It was not very long ago that the economy was on fire, fueled by tax cuts and other short term measures it seemed like the stock market could do no wrong as our portfolios maintained their upward trajectory. What a difference a few months can make. COVID-19 has decimated world economies while targeting the weakest among us.

But just like the virus has proven that not all people react the same when exposed to adversity so too have the companies we depend on. Where some businesses have struggled after being forced to shutter their doors and may never recover others have continued on, facing the challenges or even excelling in the face of adversity. What has become clear is that business as usual may never be the same and as investors we have to identify those companies that can not only weather the storm but create opportunities investors can take advantage of. Companies like Brookfield Infrastructure (BIP, BIPC).

COVID-19 will necessitate Change

COVID-19 has exposed many businesses that we never thought needed exposing. Services, sports and entertainment, travel, real estate and transportation are a few of the industries that have been significantly impacted. Any business where people come together has been put at risk due to the pandemic. While it will be necessary to re-evaluate how these businesses move forward post pandemic others will transition and continue on more resilient to the adversity around them.

Brookfield Infrastructure has shown themselves to be one of these resilient companies. When the pandemic first hit Brookfield acted quickly to have all of their operations classified as essential services. When governments around the world took measures to shut down their economies to protect their people, Brookfield was taking measures to not only protect their people but protect their ability to continue providing service. As a result all of Brookfield Infrastructures assets continued to be available for service, continued to produce revenues for the company and shareholders.

All things considered a good first quarter

In the first quarter of 2020 BIP generated FFO of $358 million, up 2% from the year before with earnings that were basically in line with the previous year. This was despite significant slowdowns in China for most of the period impacting shipping through their ports business as well as the more widespread impacts that would take place around the world in late February and March.

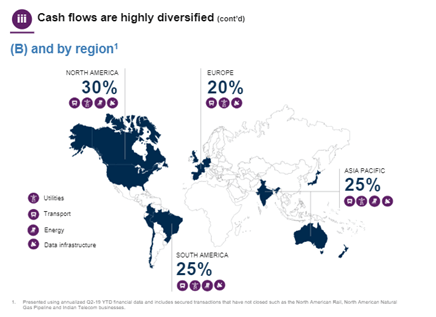

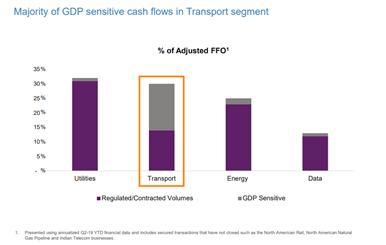

A reason for this resilience has been the fact that their utility, data and energy assets typically generate approximately 70% of FFO and will be less impacted by the current market slowdowns. The greater impact will be felt from their transportation infrastructure assets which are more reliant on steady volumes to generate revenues. Assets like toll roads have experienced a greater drop off than has been felt at their ports and rail businesses reinforcing the importance of diversification within their asset base and minimizing the overall impact to the company.

Geographically the company has also seen differences as Asian economies shut down sooner, had lesser impacts from a health perspective and restarted sooner and perhaps more sustainably than in North America and Europe.

Executing their business strategy

The duration of the crisis will impact the company but reinforces their commitment to stay focused on the four main pillars which underpin their business strategy.

- Maintain high levels of liquidity at all times

- Finance assets with long duration, fixed rate debt,

- Invest in high-quality, well-contracted assets

- Diversify the portfolio by both geography and sector.

The first pillar focuses on their ability to maintain a high level of liquidity at all times. To this end BIP just completed a number of capital markets initiatives which included a C$400 million bond issuance as well as securing operating and corporate level credit facilities. In total the company currently has $4.3 billion in available liquidity leaving it in the strongest position it has been in a number of years.

These initiatives position the company well to weather the current crisis but were prioritized many months ago. I remember Brookfield Asset Management (BAM) CEO Bruce Flatt discussing the need for preparedness back at their Investor Day presentation in 2019 as he felt the current bull market was rather extraordinary and how the company was preparing themselves for the inevitable pullback. I do not believe he envisioned what we are dealing with currently but it does show the company's preparation and that is what shareholders should expect.

The second pillar of their strategy is to finance their assets with long duration, fixed rate debt. To this end the company has been refinancing most of its debt for the past five years pushing out maturities as far as possible while taking advantage of lower rates. Currently only 10% of debt will mature in the next 3 years creating visibility the company is comfortable working within.

