price is the non-US light crude price and closed today at $54.06/bbl, or about +$7/barrel higher than WTI-Cushing.

*WTI-Midland is the same crude, but at the transport-constrained location of Midland, Texas. For January 2019 WTI-Midland oil trades -$5.70/bbl less than at Cushing, or at $41/barrel.

*Bakken, or Clearbrook, has the same density and sulfur quality as those above, but is produced in North Dakota crude and traded at the Clearbrook, Minnesota hub. Its differential varies depending pipeline availability in North Dakota and Canada. Currently Bakken crude is -$1.75-$4.75/barrel lower than WTI-Cushing, so about $42-$45/barrel.

*(WCS) is Western Canadian Select, used in Canada, but also exported to the U.S. Due to transportation constraints even more severe than in the Permian, the WCS price is -$20/barrel less than WTI-Cushing, or $27/bbl. The differential has been as much as $52/barrel.

Given these large differentials, it's advantageous for Marathon Petroleum to have good access to Bakken and WCS for its 10 inland refineries.

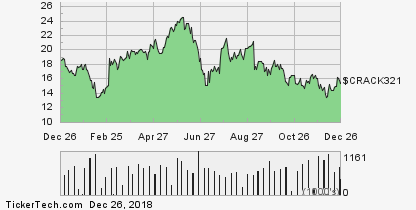

The Crack Spread and Refining Profitability

The trend in the 3-2-1 crack spread, a measure of refining profitability, is shown below and is currently about $15.50/barrel. However, while this number is defined as three barrels of crude subtracted from the sum of two barrels of gasoline and one of distillate, the specific crude used for this calculation is WTI-Cushing. Companies like Marathon that can use less expensive crude as feedstocks will net larger profitability.

Credit: energystockchannel.com

Since winter is an off-season for petroleum product demand, seasonal slumps in earnings and prices, let alone the entire stock market downdraft, make refiner stocks like Marathon Petroleum more of a bargain than in the summer high season.

Competitors

The barriers to the US refining industry remain high due to siting issues, the large, fixed cost of capital assets, a domestic market that's not increasing, and a regulated, consumer-facing gasoline business that's highly competitive and much scrutinized. All of Marathon Petroleum’s three MMBPD of refining capacity is domestic. Valero (VLO), its neck-and-neck competitor, has 3.1 MMBPD of capacity, but with a refinery in Wales and one in Canada Valero’s domestic capacity is 2.625 MMBPD.

Total U.S. refining capacity is 18.6 MMBPD, so Marathon Petroleum’s share is 16% to Valero’s 14%.

In the MidContinent and Rockies, Marathon Petroleum’s major competitors include BP (BP), HollyFrontier (HFC), Phillips 66 (PSX), and Valero. On the Gulf Coast, Marathon’s competitors are virtually every U.S. refiner, since most own at minimum one Gulf Coast refinery.

Marathon Petroleum’s Oil Refineries and Operations

With the acquisition of Andeavor, Marathon Petroleum operates 16 refineries having a total capacity of 3 million BPD. Ten of these refineries are inland. The remaining six include two large 550,000-plus BPD refineries in Texas and Louisiana, one refinery in Alaska, refineries in northern and southern California, and a refinery in Washington state. Marathon’s coastal refineries in Louisiana and Texas also are able to receive waterborne crude from around the world.

Garyville, Louisiana refinery, Credit: marathonpetroleum.com

Growth Prospects

In third quarter news the company explained it's starting to consider combination synergies for ANDX and MPLX. And in the December 2018 investor-day presentation, Marathon Petroleum said it could raise gross run-rate synergy potential by up to 40% to $1.4 billion.

In terms of diversification, the company's executives explain that non-refining segments contribute more than 50% of EBITDA. Thus, they are not totally reliant on refining margins, aka crack spreads.

For 2019, the company plans $2.8 billion of capital spending yet expects to return more than 50% of discretionary cash flow to investors, implying share repurchases of $2.5 billion.

Marathon Petroleum’s Financial and Stock Highlights

Marathon Petroleum’s market capitalization is $40.3 billion at a Dec. 26, 2018, stock closing price of $58.35 per share.

The company's trailing twelve months’ earnings per share is $8.12, giving it a 5.3% return on assets, a 22.2% return on equity and a bargain trailing price-earnings ratio of 7.2. The average of analysts’ estimated earnings per share (EPS) for 2019 the next 12 months are $7.64, a decrease of 6%.

Marathon's third quarter 2018 net income was $941 million, with net income attributable to MPC of $737 million or on a diluted per share basis $1.62. Nine months’ net income is $2.4 billion, with $1.8 billion attributable to MPC.

