Welcome to our Cannabis Earnings series where we break down the latest earnings to help you focus on the most important topics.

Introduction

Supreme Cannabis (OTCQX:SPRWF) has been a disappointment for investors but it was easy to spot the flaw in its previous B2B business model. The most direct reason behind Supreme's ~90% share price collapse was its insolvency and the following debt restructuring that led to massive dilution. While progress has been made under the new CEO, the company still has a long way to go to repair its balance sheet and it probably will never reach its previous share prices after diluting shareholders by 67% since mid-2019.

(All amounts in C$)

Making Progress

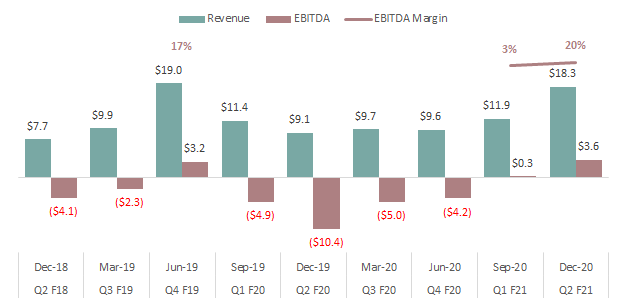

Supreme Cannabis underwent a period of transition last year when the wholesale market collapsed due to a severe oversupply. The company suffered from sales declines and margin compression leading to its worse quarter in Q4 F2020 when EBITDA came in at a negative $10M. Since then, the company pursued aggressive cost-cutting and appointed Beena Goldenberg as the new CEO who is already making good progress on the turnaround. Beena was the former CEO of Hain-Celestial Canada and interestingly Aphria's current CEO Irwin Simon was the founder and CEO for Hain Celestial (HAIN).

(Source: Filings)