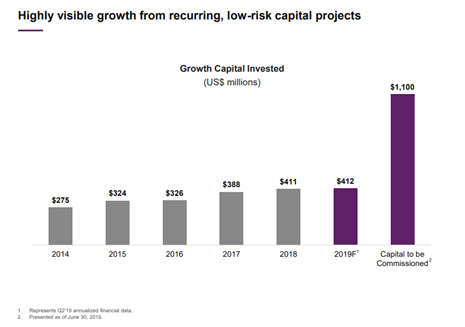

Their third pillar is to invest in high-quality, well-contracted assets which has paid dividends in the most recent quarter as revenues increased by 2% despite adversity in world markets. Of their total growth 6% can be attributed to organic growth aided by $1.6 billion in new investment placed into service during the past year. In an environment where asset valuations had become expensive the company has been taking advantage of the premium valuations on some mature assets to recycle $1 billion in 2019 and an additional $500 million in 2020 to be redirected towards newer higher yielding opportunities.

Although new recycling efforts have been put on hold due to the pandemic I am confident the company will be targeting new opportunities as they present themselves. As proof, during their most recent presentation to shareholders the company revealed that they had initiated equity positions in several major companies they felt had become undervalued as a result of the pandemic opening the door to future activity.

Their final pillar centers on diversifying the portfolio by both geography and sector. This strategy is proving fruitful as markets around the world reopen at different paces and with differing degrees of risk and political support.

Utility like security with a growth company approach to business

During their 2019 Investor Day Presentation, Brookfield Infrastructure Managing Partner and CEO Sam Polluck introduced the term "Grow-tility". He coined this phase to describe how Brookfield Infrastructure combines the traditional characteristics of a growth company with the stability offered by a utility.

Brookfield Infrastructure Partners invests in infrastructure assets that provide essential services through their network of Utilities, Transportation, Energy and Data assets. These include the movement of passengers and freight on toll roads and rail networks, the distribution of energy and other products through ports and pipelines as well as the movement of data through towers and transmission lines. All these services are critical infrastructure to any economy and will remain in demand regardless of economic circumstance.

During the pandemic it is comforting to be able to envision the company as a utility. Similar to a utility many of their services are either contracted or regulated such that cash flows are protected. Like a utility this type of business is very attractive to an income or risk adverse investor who values the steady flow of cash needed to meet their monthly needs.

Different from a utility, which are often constrained in their ability to grow their business by the macro environment in which they operate, BIP works on a more global scale and has the ability to expand their focus as opportunities present themselves. Using a variety of financial levers including debt financing, existing cash flows, new, private and institutional equity, the company searches out value propositions where they can inject their expertise to take on new opportunities that would be accretive to shareholders and partners.

Using this approach the company has been able to grow their business at a much faster pace than most utilities, increase their dividends and expand their enterprise. The company has also been able to be patient taking a longer term approach to their business than many of their competitors are afforded. On their Q1 conference call there were discussions about opportunities that might present themselves in the airport business. BIP has shied away from this sector in the past due to high valuations but it is in times like these that opportunity often presents themselves and the company confirmed that they are exploring a wide number of opportunities.

A focus on quality adds safety to the dividend

When it comes to paying dividends quality of cash flows are key both in terms of the certainty of receiving revenue and in terms of the ability of your customers to pay. In the case of Brookfield Infrastructure 95% of their revenues are either contracted or regulated creating some certainty to their income streams. The other important part is that 85% of those customers represent investment grade companies or institutions.

In their most recent letter to shareholders the company reaffirmed that their dividend is safe. Although the payout ratio has trended above their projected target range, and they anticipate that this will remain the case through the rest of the year, the payout is easily covered within existing FFO. I believe that cutting the dividend would only be as a last resort and based on their current cash flows and strength in their capital position this will not be an issue.

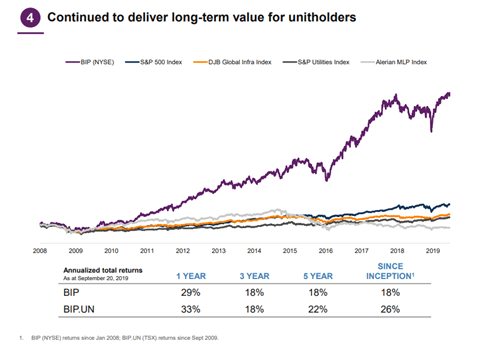

With a current yield of more than 5% following a 6.9% increase at the start of the year this is a great opportunity for new investors. Also important to know is that the company has increased its dividend by an average of more than 9% per year over the last 5 years and regular increases are built into their DNA. As a dividend investor this is the sort of thing that I look for and depend on in my portfolio.

