Welcome to our Discover Cannabis series, where we publish in-depth research to introduce new cannabis companies to our coverage.

Situation Overview

Planet 13 (OTCQB:PLNHF) has performed very well in 2019 with the stock up 113% this year so far. Much of the growth came from its recently announced financials for its Superstore in Las Vegas where sales topped some of the largest Canadian cannabis companies. However, we view Planet 13's success as unlikely to be replicated given its lack of track record of winning licenses in Nevada and unclear path to enter other states.

Company Overview

Planet 13 is a cannabis company operating in Nevada that has been garnering a lot of investor attention lately. The company has one license to operate a cannabis dispensary in Nevada and has recently used it to open up a large cannabis store called the Superstore. Planet 13 has one cultivation license in Nevada, which has a capacity of 950 kg per year. The company also has two retail licenses to sell medical and recreational cannabis. Before the Superstore was opened, the company used both licenses in its Medizin location. However, the company wasn't able to secure additional retail licenses in the last application round. In order to open the Superstore on November 1, the company had to shut down its Medizin location to make room for the bigger location. The Superstore is a 16,000 square feet complex that benefits from the large number of visitors that come to Las Vegas each year.

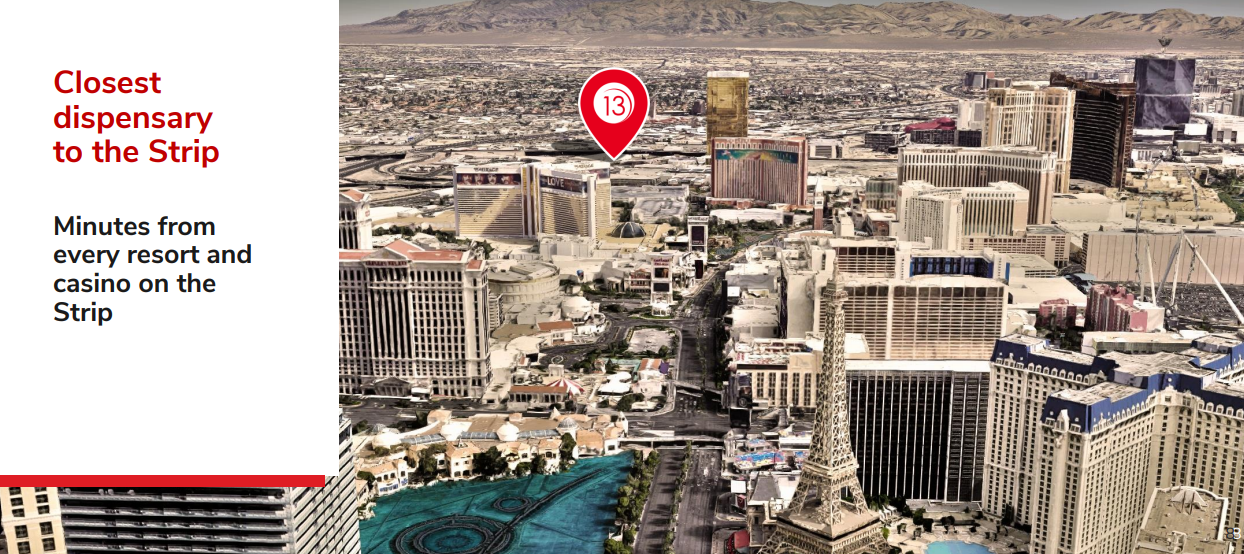

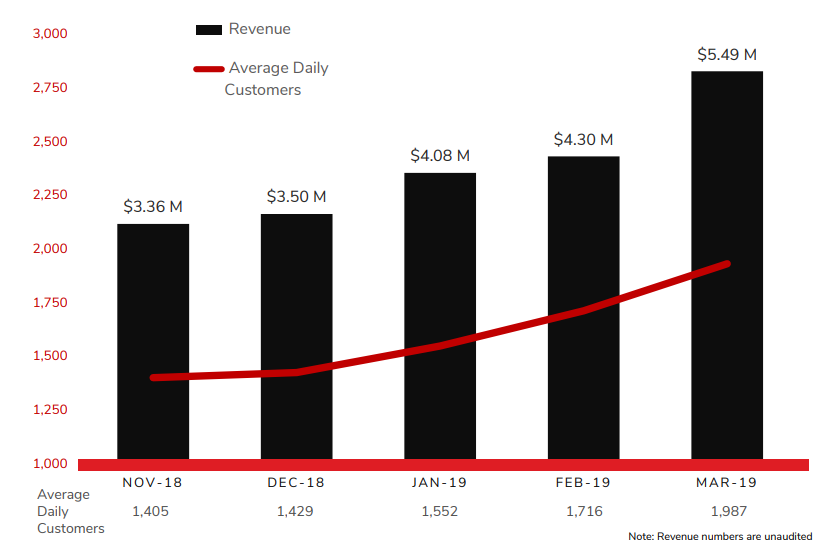

The Superstore is located very close to the Strip in Las Vegas and has produced outstanding sales in the first five months it opened. The company reported sales of $5.5 million in March, which have increased 64% from November 2018 when it first opened. With annualized sales of $66 million based on the latest monthly sales, the Superstore is producing some of the highest sales numbers we are seeing from any company.

(Investor Presentation)

Encouraged by the success of the Superstore, Planet 13 has begun its Phase II expansion that will add a coffee shop and a dining space to the existing cannabis store. Phase II is meant to attract more consumers that might not be looking for cannabis products in the first place and create potential cross-selling opportunities. The company is also thinking of adding more space for hosting events and other social functions.

However, we think the key question for investors is whether Planet 13 could replicate its success at other locations. Within Nevada, the company already failed to secure additional licenses in the last RFP. Outside Nevada, we think it would be extremely difficult to replicate its success in Las Vegas due to two reasons. First of all, the cannabis regulatory environment is highly complex and varies with each state. Planet 13 does not have licenses to operate in other states at this moment. Secondly, Las Vegas is a unique place with its tourism and consumerism, which helped the impressive performance of the Superstore. However, we think other states might not have the same business environment as we have not seen other operators reaching similar economics at their stores. Overall, we view Planet 13's Superstore performance as a largely one-time success that is difficult to replicate.