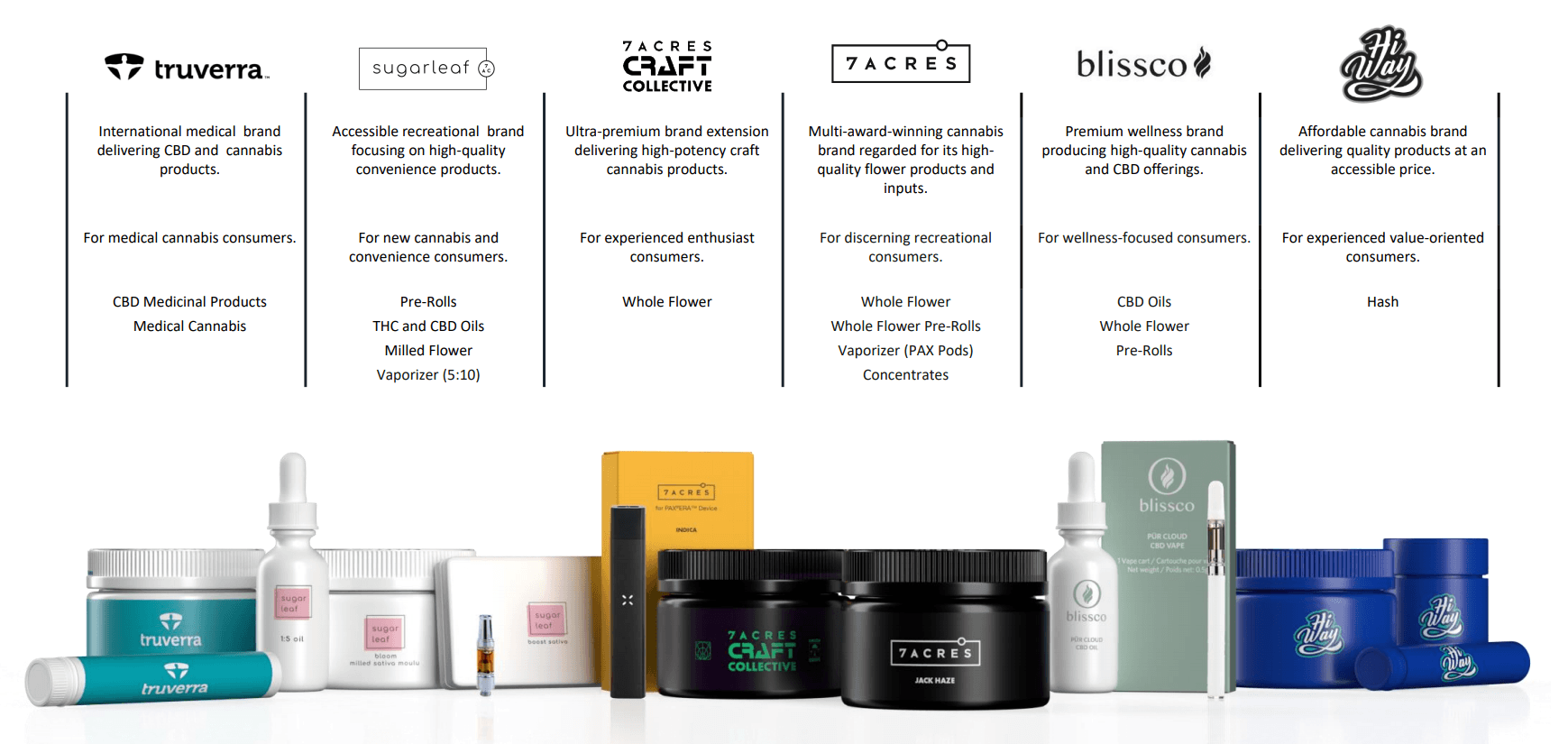

Supreme achieved improving operational results last quarter as its expanded product offering is driving higher sales. It also hired a sales agency humble-fume to help drive sales with physical retailers in Canada. One of the most critical tasks for Supreme during the last year was to create a portfolio of consumer brands in order to transition away from the wholesale market. Due to the strategic mistake of focusing on wholesale, Supreme suffered from a late start compared to other LPs.

Therefore, Supreme's direct sales to the provinces still lagged other leading LPs and its balance sheet was stretched due to mounting losses and dwindling financing options. The company is starting to make some progress with losses turned into positive EBITDA and sales rose in the D2C segment which made up 70% of its Q1 sales. We think the CEO is definitely making the right moves to position Supreme as a viable company but the balance sheet risk remains high.

(Source: IR Deck)

When we first wrote about Supreme in May 2018, we already concluded that its B2B business model was not smart given that it was reasonably easy to see the inevitable oversupply in Canada:

Supreme focuses on executing on its B2B strategy in the cannabis space. The strategy will result in lower realized prices and subject Supreme to risk of the oversupplied market.

Unfortunately, Supreme did not realize that until it got crushed in 2019 as the wholesale market evaporated. However, developing new brands and signing up new distribution agreements take time and other LPs had a headstart in the direct-to-consumer race. Supreme also lacks the capital markets prowess like Aurora (ACB) and Sundial (SNDL) so it could not access capital markets to help with its upcoming debt maturity.

Aurora and Sundial were able to chug along only because they could issue practically an unlimited number of shares via ATM programs which made them the modern era "zombie" stocks that can never die. Supreme did not have a major U.S. listing and had limited trading volume so its ATM was tiny and insufficient. In summary, Supreme made an early mistake by focusing on the wholesale business and it also lacks capital markets depth like some Canadian LPs to raise required financing.

Balance Sheet and Valuation

While Supreme is starting to make some progress on turning around its operations, the company had to restructure the balance sheet to avoid bankruptcy. The company was effectively insolvent when it realized that it could not repay its upcoming convertible debentures. Supreme had $100M of convertible debentures due October 2021 that it could not repay, so it pursued a debt restructuring in late 2020 to convert $63.5M of the principal into 116.6 million shares issued at $0.17/share.

The remaining $36.5M of debentures were restructured to extend the maturity to September 2025, lower the coupon to 8.0%, and lower the conversion price to $0.285/share. Supreme also had to issue a new tranche of Accretion Debentures which will grow to $13.5M from September 2020 to 2023. Needless to say, it was a necessary but very costly transaction for Supreme shareholders.

