For the second month in a row, June non-farm payrolls crushed expectations with a gain of 4.8 million jobs compared to a consensus estimate of 3 million. Since May, 7.5 million jobs have returned dropping the unemployment rate to 11.1% from a peak of 14.7% in April reinforcing the theme of an emerging recovery out from the worst of the pandemic. While it's positive that more people are getting back to work, investors should look at the declining unemployment rate in the context of what continues to be significant economic weaknesses.

What we're seeing is a return of temporarily laid-off workers from industries most directly impacted in the early stages of the pandemic. More concerning is the prospect of a significant number of permanent job losses that represent structural challenges for the economy beyond this year. Separately, the recent trend of spiking coronavirus cases is set to slow the pace of job gains in the coming months that adds a new layer of uncertainty. We think the outlook remains bearish for stocks and expect more downside in the second half of the year.

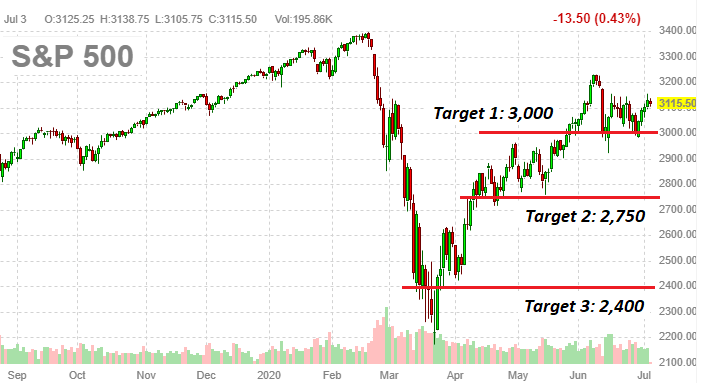

(Source: finviz.com)

The S&P 500 index (SPY) currently at ~3,115 is still about 3% lower from the highs in early June while the past month has been defined by renewed volatility. The setup here is that the surge in coronavirus cases now represents a catalyst for renewed financial stress across the economy. We think a breakdown below 3,000 can put the bears firmly back in control targeting 2,750, or about 8% downside over the next couple of months, as our next target. A move lower to 2,400 through next year would take the market to a more reasonable valuation where a new reassessment can be made.

How The Market Got The June NFP So Wrong (Again)

One

Are you interested to learn how this idea can fit within a diversified portfolio? With the Core-Satellite Dossier marketplace service, we sort through +4,000 ETFs/CEFs along with +16,000 U.S. stocks/ADRs to find the best trade ideas.

Click here for a two-week free trial and explore our content.