The table below shows operational income by segment, in millions. In early 2018, some assets were contributed from the refining and marketing segment to the midstream segment and $230 million of income is reflected in the midstream rather than the refining and marketing segment, where it would have been in 2017.

The remainder of the drop in quarterly refining and marketing results were due to lower crack spreads, partially offset by wider U.S. and Canadian crude differentials.

3Q18 | 3Q17 | 9M18 | 9M17 | |

Refining & Marketing | 666 | 1097 | 1558 | 1589 |

Speedway | 161 | 208 | 415 | 581 |

Midstream | 679 | 355 | 1863 | 996 |

At Sept. 30, 2018, the company had $33 billion in liabilities and $53 billion in assets, giving Marathon Petroleum a liability-to-asset ratio of 62%. Its ratio of current assets divided by current liabilities is 1.65, comfortably above the desirable minimum of 1.0 and thus a positive.

Its most recently reported operating cash flow was $6.2 billion and its levered free cash flow is $2 billion. With an enterprise value (EV) of $58 billion, its EV/EBITDA ratio is 9.1, so below the preferred ratio of 10 or less.

Marathon Petroleum’s 52-week price range is $54.29-$88.45 per share, so the Dec. 26, 2018 closing price of $58.35 is 66% of the one-year high. The company’s one-year target price is $99.94 per share, putting its closing price at only 58% of that level.

MPC data by YCharts

MPC data by YCharts

Marathon Petroleum pays a dividend of $1.84 per share, a yield of 3.2% to its now-lower stock price.

Overall, the company’s mean analyst rating is a 1.5-1.9, or between “strong buy” and “buy,” from the 19 analysts who follow it. The most recent rating change — occurring today — was Standpoint Research initiating at “accumulate.”

At Sept. 30, 2018, Marathon Petroleum’s largest institutional stock holders were Vanguard with 7.8%, State Street with 5.3%, BlackRock with 4.6%, Boston Partners with 2.8%, and Millennium with 2.6%.

Marathon Petroleum’s beta is 1.61, representing steeper volatility than might be expected for such a large company but reflective of the dual, and not reliably synchronized, uncertainties of oil prices and petroleum product prices.

Logistics Partnerships

Marathon Petroleum's two master limited partnerships, MPLX LP and Andeavor Logistics LP, have combined market capitalization of $32.8 billion: $24.4 billion for MPLX and $8.4 billion for ANDX. The assets of both are mainly pipelines and terminals. Attractiveness of partnership shares are specific to an investor’s tax situation and are not evaluated in this analysis. However, Marathon Petroleum operationally integrates the partnership’s assets with its refining assets.

Governance

Institutional Shareholder Services ranks Marathon Petroleum’s overall governance as an 8, with sub-scores of Audit (2), Board (9), Shareholder Rights (9), and Compensation (1). Approximately 1.4% of the outstanding stock is shorted, a decline from the level of 7.8% two months ago.

A Note on Valuation

The company’s book value per share of $33.63 is about 60% of its current market price, showing that market value of Marathon Petroleum’s assets is higher than its depreciated base and indicating investor optimism.

Positive and Negative Risks

Potential investors should consider their oil and petroleum product price expectations (and thus, refining margin) as the factors most likely to affect Marathon Petroleum. Marathon is advantaged with a diversity of sources and positive exposure to lower-priced inland U.S. and Canadian crude oil supply.

However, the company’s governance score is quite weak.

There's also the risk of distraction as Marathon adds the operations of Andeavor, itself a premier refiner.

Recommendations for Marathon Petroleum

Potential investors should factor the company’s weak governance score into their decisions.

I continue to recommend this well-run largest of the U.S. oil refiners to investors interested in both growth and yield. Stock market downdrafts have reduced its price and thus increased its dividend yield. The company has identified growth synergies in its combination with Andeavor and in the two limited partnerships. Marathon has a history of improving refinery operations, notably of the large Galveston Bay refinery, which speaks to its ability to integrate the Andeavor refineries successfully. Its access to incredibly low-priced Canadian crude as well as discounted Bakken and Permian crude will strengthen refining profitability.

Market timers will want to note that it is not unusual for refiners’ results, and stock prices, to swing up during the spring and summer since summer is peak gasoline season.

While you're here, consider subscribing to Econ-Based Energy Investing, a Seeking Alpha Marketplace platform by a veteran energy investor that draws from a group of more than 400 public companies. Weekly in-depth articles (three company-specific analyses and two stock-by-stock portfolio reviews) provide you with recommendations for long energy investments. Service is discounted at 20% to all current and new subscribers. After January 15, 2019, the price will increase for subscribers joining later, but will remain the same for all who join before January 15, 2019.