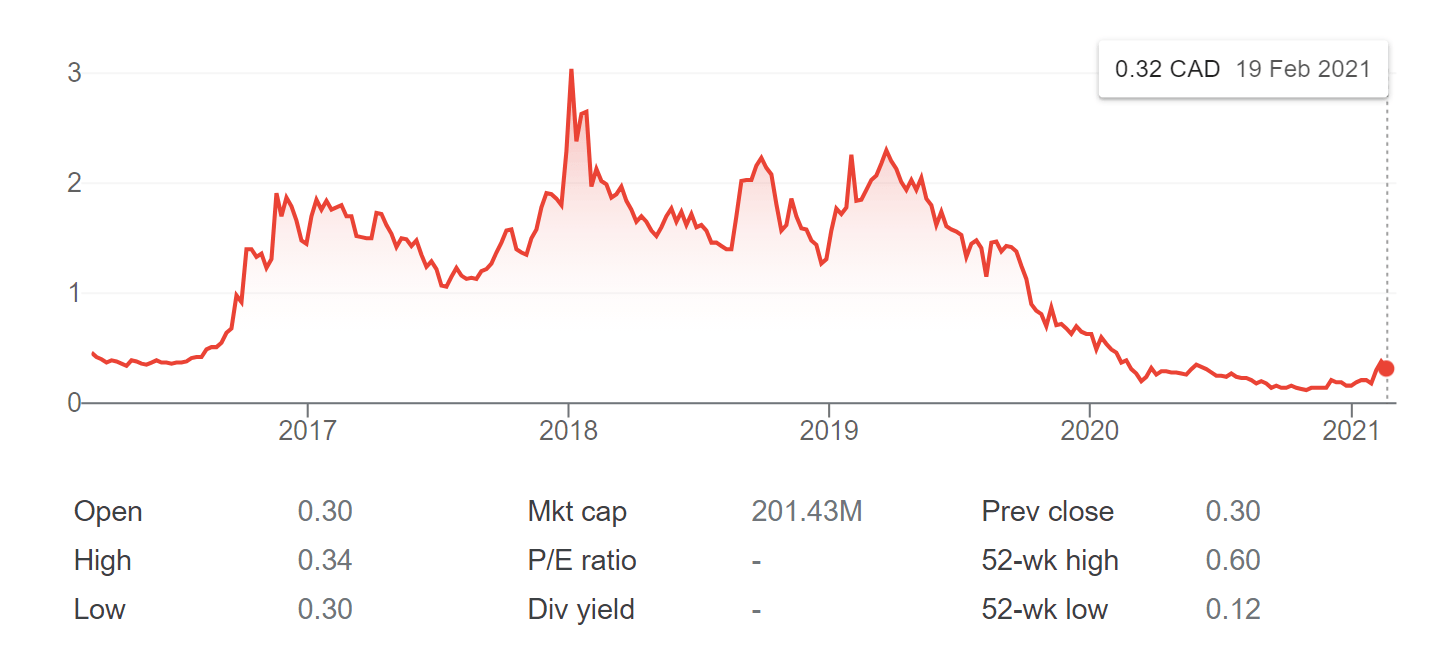

(Source: Google Finance)

Due to the debt restructuring and several equity issuances, Supreme's share count ballooned from 301 million on June 30, 2019, to 508 million on December 31, 2020. The debt restructuring was the biggest contributor to this increase but Supreme also issued 32 million shares to acquire BlissCo and Truverra in 2019. It also has a small ATM program and has issued 19 million shares at an average price of ~$0.20. The huge dilution and punitive debt restructuring was a key reason for the ~90% share price drop.

Supreme has a market cap of $170M and trades at ~3x EV/Sales and 14.5x EV/EBITDA based on the latest quarter annualized. These valuation metrics do not look very high but the stock still carries high balance sheet risk. After the aforementioned debt restructuring, Supreme still has $58M of bank debt and $37M of convertible debt (currently in the money). It also has $13.5M of accretion debentures mentioned above which are essentially cash obligations.

Supreme definitely recognizes its precarious financial position and took advantage of the recent market frenzy to conduct two back-to-back equity issuances. It raised $23M at $0.19 per share in January and another $26M at $0.31 per share in February. It is smart for management to do everything to ensure its near-term survival and the capital markets could close for an extended period of time once the current mania faded. However, the equity issuances done at depressed prices and accompanying warrants made a comeback to previous share prices that much more difficult.

Conclusion

Under the new CEO, Supreme has made tangible progress on entering the consumer markets after a costly early strategic mistake of focusing on the wholesale business. We had identified the flaw in its business model as early as May 2018 but the fiasco eventually played out over the next two years. Now that Supreme is competing with other LPs in the consumer market, it is finding some initial success with its brands and products.

However, the Canadian market is hyper-competitive and it remains to be seen whether Supreme could capture additional market share. The Canadian market has improved significantly during 2020 as Ontario ramped up retail rollout so Supreme should benefit along with the broader industry. At the end of the day, Supreme remains cash tight and rushed to raise equity at depressed share prices twice in the last two months. Therefore, we remain cautious about the stock due to its fragile balance sheet and risks of additional dilution in the near term.