Diversification is a key component to their success

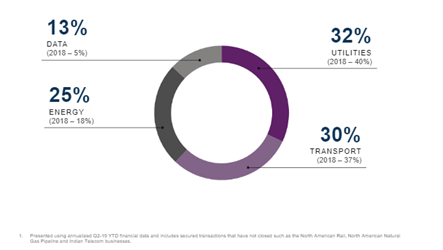

As mentioned earlier 70% of Brookfield's business comes from their Energy, Data and Utilities business which have seen minimal impact from the effects of the coronavirus. Even within their transportation business the impacts have been spread out as a drop in their ports business due to reduced outputs from China and toll road traffic are being offset by rail which experienced a 9% increase in the first quarter. As outputs from China return this should help to offset drops in other parts of the world associated with the current crisis.

In fact recent acquisitions completed in 2019 are adding greater diversification by sector with an increased presence in the data and energy sectors. This trend will continue as the company moves closer to closing their previously announced Indian telecommunications tower initiative. The attached graphic also highlights the geographic diversification that the company enjoys making them the most geographically diversified under the Brookfield Asset Management Partnerships umbrella.

Areas of concern

Transportation remains the greatest area of concern for the company in the short term with 40% of their business exposed directly to GDP and it will be interesting to watch as the world's economies adjust. Despite this the company recently assessed the overall impact from this sector at around 5% to their bottom line which are possible under present circumstances.

Currency fluctuations are also a concern for such a global business with Brazil currently presenting particular challenges through the depreciation of their currency. Even though year over year revenues are heading in a positive direction for the country when converted to USD they show declines. As they emerge from a prolonged recession the hope is that things will continue to trend in a positive direction, however the current crisis and a lack of strong leadership confronting it are not helping them.

Other currencies, like the Canadian dollar, have also taken a hit during the crisis as the collapse in the price of oil and a flock to the safety of the USD have had an impact on resource based economies like Canada. As the price of oil rebounds this should benefit some of these countries.

There is also the concern that there could be a second wave of the coronavirus as businesses open and people resume their activities without an approved vaccine or accepted treatment.

A great opportunity for the contrarian investor

Organically BIP is in a position where they should be able to grow their business between 6-9% on an annual basis. In this environment that would make many investors very happy. Add to that the fact that they annually reinvest between 15-20% of their cash flow back into the business in terms of productivity enhancements and organic growth it explains their ability to increase the dividend by over 9% per year for both the 5 and 10 year periods.

But Brookfield has historically been a company that has thrived during times of uncertainty, taking a contrarian approach to many of their investment ideas. This time is no different. During the first quarter the company was aggressively investing in the shares of companies they felt presented significant undervaluation due to the pandemic.

They are looking at these investments as a potential starting point towards future activity with these companies. In a worst case scenario they feel confident they can recycle the shares at higher valuations should no greater opportunities present themselves. This is why I like Brookfield. When many companies are looking for shelter they are looking for opportunity.

The fire sale may be ending

When compared to their historical valuation levels and their peer group Brookfield Infrastructure appears to be attractively valued trading significantly below its 52 week highs. Currently, Brookfield trades at a valuation of 5.7x FFO which compares to 9.3x its 5 year average. Using these metrics it is currently trading 39% below its 5 year average. Compared to its peer group average of 7.7x FFO it currently trades 26% below that benchmark as well.

Another plus is their current 5% dividend which is a full percentage point higher than their average North American Utility peer group. As a dividend investor this is a key consideration for me as I prioritize income and the company's ability to support and grow that income. With a five year growth rate above 9% I am confident that in the medium to long term I will stay ahead of inflation which enhances versus maintaining my quality of life. In the short term I am not expecting a 9% increase but am confident it will not be cut and believe that it will still increase above my personal 5% benchmark that I like to use.

Another thing to be aware of is their current K1 status and the tax implications or restrictions created for US investors investing in their regular BIP shares. To avoid this invest in their newly created (NYSE:BIPC) shares or carry your holdings in a registered account.

I do believe that Brookfield infrastructure, like most companies, was caught up in the panic of the pandemic and will eventually work itself back to its previous trading range. This may take several weeks or several months for consistency to work its way through their earnings but I am confident that as normalcy returns so will their premium valuation.

Final Thoughts

During periods of uncertainty some people get rich and others lose their shirts. That is the difference between investors and speculators. As an investor I am always looking for great companies that provide me security knowing that their businesses are well run, present superior growth prospects, are protected by a deep moat and share their success with shareholders. As a dividend investor I look for companies that provide a generous and steadily growing dividend. Brookfield Infrastructure checks all of these boxes.

The fact that they were able to grow in what was a most challenging first quarter reaffirms my confidence in their business model and their ability to execute. Being able to draw on a large capital pool with the support of their parent company and institutional investors is also a plus. Add to this their history of capitalizing during periods of uncertainty and it gives me confidence they will use this crisis to generate new opportunities in the long term.

Their resiliency, an ability to execute and capitalize on opportunities will support the long term growth in their dividend which for me is the most important part of their success story. For this reason I am bullish on Brookfield Infrastructure and you should be too.