Valuations Make Sense?

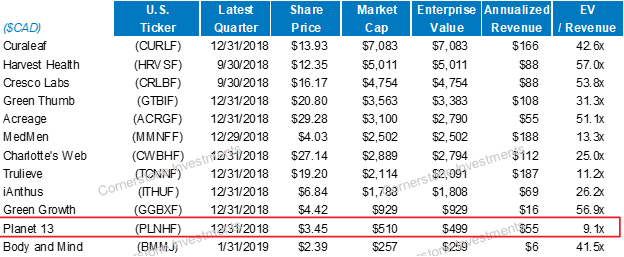

Planet 13 is trading at 9.1x EV/Revenue and has a market cap of C$510 million. While the company does not look very expensive from a valuation perspective, we think Planet 13 should trade at a discount to its peers due to several limitations of its business model. First of all, Planet 13 is enjoying a first-mover advantage in the Las Vegas Strip area. However, we think other players in the Nevada area are also preparing to open stores in the adjacent area. We expect competition to pick up and divert traffic as there is no barrier to entry for Planet 13's existing Superstore. Additionally, the company failed to win any retail license in the latest RFP, which significantly limited its near-term growth potential. Another reason that we think Planet 13 should trade at a discount to other leading MSOs is its concentration risk given its entire operation hinges on a single location. If there is any disruption at its Superstore, the entire company would be affected, which should be factored into the valuation. Similarly, regulatory risks are high for the company given any changes in the current cannabis regulation.

Looking Ahead

Planet 13 is a unique company that made a name for itself by opening one of the largest and possibly highest revenue-earning cannabis stores in the world as far as we know. Since it opened its Superstore in November last year, monthly sales have reached $5.5 million, which is higher than a lot more established companies. For example, Cronos (CRON) generated C$5.6 million and Tilray (TLRY) generated C$20 million in sales during their latest quarter while both companies have market caps over $5 billion. Planet 13's valuation appears reasonable among the small- to medium-sized U.S. cannabis companies; however, its business model carries inherently higher risks due to reliance on a single store for 100% of its revenue.

We view Planet 13 as a risky investment due to its business model that is highly concentrated and lacks diversification. Despite the recent success in its Superstore, we view its near-term growth profile muted due to no path to opening additional stores. Planet 13 failed to secure additional licenses in Nevada which resulted in its closure of another dispensary in order to make room for the Superstore, a situation we think could have been better managed by the company. Overall, we have a neutral view on the stock unless it could find paths to replicate its success at additional locations.